Neutral Bharat Dynamics Ltd For Target Rs.1,150 Motilal Oswal Financial services Ltd

Weakness persists through FY26

Bharat Dynamics’ (BDL) results were weaker than our estimates, with execution impacted by delays in the supply of radars, seekers, and other components for Akash and Astra Mk1 missiles from external vendors. The company is likely to book ~INR20- 25b of revenues in 1HFY27 from these orders as the supply of these components commences. BDL may also resort to importing certain components to avoid further delivery delays. While the order book remained healthy at ~INR260b, we expect overall execution to remain slower than our earlier estimates, with margins likely to stay under pressure due to a higher share of bought-out components. We, thus, cut our FY27/FY28 earnings by 25%/28% and downgrade the stock to Neutral with a revised TP of INR1,150 (vs. INR1,500 earlier), based on 42x Jun’28E EPS. The stock is currently trading at 70.5x/48.1x/38.1x on FY27/FY28/FY29 EPS. We believe it is prudent to await a sustained ramp-up in execution and improved supply-side visibility.

Weak set of results

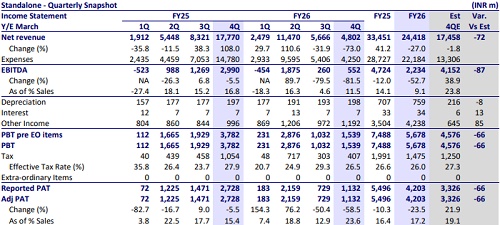

BDL reported a weak set of results with a miss across all metrics. Revenue declined 73% YoY to INR4.8b in 4QFY26. Gross margin remained strong at ~62.4% in 4QFY26. However, due to weaker execution, operating deleverage resulted in EBITDA margin being lower at 11.5% vs. our estimate of 23.8%. Absolute EBITDA declined 82% YoY to INR552m. Weak execution and margin contraction led to PAT declining 59% YoY to INR1.1b (66% below our estimate). For FY26, revenue/EBITDA/PAT declined 27%/53%/24% YoY to INR24.4b/2.2b/4.2b, while EBITDA margin contracted 500bp YoY to 9.1%. For FY26, OCF increased 260% YoY to INR6b, while the company reported FCF inflow of INR3.8b due to capex of INR2.2b during the year (vs. an outflow of INR1b in FY25).

Performance impacted by delays from external vendors

FY26 revenue performance was impacted by ~INR20b due to delays in deliveries of Akash and Astra Mk1 missiles. The delay in Akash missile was primarily due to delayed supplies of radars and communication systems from another vendor. While testing of these systems has been completed, final government clearance is still awaited. The company expects to deliver and book ~INR13b of revenue from this project itself in 1QFY27. For Astra Mk1, delays in receipt of seekers from an external vendor impacted execution; with this issue likely to persist for some more time, BDL has decided to import these components to avoid further slippages and expects to book ~INR10b of related revenue by 2QFY27. Other key deliverables during FY27 include ATGM and MRSAM programs. With this, FY27 revenue can scale up to ~INR45b, with margins of ~14-15%, as a higher share of bought-out components could continue to weigh on profitability. FY28 is expected to mark the peak execution phase for Akash, with potential revenues of ~INR65b and improved margins as the share of missiles increases. We expect revenue to expand at a CAGR of 58% over FY26-28, while execution ramp-up across key missile programs and resolution of supply-side bottlenecks will remain key monitorables.

Valuation and view

The stock currently trades at 70.5x/48.1x/38.1x P/E on FY27/FY28/FY29 estimates. We downgrade our rating on the stock to Neutral with a revised TP of INR1,150 (vs INR1,500 earlier), based on 42x Jun’28E earnings

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041