India GDP :Services momentum drives Q4; FY27E at 6.3% amid headwinds by Emkay Global Financial Services Ltd

Q4 GDP growth at 7.8% was primarily driven by strong growth in Services, while Industry growth slowed, led by Manufacturing (possibly due to the impact of the West Asia crisis). GFCF growth saw a sharp improvement, despite a YoY decline in general government capex, which may indicate a pick-up in private capex. For FY26, GDP growth at 7.7% was higher than the second advance estimate, helped by healthy Services and Manufacturing (despite US tariffs). On the expenditure front, fiscal and monetary easing helped improve private consumption, while GFCF rose on the back of strong government capex. While this data indicates strong momentum heading into FY27, headwinds for growth loom. The West Asia crisis is likely to materially hurt manufacturing output in Q1 due to higher input costs and lower energy availability. Private consumption would also be hit after retail fuel price hikes. With average Brent forecast of USD90/bbl, potentially weaker monsoons amid El Niño, and an unfavorable base effect, we maintain our FY27 real GDP forecast at 6.3%.

Q4FY26 GDP growth at 7.8%, led by Services and private capex pick-up

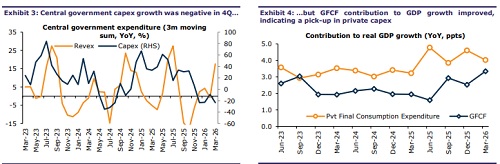

Q4FY26 GDP growth was 7.8% (Emkay: 7.4%), notching higher than the implied FY27 second advance estimate (7.4%). Nominal GDP growth came in at 9.1%. GVA growth was at 7.9%, led by extremely strong growth in Services (9.9%). Within Services, growth remained substantial for Trade, Hotels, etc (12.5%) and Financial, Real Estate, etc (10.4%), while Public Admin, Defense etc, stayed muted at 5.8%. Industry growth slowed to 7.3% vs 9.5% in 3Q, led by slower Manufacturing growth (7.3% vs 12.8% prior). This likely reflects some of the impact of higher input costs and lower energy availability in March following the West Asia crisis. Construction growth improved to 8.4% (vs 6.7% prior), while Electricity and other Utilities rose to 4.1%. Agri growth improved sequentially to 3.6% on the back of a healthy rabi harvest. On the expenditure front, private consumption growth was healthy, albeit lower sequentially (7.1% vs 8.2% prior), while government consumption was at 4.9%, reflecting an improvement in general government ex-interest revex growth in Q4 (7% YoY vs -4% prior). GFCF growth improved to 10.8% (8.2% prior), but with general government capex declining 8% YoY in Q4. This may reflect a pick-up in private capex. We note that data for prior quarters has been revised upward marginally.

Healthy govt capex and private consumption drive FY26 GDP growth to 7.7%

The healthy Q4 print, along with upward revisions for previous quarters, means that FY26 GDP growth was at 7.7% (vs second advance estimate of 7.6%), with nominal GDP growth at 8.9%. GVA growth at 7.9% was largely on account of a healthy improvement in Services growth (9% vs 7.9% in FY25). This was led by higher growth in Trade, Hotels, etc (10.1%), while Financial, Real Estate, etc, stayed flat at 9.9%, and Public Admin, Defense, etc, rose to 5.8%. Industry growth was stable at 8.5%, with Manufacturing rising to 10.7% despite the US tariff hit for nearly half of FY26. Electricity and other Utilities slowed to 1.7% and Construction was flat at 7.4%. Agri growth slowed to 3%. On the expenditure side, private consumption picked up to 7.7%, likely aided by the impact of monetary and fiscal easing, while government consumption slowed to 5.5%. GFCF growth picked up to 8.2% (FY25: 6.4%), reflecting much higher general government capex growth (~16% vs FY25: ~5%). Net exports remained a marginal contributor, with export growth at 6.3% and import growth at 5.6%.

FY27E GDP growth at 6.3%, with higher oil prices and weak monsoon

While these numbers indicate strong growth momentum being carried into FY27, the West Asia crisis will have a material impact on growth, with 1QFY27 likely to see the manufacturing sector bearing the brunt of higher input costs and lower energy availability. Services, especially the informal sector, may also see slower growth amid these headwinds, while consumption will also take a hit with the hike in retail fuel prices. With average Brent price forecast of USD90/bbl, the prospect of weaker monsoons amid the El Niño effect, and an unfavorable base effect, we maintain FY27E real GDP forecast at 6.3%. However, real GVA growth is likely to be higher at 6.5%, accounting for lower net indirect taxes, with higher subsidies and possibly lower indirect tax collections.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354