Insurance Sector Update: Getting healthier by Kotak Institutional Equities

Getting healthier

A combination of strong protection growth, a shift to non-par, lowered GST hit and low APE base is a near-term tailwind for life companies. On the flip side, solvency depletion is rapid in some cases. In the non-life business, the health business remains strong, coupled with the rangebound claims ratio. However, competition between players, especially in multi-channel insurer formats, is getting intense amid the expected cap on commissions. SBI Life, Star Health and PB Fintech are names we prefer.

Life insurance: Multiple near-term tailwinds

We find tailwinds to the margins of life insurance companies with an increasing share of non-par/annuity, supported by the upward sloping yield curve, following a recent rise in bond yields. Protection growth remains strong; Exhibit 2 shows that growth in sum assured was 52-167% for listed life companies in 3QFY26 and 36-124% in January 2026. The drag of GST (due to ITC loss) is waning faster than expected (Exhibit 4). All of this points toward strong VNB growth in the near term, driving upgrades after the 3QFY26 results (Exhibit 25). 2HFY25 was a weak period following surrender value guidelines; the low base is now providing a boost.

Competition intense, what happens next?

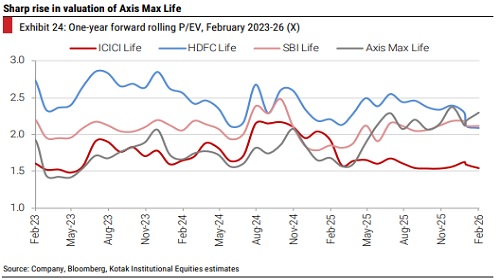

Competition, especially among multi-insurer banks/distributors, remains intense. Activation of the parent bank and the addition of new banks have driven strong bancassurance growth for SBI Life and Axis Max Life, respectively. HDFC Life fared weakly at the parent bank. Market sources suggest mixed feedback of various distribution channels accepting commission haircuts due to ITC loss on account of GST. All eyes are on guidelines on commission caps likely drafted shortly and implemented from April 2026. Prima facie, we do not expect severe disruption, which otherwise poses a risk to growth for the entire sector. Nevertheless, we expect competitive intensity to mellow down as distributors leverage volume tailwinds.

Healthy way forward

We are becoming more assertive of health insurance companies as the claims ratio remains under control and growth accelerates. Exhibit 35 shows that SAHIs reported 18% GWP growth in retail health in 3QFY26, which continued to 33% in January 2026. Negotiations with hospitals during the quarter also suggest that medical inflation will likely remain under control. Valuations, based on IFRS financials, are not demanding for listed SAHIs. On the other hand, the motor business has seen lower GWP growth (than volume growth reported by OEMs) due to price deflation and intense competition in motor OD; tariff hikes will determine the growth trajectory in motor TP.

Solvency: Interplay of strong growth, protection and RBC

norms High growth tailwinds on term/protection business have prompted many insurance companies to raise subordinate capital. Exhibit 5 shows solvency trends across companies; the ratio is depleting rapidly for select players, some of whom may require capital. A framework for risk-based solvency capital (RBC) is expected shortly, which will drive further capital consumption or release. Focus may also likely shift to IFRS, which is expected to be implemented in March 2027E.

APE growth improves in 3Q, momentum broad-based after GST

APE growth picked up meaningfully in 3QFY26 for the private sector, supported by (1) a low base after surrender value guideline implementation in 3QFY25 and (2) strong tailwinds from GST exemption on life insurance premiums.

SBI Life and Axis Max Life delivered strong acceleration, driven by the revival in bancassurance and agency, respectively. HDFC Life’s growth remained moderate, constrained by continued weakness in the bank channel, despite healthy agency performance. ICICI Prudential Life showed early signs of recovery, with APE turning positive after three consecutive quarters of decline. LIC reported a sharp rebound, aided by a low base and strong GST-led demand.

Sum assured growth remained elevated, significantly outpacing APE growth, reflecting (1) strong traction in retail protection, (2) higher rider attachment and (3) improved ticket sizes across savings products. Post-GST demand trends have clearly strengthened, though sustainability beyond 4QFY26E remains the key monitorable.

Above views are of the author and not of the website kindly read disclaimer

Tag News

Life Insurance Sector Update : New business in Jul-26 - Slowdown in growth momentum by Emkay...