Neutral IndusInd Bank Ltd for the Target Rs. 950 by Motilal Oswal Financial Services Ltd

Lower provisions aid earnings; guides FY27 exit RoA at 1%

Adjusted NIM expands 4bp QoQ

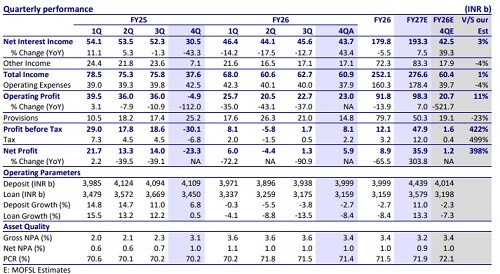

* IndusInd Bank (IIB) reported a 4QFY26 PAT of INR5.9b (MOFSLe PAT: INR1.2b), backed by lower opex and provisions.

* NII grew 43% YoY (dipped 4.2% QoQ) to INR43.7b (largely in line). Its NIM expanded 4bp QoQ to 3.39% (Adj. NIM stood at 3.35% in 3QFY26).

* Other income was flat QoQ (4% miss on MOFSLe). Opex declined 11% YoY/5% QoQ to INR37.9b (4% lower than MOFSLe).

* The loan book dipped 8.4% YoY (-0.5% YoY), amid a rundown in corporate book, while the bank aims to shift from large corporate to mid-market. Deposits rose 1.6% QoQ (down 2.7% YoY), led by CASA deposits.

* Fresh slippages declined 29% QoQ to INR18.2b in 4QFY26. The GNPA ratio improved 13bp QoQ to 3.43%, while the NNPA ratio declined 4bp QoQ to 1.0%. PCR stood flat at 71.4%.

* We raise our earnings and project IIB’s RoA/RoE at 0.7%/5.6% for FY27E. Reiterate Neutral with a TP of INR950 (based on 1.1x Sep’27E ABV).

Credit growth to track system growth in FY27E; credit costs improve

* IIB reported 4QFY26 PAT of ~INR5.9b (vs. our profit estimate of INR1.2b), aided by lower opex and provisions.

* NII grew 43% YoY/dipped 4% QoQ to INR43.7b (largely in line). Its NIM improved 4bp QoQ to 3.39% (adj. NIM stood at 3.35% in 3QFY26).

* Other income grew 0.4% QoQ (up 142% YoY, 4% miss on MOFSLe). Opex declined 11% YoY/5% QoQ to INR37.9b. C/I ratio, thus, declined to 62.3% vs. 63.8% in 3QFY26. PPoP thus stood flat QoQ at INR22.9b (11% higher than MOFSLe).

* Provisions stood lower vs. our estimate at INR14.8b (down 29% QoQ/ 41% YoY decline), as slippages declined for most of the segment, including MFI.

* The loan book declined 8.4% YoY/0.5% QoQ to INR3.2t, amid a continued dip in the corporate book (down 16% YoY and 3% QoQ). While retail declined 4% YoY/up 1.1% QoQ, within retail, VF grew 4.5% YoY/1.7% QoQ, and consumer banking stood flat QoQ (up 6.7% YoY).

* The deposit book grew 1.6% QoQ (down 2.7% YoY), amid the bank’s focus on de-bulking large bulk deposits. CASA book grew 4.9% QoQ (down 7% YoY), led by a spike in CA deposits due to seasonality (up 11.5% QoQ). Hence, the CASA ratio inched up to 31.2%.

* Fresh slippages declined 29% QoQ, led by improvement across segments (VF, MFI, and consumer). As a result, the provisions also experienced improvement. Asset quality ratios improved with GNPA/NNPA declining 13bp/4bp QoQ to 3.43%/1.00%. PCR was largely flat QoQ at 71.4%.

Highlights from the management commentary

* The bank aims to align credit growth broadly with industry levels in FY27E. The industry credit growth is expected at ~13-14%.

* Management aims to improve RoA to 1% by the end of FY27, led by NIM, improvement in fee income, and optimization in the balance sheet.

* The focus on the mid-market segment is increasing; wholesale growth will be driven more by the mid-market, while large corporate exposure has seen some dip.

* Liability-side repricing is largely complete, though CASA franchise improvement is still underway. An improvement in CASA mix should support a reduction in deposit costs going forward.

Valuation and view

IIB reported a decent quarter, supported by stronger NII and sharply lower-thanexpected provisions, driven by improvement in slippages across segments. Consequently, RoA improved to 0.45% from 0.1% in 3QFY26, with the bank targeting an exit RoA of ~1% by the end of FY27E. Other income remained subdued due to modest fee and treasury income, while opex declined QoQ. NIMs expanded 4bp QoQ to 3.39% (adjusted for one-offs in 3Q). Business growth was modest, reflecting debulking of the corporate book and a strategic shift towards the mid-market segment. Deposit growth was fueled by CASA, resulting in a decline in the CD ratio to 79%. The reduction in slippages was broad-based, leading to lower provisions in 4Q versus expectations. The bank expects loan growth to broadly track industry growth in FY27, with potential to outpace the industry in FY28. We raise our earnings by 14%/18% for FY27/28E and project IIB’s RoA/RoE at 0.7%/5.6% for FY27E. Reiterate Neutral with a TP of INR950 (premised on 1.1x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412