Gold - The Quiet Conviction- — An observation report based on WGC Central Bank Gold Survey, 2026 note by Chirag Mehta, CIO , Quantum AMC

Since 2018, the same questions have anchored the annual conversation with central banks: how much gold they hold, why, where it sits, and what comes next. This year, the answers landed differently. Fieldwork ran by World Gold Council, between February and May 2026, with the bulk of responses gathered after the Middle East conflict erupted, so the data captures a live moment of geopolitical stress rather than the usual slow accretion of institutional consensus.

* Observation — The Relentless Climb

Intent to accumulate gold by central banks has climbed steadily, from 9% in 2019 to 45% in 2026, holding its upward trajectory through COVID (2020–21), the post-Ukraine reserve shock (2022), the inflation cycle (2023), and record prices (2024–25). That persistence across such varied conditions suggests this isn’t a reaction to price or to any single event, but more consistent with a gradual reweighting of gold’s role in reserve portfolios. The divergence beneath the headline number is telling: 53% of Emerging Market & Developing Economies (EMDE) central banks plan to add gold in the next year, against just 18% of advanced-economy banks. That 35-point gap points to differing motivations as much as differing wealth – (EMDE) Central Banks increasingly treating gold as a lever for monetary autonomy, advanced-economy banks still largely holding it as legacy reserve. Overall, the numbers look very supportive for gold for 2026.

* Observation II — The Dollar Sentiment Shock

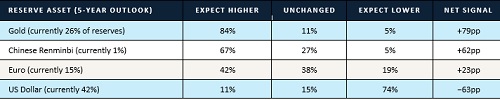

Dollar sentiment shifted sharply: banks expecting a smaller dollar share of reserves in five years rose from 45% to 74% in a year, a 29-point jump too large for gradual drift, pointing to a specific catalyst. Behaviour backs this up: two decades of steady dollar reduction alongside recent gold accumulation suggest decisions already in motion. In short, this isn’t a comment on these central banks’ own finances, it’s caution about the dollar’s home economy. The shift rest on geopolitical tension, sanctions exposure, US fiscal and debt trajectories, and trade fragmentation – external factors rather than any weakness in the economies doing the diversifying. The reading held even after “de-dollarisation” was dropped as a response option in 2025: two-thirds of prospective buyers in 2026 still cited “higher economic risks in reserve currency economies”. The same concern, minus the label.

* Observation III — What Crisis Does to Gold’s Rationale

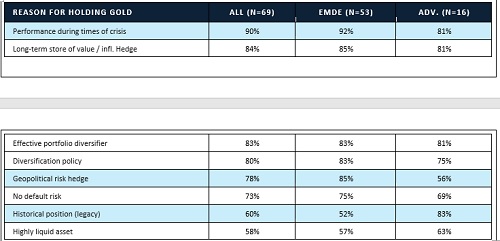

Crisis performance is now the top-cited reason for holding gold with 90% of respondents, the highest in nine years. The timing matters as most responses came in after the Middle East conflict began, so this is reserve managers observing gold’s crisis behaviour live, not recalling it from theory. The same EMDE – advanced economy split shows up here too. EMDE banks lean heavily on gold as a geopolitical risk diversifier (85% vs. 56%), echoing the sanctions and external-financing concerns already visible in their dollar-diversification stance. Advanced economies, by contrast, still anchor their reasoning in legacy holdings (83% vs. 52%) – gold as inheritance rather than active strategy. The pattern holds: one group is building a forward-looking case for gold, the other is justifying what it already has.

* Observation IV — Geopolitics Overtakes Inflation for the First Time

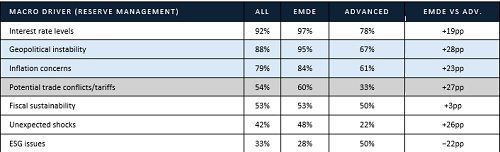

Geopolitical instability has overtaken inflation as the top concern shaping reserve decisions (88% versus 79%, a first in the survey’s history), signalling an addition from economic to structural risk. The EMDE – advanced economy split persists here too: 95% of EMDE banks flag geopolitical instability, consistent with the sanctions and external-vulnerability concerns already running through their gold and dollar positioning. Trade conflicts and tariffs, a risk factor only since 2025, already register 54%, reinforcing the trade-fragmentation thread noted earlier. Across nearly every risk category, EMDEs report higher concern than advanced economies, the same resilience-driven posture, underscoring a stronger emphasis on resilience and risk mitigation.

