Neutral Bata India Ltd for the Target Rs.600 by Motilal Oswal Financial Services Ltd

Operational discipline visible; structural upside limited

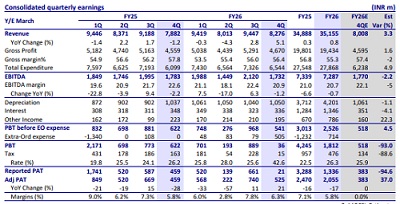

* Bata India (BATA) reported 5% revenue growth in 4QFY26, marking a second consecutive quarter of improving momentum, driven by broad-based growth across channels and categories.

* Reported EBITDA margin contracted 135bp YoY to 20.9% due to one-offs, while adjusted PAT rose 21% YoY to INR525m, reflecting stronger underlying profitability.

* FY26 was a year of operational reset, with management focused on improving the consumer value proposition through product refreshes, inventory simplification, and channel execution.

* While a weak start kept FY26 revenue broadly flat and pre-Ind AS margins contracted 40bp to 10.4%, growth accelerated in 2HFY26, suggesting early benefits from these initiatives.

* Management highlighted stabilization in the value segment and continued strength in premium brands such as Hush Puppies and Power.

* ZBM has scaled to 550 stores, delivering ~5% higher sales than the rest of the network. Although these locations account for only ~50% of COCO stores, they contribute over 70% of COCO revenue, highlighting their superior productivity.

* While strategic initiatives are beginning to yield results, we believe a sustained acceleration in growth will require further improvement in product relevance and execution.

* Accordingly, we continue to build in a measured earnings recovery, forecasting FY26–28E revenue/EBITDA/adj. PAT CAGR of 4%/7%/7%. Reiterate Neutral with a revised TP of INR600 set at 25x FY28E EPS

Working capital and cash flow

* Inventory days improved sharply to 73 days (vs. 85 days in FY25), the lowest in several years, driven by accelerated clearance of aged inventory, decluttering initiatives, and tighter inventory control. Absolute inventory declined 13% YoY, while core working capital remained stable at ~58 days.

* Operating cash flow (post leases) declined to INR2.1b (vs. INR3.8b in FY25) due to weaker profitability. Consequently, FCFF moderated to INR1.5b from INR3.1b in FY25.

Valuation and view

* Strategic initiatives are gaining traction, led by franchise-led distribution expansion, product premiumization, sharper youth-focused offerings, and continued investments in inventory productivity, omnichannel capabilities, and brand building.

* While operating metrics are improving, we believe it will take time for these initiatives to translate into sustained revenue acceleration and meaningful margin recovery, with profitability likely to remain below pre-COVID levels, even by FY28E.

* We modestly revise our FY26–28 estimates and project revenue/EBITDA/adj. PAT CAGR of 4%/7%/7% over FY26-28E.

* However, a potential demand recovery in the organized value footwear segment, following GST rationalization, limits downside. Reiterate Neutral with a revised TP of INR600.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

2.jpg)