IT Sector Update : Stabilizing amid AI and productivity challenges by Elara Capital

The Nifty IT Index has corrected 23% since 3 February 2026, with large-cap & mid-cap IT stocks having corrected 20% and 21%, respectively. Market prices have since stabilized, as concerns of India’s IT companies losing significant business to new firms and AI tools appear to have subsided. That said, IT companies continue to grapple with “productivity pass-through” pressures. Clients continue to demand higher productivity gains not just from new contracts but also from existing ones as per our understanding. This dynamic is poised to drive revenue deflation in the near to medium term for companies. However, we expect IT companies to optimize costs by further moderating hiring, and emphasizing revenue per employee productivity, which should stabilize profitability. Our tops picks are INFO from the large-cap space and MPHL from our mid-cap space.

AI productivity 1-3% deflation risk: IT companies face potential revenue deflation from AI led productivity gains in the near to medium term. IT companies with higher exposure to time & materials (T&M) contracts will likely feel the most impact in our view. T&M contract mix is around 46-52% for the companies which report this data. AI-driven revenue compression varies by the extent of productivity pass-through to clients. Based on our calculations, companies with 50% mix of T&M contracts could see portfolio-level deflation in the range of 1-3%. We have not factored any impact of AI deflation in our estimates.

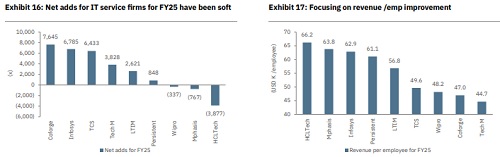

No material margin improvement in the near term: The IT industry is undergoing a structural shift from effort-based models to non-linear growth models. Future hiring is unlikely to track revenue growth, as companies prioritize productivity improvement like revenue per employee. Moreover, key margin levels are largely exhausted as Last Twelve Months (LTM) attrition has already hit multi-year lows (while most are running at high utilization). Subcontracting cost is moderating for most companies, so these tailwinds won’t drive material margin improvement in the near term.

INFO and MPHL remain our top picks: We favor INFO in the large cap space for its stable management, top revenue per employee among large caps in the past four years, No 1 ranking in the Forrester Wave AI technical Services Q4CY25 report in terms of strategy. It also offers superior low double-digit earnings growth vs peers during FY26-28E. At ~16x FY28E earnings, valuation remains attractive. We value INFO at 19x FY28E earnings to arrive at a lower TP of INR 1,600 per share. In the mid-cap space, MPHL stands out amid robust technology spending across BFSI (US top banks tech spend up 9% YoY in Q4CY25). With 60%+ revenue mix from BFSI, it is well-positioned. We expect an CAGR earnings of 16.5% during FY26-28E; the stock trades at 17x FY28E earnings, and we value it at 21x on FY28E earnings to arrive at a lower TP of IN 2,760 per share.

Please refer disclaimer at Report

SEBI Registration number is INH000000933