Neutral HDB Financial Services Ltd for the Target Rs.720 by Motilal Oswal Financial Services Ltd

* HDB Financial Services’ (HDBFIN) 4QFY26 PAT rose 41% YoY/17% QoQ to ~INR7.5b (in line). FY26 PAT grew 17% YoY to INR25.4b. NII in 4QFY26 grew 22% YoY to ~INR24b (in line). Other income stood at ~INR6.6b (up 3% YoY).

* Opex grew ~7% YoY to ~INR13.7b (in line). Cost to income (CIR) in the lending business was stable QoQ at 39.5% (PQ: 39.5%, excluding the impact of labor code, and PY: 42.9%). PPoP stood at INR17b and grew 27% YoY (in line).

* Yields (calc.) declined ~10bp QoQ to 14%, while CoB (calc.) declined ~40bp QoQ to 7%, leading to spreads (calc.) rising ~30bp QoQ to ~7%. Reported NIM in 4QFY26 rose ~15bp QoQ to ~8.25%.

* Management shared that the sequential decline in yields during the quarter was driven by a change in the product mix, and it expects improvement in yields as growth in unsecured segments picks up. HDBFIN targets sustaining NIM in the ~8%+ range going forward as well. We estimate NIM of 8.2%/8.1% in FY27/FY28E (vs. 8.25% in FY26).

* Management indicated that there has been no material impact from geopolitical tensions so far, including within the MSME segment, with performance in Mar’26 remaining stable. However, the situation remains fluid, and the company will continue to closely monitor any potential second or third order impacts over the coming weeks/months.

* HDBFIN is witnessing improvement across key operating metrics, with better asset quality, moderating credit costs, and improving margins. However, overall loan growth remained relatively subdued, impacted by elevated repayments despite healthy disbursements. While the business trajectory is improving, the pace of recovery in loan growth continues to be gradual. We await a clearer and more sustained traction in loan growth before turning constructive on the stock, as a meaningful acceleration in loan growth will remain a key monitorable for a valuation re-rating.

* We estimate a CAGR of 14%/16%/20% in disbursement/loans/PAT over FY26-28, with RoA/RoE of ~2.5%/14.3% in FY28. Reiterate Neutral with a TP of INR720 (premised on 2.2x Mar’28E BVPS).

* Key risks: 1) Execution risk remains in translating scale into sustained profitability, as operating efficiency metrics currently lag peers; 2) rising competition in semi-urban and rural lending and potential yield compression, and 3) credit costs continuing to remain elevated even in the following years.

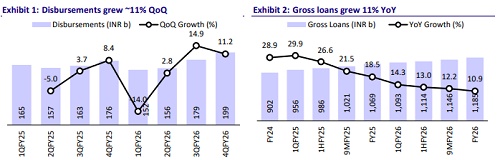

Disbursement momentum picks pace; loan growth muted at 11% YoY

* Total loan book grew 11% YoY and ~3.3% QoQ to INR1.18t. Enterprise lending loan book grew 7% YoY/3% QoQ, Asset finance grew 10% YoY/2.6% QoQ, and Consumer Finance grew 19% YoY/5% QoQ during the quarter.

* Disbursements grew 13% YoY and 11% QoQ to INR199b. Enterprise lending disbursements grew ~16% YoY, asset finance disbursements declined 1% YoY, and consumer finance disbursements grew 25% YoY. Repayments (annualized) were elevated at 56% (PY: 50% and PQ: ~53%).

* Total customer franchise rose ~20% YoY to 22.9m.

* HDBFIN indicated that while 1Q is typically a seasonally softer quarter, it still expects healthy growth, with the improving business momentum witnessed in 2HFY26 likely to sustain into FY27. Management targets a loan growth in the range of Nominal GDP + 6-7% over the medium term. We model a loan CAGR of ~16% over FY26-28E.

Improvement in asset quality; sequential moderation in credit costs

* Asset quality improved with GNPA declining ~40bp QoQ to ~2.45%, while NS3 declined ~15bp QoQ to ~1.1%. PCR was broadly stable QoQ at ~55.5%.

* Credit costs stood at ~INR6.8b (in line). Annualized credit costs stood at ~2.3% (PQ: ~2.5% and PY: ~2.4%). HDBFIN shared that asset quality improved across all segments, including the unsecured portfolio, supported by prudent underwriting and stronger collection efforts. Management guided for FY27 credit costs of ~2.3%, backed by improving trends in asset quality. We estimate credit costs (as % of avg. loans) of ~2.4%/2.2% in FY27/FY28E.

Key highlights from the management commentary

* Management highlighted its strategic focus on increasing the share of used vehicle financing, with a target to achieve a balanced 50:50 mix between new and used vehicles over the medium term.

* The company highlighted that risks arising from the West Asia conflict and potential weather-related disruptions remain key monitorables, particularly from the perspective of inflation and overall growth.

* Cost of funds (CoF) is being actively managed through a diversified borrowing strategy, with management indicating that CoF is expected to remain broadly stable in 1QFY27.

Valuation and view

* HDBFIN reported a healthy quarter, with a meaningful pickup in disbursements, even as the overall loan growth remained muted due to elevated repayments. Asset quality improved sequentially, leading to a moderation in credit costs. Margins expanded ~15bp QoQ, supported by a decline in CoF.

* HDBFIN currently trades at 2.3x FY27E P/BV. We estimate a CAGR of 14%/16%/20% in disbursement/AUM/PAT over FY26-28, with RoA/RoE of ~2.5%/14.3% in FY28E. Reiterate Neutral with a TP of INR720 (premised on 2.2x Mar’28E BVPS). With valuations largely factoring in medium-term growth potential, we will look for clearer evidence of stronger execution on loan growth, the ability to better navigate industry/product cycles, and structural (not just cyclical) improvement in return ratios.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041