Neutral Bajaj Auto Ltd for the Target Rs. 9,965 by Motilal Oswal Financial Services Ltd

Healthy performance in a tough macro

Outlook remains uncertain across key segments

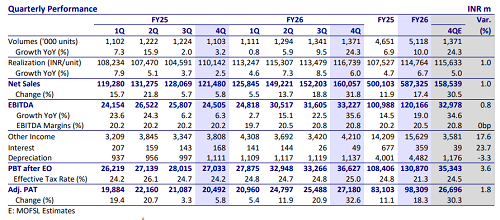

* Bajaj Auto’s (BJAUT) 4QFY26 earnings at INR27.2b were in line with our estimate. Favorable currency, price hikes, and an improved mix helped offset cost headwinds and maintain margins QoQ at 20.8% (in line).

* While BJAUT has been able to post healthy performance in this adverse macro thus far, there are multiple headwinds to navigate. Export demand remains healthy, though the outlook remains uncertain, given the geopolitical issues. Even in the domestic market, while BJAUT is likely to outperform the motorcycle industry on the back of its new launches, growth is likely to moderate in FY27E. Further, a sharp surge in input costs is likely to limit margin upside. Overall, we factor in BJAUT to post 15%/15%/14% CAGR in revenue/EBIDTA/PAT over FY26-28E. At 25.4x/22.2x FY27E/FY28E EPS, the stock appears fairly valued. We reiterate a Neutral rating with a TP of INR9,965, based on 22x FY28E core EPS.

Performance in line

* BJAUT’s 4QFY26 revenues came in line with our estimates, growing 31.8% YoY to INR160.1b. Volumes were up 24.3% YoY to ~1.4m units and realizations were up 6% YoY to ~INR117k units. An improved product mix, favorable currency movement, and record volumes drove growth across all businesses.

* EBITDA margins grew 60bp YoY to 20.8% (flat QoQ), in line with our estimates. Margins were stable QoQ despite input cost inflation, as led by an improved mix, price hikes, and favorable currency.

* EBITDA also grew 35.6% YoY to INR33.2b.

* PAT for the year was up 32.6% YoY to INR27.2b, in line with our estimates.

* For full year FY26, Revenue/EBITDA/PAT grew by 17.4%/19%/18.3% to INR587b/INR120b/INR98.3b, respectively.

* CFO for FY26 stood at INR89.6b, and FCF was at INR85.4b. RoE and RoCE for FY26 stood at 29.3% and 28.1%, respectively.

Highlights from the management commentary

* BJAUT has lined up new models, with refreshed launches in both 125cc and 150cc+ categories expected from July onward, including new Pulsar offerings aimed at further strengthening competitiveness. However, they have not yet revealed the timeline for the launch of the new affordable 125cc motorcycle.

* Near-term demand outlook for domestic motorcycles has moderated, with near-term industry growth expected at 7-9% based on April trends, reflecting the impact of price hikes, potential inflationary pressure, and weaker consumer sentiment. Within this moderation, the premium motorcycle segment, particularly 150cc+, is expected to grow at ~1.5x-2x the broader industry.

* The export outlook remains robust in the near term, driven by strong positioning in key markets such as Latin America and Asia, although geopolitical risks and logistics challenges remain monitorable.

* Electric mobility across both two-wheelers and three-wheelers is expected to continue growing faster than the broader market, remaining a key strategic growth engine for BJAUT.

* Commodity inflation is emerging as a significant near-term headwind, with steel up ~15%, copper ~20%, and aluminum/noble metals up 35–45%, translating into a projected material cost inflation impact of ~3.5–4.0% of revenues in 1QFY27. However, favorable currency movements and pricing actions helped mitigate the impact in 4Q. The company has already implemented pricing action in April to offset ~40% of this impact.

Valuation and view

While BJAUT has been able to post healthy performance in this adverse macro thus far, there are multiple headwinds to navigate. Export demand remains healthy, though the outlook remains uncertain, given the geopolitical issues. Even in the domestic market, while BJAUT is likely to outperform the motorcycle industry on the back of its new launches, growth is likely to moderate in FY27E. Further, a sharp surge in input costs is likely to limit margin upside. Overall, we factor in BJAUT to post 15%/15%/14% CAGR in revenue/EBIDTA/PAT over FY26-28E. At 25.4x/22.2x FY27E/FY28E EPS, the stock appears fairly valued. We reiterate a Neutral rating with a TP of INR9,965, based on 22x FY28E core EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

600-400.jpg)