* Observation V — When Silence Speaks: The Vault as a Political Statement

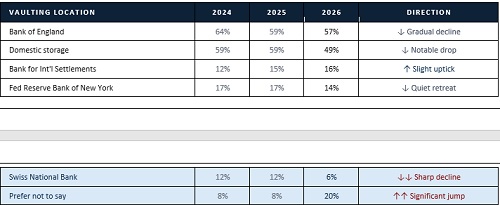

The clearest signal in the 2026 survey isn’t where central banks store their gold, but their growing reluctance to disclose it. “Prefer not to say” responses rose from 8% to 20% despite record participation, suggesting deliberate discretion rather than missing data. At the same time, reported storage at the Swiss National Bank fell from 12% to 6%, the New York Fed’s share continued to decline, and reported domestic storage eased to 49%.

Country-level developments paint a clearer picture than the survey responses, particularly after the 2022 freeze of Russia’s foreign reserves. France repatriated 129 tonnes from the New York Fed, raising domestic custody from 95% to 100%; Serbia brought back its entire ~40-tonne reserve; and Nigeria initiated partial repatriation. At the same time, several central banks accumulated gold while expanding domestic custody. India added ~200 tonnes while repatriating 274 tonnes, increasing domestic custody from 38% to 77%; Poland acquired ~300 tonnes while continuing the repatriation of 100 tonnes from the Bank of England; and the Czech Republic has tripled its domestically held gold since end-2022 while initiating repatriation. This stands in contrast to the survey, where many respondents expect domestic storage to decline. The divergence, coupled with the sharp rise in central banks choosing not to disclose vaulting locations and falling western vault storage suggests that sovereign control over gold is becoming a higher strategic priority. Central banks are not just accumulating more gold; they are increasingly choosing to keep it at home.

* Observation VI — From Passive Store to Active Instrument

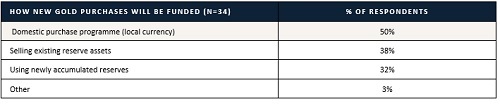

Among the 37% of central banks actively managing gold reserves, the objective has flipped from return-seeking to defence: risk management as the stated motive nearly doubled (22% to 42%), while tactical trading faded. The tools reflect that posture. Eleven central banks are now exploring gold-for-collateral swaps, a way to access foreign-currency liquidity if conventional funding channels seize up, a direct alternative against the sanctions and external-financing risks raised earlier. More striking: half of all prospective buyers plan to fund purchases through domestic programmes settled in local currency, meaning a growing share of gold accumulation needs no foreign exchange at all. Taken together, the shift points toward a more self-contained reserve model, built on domestic gold, local currency, and local custody, that owes less to the global financial system.

Concluding Observation — The Demand Architecture for Years Ahead

Stepping back from the individual findings, the nine-year evolution of the CBGR Survey shows gold has transitioned from a niche reserve preference to a mainstream strategic asset. The 2026 survey reinforces this shift through rising expectations for higher gold allocations, expanding domestic purchase programmes, and the increasing use of gold in active reserve management via deposits, swaps, and collateral operations. Together, these trends indicate that central bank gold demand is structural, not cyclical. It has endured a decade-long US equity bull market, multiple interest-rate cycles, a global pandemic, and major geopolitical conflicts, with conviction only strengthening. The 2026 survey captures this inflection point: geopolitical instability has overtaken inflation as the top reserve management concern, confidence in the US dollar has weakened, and faith in gold's crisis performance has reached a record high. Reflecting this shift, 89% of respondents expect global central bank gold reserves to increase over the next 12 months.

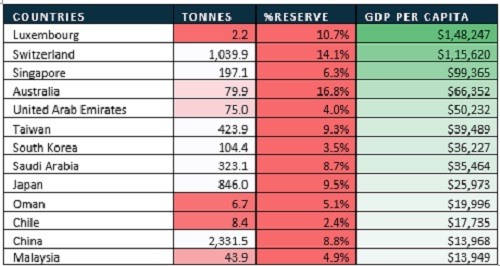

Even as the structural demand from active accumulators remains firmly in place, the survey's demand outlook may carry a second, underappreciated dimension. The economies that have not yet acted but carry the conditions that make accumulation increasingly difficult to defer. Several high-income sovereigns still hold only a small share of their reserves in gold (as shown in the table above), despite having sophisticated reserve portfolios capable of greater diversification. This is notable as gold has proven critical during crises and as 74% of central banks expect it to gain at the dollar's expense over the next five years. Against a decade of successive shocks - a global pandemic, the weaponisation of Zreserve currencies, sustained geopolitical fracture, and the sharpest single-year deterioration in dollar sentiment, the cost of that inaction is rising. The foundations for the next wave of central bank gold demand may already be visible in what these institutions have not yet done.

Above views are of the author and not of the website kindly read disclaimer

_Securities_(600x400).jpg)