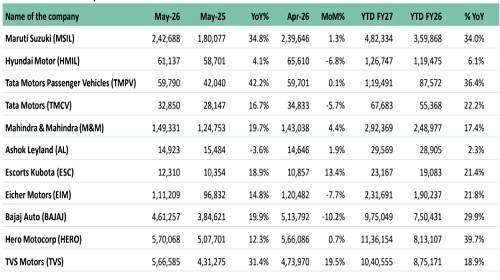

Monthly Auto Sales Update- June 2026 by ARETE Securities Ltd

Auto industry volumes rose 2% MoM and 21% YoY in May, with broad-based strength across segments sustaining the

momentum from April. 2W volumes continued to lead, supported by rural demand recovery, scooter outperformance and

strong export traction, particularly at TVS and HERO. PV dispatches were largely flat MoM (-0.3%) at record levels, with

MSIL and TMPV driving 28% YoY growth on the back of UV-led domestic demand and robust exports. CV volumes declined

1% MoM, though 11% YoY growth held, with TMCV leading on SCV and passenger carrier strength. Tractor dispatches rose

5% MoM and 22% YoY, aided by timely Rabi harvesting and favourable terms of trade. Exports maintained a ~24% share of

industry volumes, growing 33% YoY, led by TVS, BAJAJ and MSIL. Near-term, the outlook is shaped by competing forces,

with four rounds of fuel price hikes since mid-May (+8-9% in petrol/diesel) and IMD's revised monsoon forecast at 90% of

LPA (60% probability of deficient season) could weigh on rural sentiment and CV demand, while sustained urban PV

demand and EV adoption may provide partial offsets.

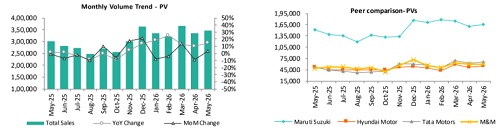

PV Segment

PV domestic dispatches rose 28% YoY but were flat MoM, with record volumes led by UV-driven growth at MSIL and strong Nexon/Punch-

led traction at TMPV. MSIL's Mini segment extended its post-GST revival to a seventh consecutive month of annual growth, while UV

volumes hit fresh highs on the back of Victoris, Brezza and Grand Vitara. TMPV's EV dispatches reached a new monthly peak, with forward

bookings up 3.5x YoY, reinforcing its lead in the sub-â‚115 lakh EV segment. M&M's SUV domestic growth of 9% YTD has lagged peers,

constrained by supplier manpower shortages rather than demand softness, with capacity expansion to 82k units/month in H2 FY27 a key

catalyst. Exports rose 20% YoY, led by MSIL, which accounted for ~75% of PV exports.

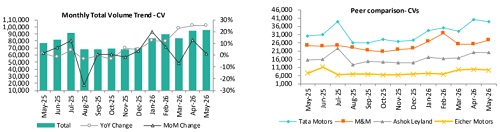

CV Segment

CV dispatches rose 11% YoY but declined 1% MoM, reflecting sequential moderation across sub-segments. TMCV led with domestic

volumes up 19% YoY, supported by SCV cargo and pickup (+30% YoY) and passenger carriers (+21% YoY), though HCV and ILMCV trucks

saw sequential moderation. M&M's CV domestic volumes grew 13% YoY, while EIM's domestic truck dispatches rose 13% YoY and MoM,

led by the LMD segment. AL's total volumes declined 4% YoY, with domestic M&HCVs down 11% YoY, impacted by a 35% fall in Buses, while

LCVs provided a partial offset at +13% YoY. Near-term, rising diesel costs and early signs of stress in freight activity could weigh on fleet

operator sentiment and replacement demand, particularly in the HCV segment.

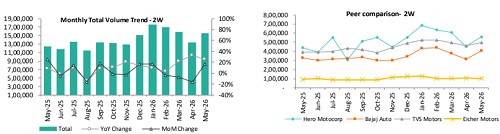

2W Segment

2W volumes rose 2% MoM and 20% YoY, with scooters continuing to gain share over motorcycles, driven by urbanization and accelerating

EV adoption. The e-2W segment recorded 1.7 lakh VAHAN registrations (+63% YoY), its second-highest month ever, as petrol price hikes

in the second half of May visibly accelerated demand, with H2 May retail volumes 57% higher than H1 May. TVS, BAJAJ and HERO

reported e-2W volumes of 42k/39k/19k units respectively, holding market shares of 25%/23%/11%. Exports in the segment grew 37% YoY,

led by TVS and BAJAJ, though sequential export momentum moderated at BAJAJ. If fuel prices rise further, given OMCs are still under-

recovering, the TCO shift toward e-2Ws could sustain through Q1 FY27, though a below-normal monsoon may weigh on rural ICE 2W

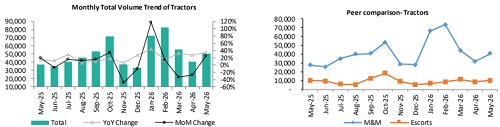

Tractor Segment

Tractor dispatches rose 5% MoM and 22% YoY, driven by timely Rabi harvesting, favourable terms of trade for farmers and sustained rural

demand. M&M's domestic tractor volumes grew 23% YoY and 3% MoM to 48k units, with ESC's domestic dispatches also rising 23% YoY and

14% MoM. Export volumes were mixed: M&M exports increased 7% YoY but declined 8% MoM, while ESC exports fell 35% YoY & 8% MoM.

key near-term risk to Kharif sowing and farm sentiment. A significant rainfall deficit could compress farmer incomes and weaken

replacement demand in H2 FY27, particularly if accompanied by higher input costs from elevated fuel and fertiliser prices.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127

.jpg)