Neutral Alkem Laboratories Ltd For Target Rs.5,840 Motilal Oswal Financial services Ltd

Strong finish; softer road ahead Domestic revival and US momentum intact; opex limits the earnings upgrade cycle

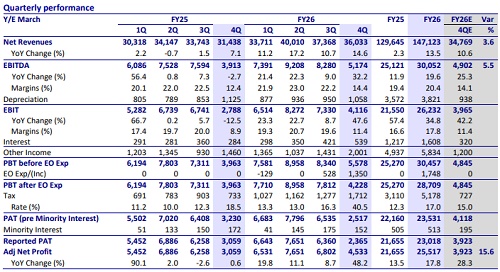

* Alkem Laboratories (ALKEM) delivered a better-than-expected financial performance with a 4%, 6%, and 16% beat on revenue, EBITDA, and PAT for 4QFY26. Strong traction in the exports segment and higher other income led to superior performance for the quarter.

* ALKEM exhibited 100bp YoY outperformance to the industry growth in the domestic formulation (DF) segment. Revival in Acute therapies and sustained growth momentum in chronic therapies led to better-than-industry growth for ALKEM. The trade generics segment is in a gradual recovery mode.

* The US business segment sustained the sales momentum on the back of new launches and increased volume off-take. The niche product launches are expected to sustain the growth prospects in FY27 as well.

* Broad-based growth across markets led to 24%/27% YoY growth in the Non-US export segment in 4QFY26/FY26.

* We raise our earnings estimate by 3%/5% for FY27/FY28, factoring in

1) limited competition product pipeline for the US market,

2) enhanced efforts to benefit from Semaglutide opportunities

3) a reduction in effective tax rate estimate. We value ALKEM at 28x 12M forward earnings to arrive at our TP of INR5,840.

* The company ended FY26 on a strong note with 13.5%, 20%, and 18% YoY growth in revenue, EBITDA, and PAT, respectively. Having said this, we expect moderation in the earnings growth trajectory over the next two years due to operational costs related to biosimilars for the US market, efforts towards improving growth prospects of the Occlutech business, and a step-up in tax rate from 18% in FY26 to 27-28% in FY27.

* Considering stable earnings over FY26-28 and valuation (29x FY27E/26x FY28E earnings), we reiterate our Neutral rating on the stock.

International business drives growth; gradual revival in DF

* Domestic formulation (DF) business grew 8.9% YoY to INR23.2b. (64.5% of sales).

* International business grew 26% YoY to INR12.2b for the quarter.

* Within international business, US sales grew 26% YoY to INR7.7b (21.3% of sales).

* Other international sales grew 24% YoY to INR4.5b (12.6% of sales).

Reiterate Neutral

* We raise our earnings estimate by 3%/5% for FY27/FY28, factoring in 1) limited competition product pipeline for the US market, 2) enhanced efforts to benefit from Semaglutide opportunities, and 3) a reduction in effective tax rate estimate. We value ALKEM at 28x 12M forward earnings to arrive at our TP of INR5,840.

* The company ended FY26 on a strong note with 13.5%, 20%, and 18% YoY growth in revenue, EBITDA, and PAT, respectively. Having said this, we expect moderation in the earnings growth trajectory over the next two years due to operational costs related to biosimilars for the US market, efforts towards improving growth prospects of the Occlutech business, and a step-up in tax rate from 18% in FY26 to 27-28% in FY27.

* Considering stable earnings over FY26-28 and valuation (29x FY27E/26x FY28E earnings), we reiterate our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041