Indian Debt Capital Market - Can it Finance India`s Growth? by CareEdge Ratings

Synopsis

• India’s corporate bond market remains underdeveloped and overshadowed by bank lending and government securities, with a relatively low share in GDP and the overall debt market.

• The market has grown steadily over time, supported by regulatory measures, but issuances remain sensitive to policy changes and interest rate movements. A major limitation is the concentration of issuances in highly rated instruments and sectors such as BFSI, with limited participation from lower-rated issuers.

• Investor participation is dominated by domestic institutions, with relatively low foreign involvement and an underdeveloped secondary market with limited liquidity.

• Despite these challenges, opportunities exist to deepen the market through regulatory reforms, broader issuer and investor bases, improved liquidity, and greater participation in mid- and lower-rated bonds offering attractive risk-reward profiles.

Corporate Bond Market in India Remains Underpenetrated Compared to Other Countries

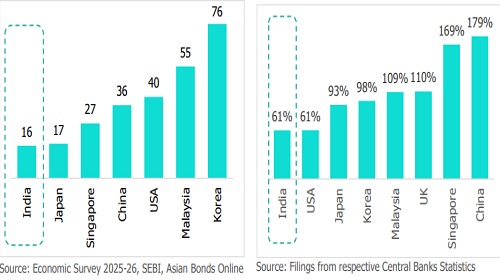

Figure 1: Outstanding Corp. Bonds as % of GDP Figure 2: Outstanding Bank Credit as % of GDP

India’s debt ecosystem reflects a structurally shallow and bank-dominated financial system. Bank credit to GDP stands at around 61%, significantly below peer Asian economies such as China (179%), Japan (93%), and Korea (98%), indicating relatively low credit intermediation. Within this broader context, the corporate bond market remains underdeveloped in both scale and participation. Corporate bonds account for roughly 21% of the total debt market, underscoring the large presence of government securities and the continued reliance on bank financing. In terms of economic size, the corporate bond market represents only about 16% of GDP, substantially lower than China (36%) and the United States (40%). This disparity highlights the smaller role of market-based financing in India compared to more advanced economies. Participation metrics further reinforce this structural gap. The ratio of debt-issuing companies to equity-listed firms in India is approximately 13%, significantly below the 25% observed in the United States, pointing to a narrower issuer base and lower market access. Collectively, these indicators suggest that India’s financial system remains less financialised, characterised by constrained capital market depth and a strong preference for bank-led intermediation. The relatively low penetration of the corporate bond market is therefore both an outcome of and a contributor to this structural imbalance.

Corporate Bonds represent approximately a fifth of India’s Debt Market

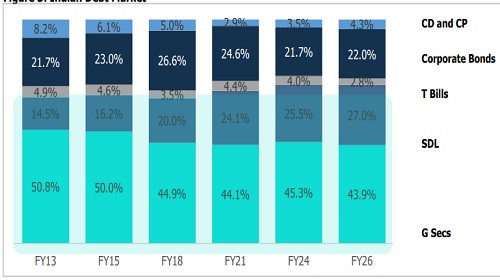

Figure 3: Indian Debt Market

India’s debt market is dominated by government securities, with corporate debt accounting for a relatively small share. Corporate bonds account for roughly 20–25% of the total debt market, while the remaining 75–80% consists mainly of central and state government borrowings. The limited share of corporate debt also reflects structural challenges, including lower credit penetration, reliance on bank financing, and investor preference for safer government instruments

Corporate Bond Market Has Witnessed Steady Growth; Strong Issuance and Outstanding Volume

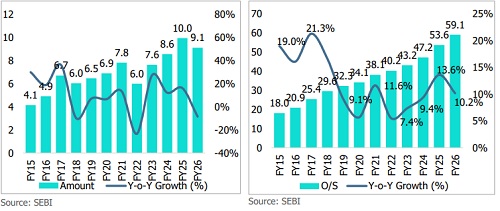

Figure 4: Movement in Corporate Bonds Issuance (Rs lakh crore) Figure 5: Movement in Corporate Bonds Outstanding (Rs lakh crore)

India’s corporate bond market has experienced steady expansion over time, though annual issuances have been influenced by regulatory changes and interest rate cycles. Bond issuances increased in FY25 following the RBI’s FY24 decision to raise risk weights on bank lending to NBFCs, encouraging a shift toward market-based borrowing.

However, issuances moderated in FY26 after the rollback of these measures in April 2025, combined with a hardening interest rate environment. Despite such fluctuations, issuances have grown at a stable CAGR of around 7.4% over the past 12 years.

The growth in outstanding corporate bonds has been even more pronounced, reflecting sustained market deepening. In absolute terms, the market has grown significantly from around Rs 18 lakh crore in FY15 to nearly Rs 59 lakh crore in FY26, underscoring consistent long-term expansion. Outstanding volumes have expanded at a CAGR of approximately 11%, exceeding nominal GDP growth of about 10% over the same period. Overall, while issuance activity remains sensitive to policy shifts and yield movements, the sustained rise in outstanding volumes points to a gradual strengthening and deepening of India’s corporate bond market.

Above views are of the author and not of the website kindly read disclaimer

Tag News

Market Round-up - 3rd August 2026 by Motilal Oswal Wealth Mangement