Downgrade to Sell Anand Rathi Wealth Ltd for the Target Rs 1,700 by Motilal Oswal Financial Services Ltd

In-line PAT excluding one-time impacts

* Anand Rathi Wealth (ARWM) reported revenue from operations of ~INR3.2b in 1QFY27 (in line), growing 18% YoY/12% QoQ, primarily driven by a 19%/16% YoY growth in revenue from the distribution of financial products/MF.

* Operating expenses for 1QFY27 grew 46% YoY to INR2.1b, with employee costs growing 53% YoY to INR1.8b (18% higher than est.) due to a onetime impact of ESOP expenses. Other expenses grew 18% YoY to INR372m. EBITDA came in at INR1.1b (27% miss), declining 15% YoY, with EBITDA margin at 33.7% (vs our estimate of 44.5%) in 1QFY27 (46.6% in 1QFY26).

* For 1QFY27, consolidated PAT stood at INR1.6b (+74% YoY), reflecting a 39% beat. Excluding the one-time impacts of fair value gains on investments, ESOP expenses, and the related combined tax effects, PAT came in at INR1.2b (+24% YoY and in line with our est.).

* The company achieved 24% of FY27 revenue guidance and 25% of FY27 PAT guidance in 1QFY27, with management reiterating confidence in meeting full-year targets. Management indicated that only 1–2bp of TER changes may have been passed on by AMCs. The company's mutual fund distribution market share expanded significantly, with net flow market share increasing to 2.47% in FY26 from 0.18% in FY20.

* We have broadly maintained our earnings estimates for FY27/28, considering the impact of ESOP expenses is offset by fair value gains on investments. We expect AUM/Revenue/PAT to expand at a CAGR of 24%/22%/18%, respectively, over FY26-28E. While the flow momentum is expected to remain stable, the stock is currently trading at an FY28E P/E of 64x, which appears stretched. Hence, we are downgrading our rating to SELL, with a one-year TP of INR1,700, based on 50x FY28E EPS.

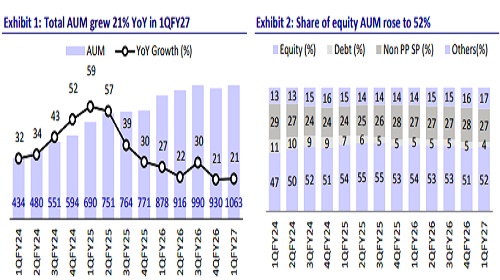

Flow momentum declines in 1QFY27

* Total AUM grew 21% YoY/14% QoQ to ~INR1.1b. The share of equity MFs in the overall AUM mix was 52%. Private Wealth/Digital Wealth AUM grew 21%/23% YoY to ~INR1t/INR25.3b, respectively, in 1Q.

* Total quarterly net inflows/equity flows declined 28%/4% YoY to INR27.4b/INR19.0b (the lowest since 2QFY25).

* Monthly SIP flows for Jun’26 increased 25% YoY to INR940m.

* The share of customers with AUM of over INR500m has increased to 30.1% in 1QFY27 from 26.9% in 1QFY26. The company onboarded 546 net new client families in 1Q, taking the total count to 13.9k families.

* Operating expenses for 1QFY27 grew 46% YoY to INR2.1b, with employee costs growing 53% YoY to INR1.8b (18% higher than est.) due to a onetime impact of ESOP expenses. Other expenses grew 18% YoY to INR372m.

* Other income for the quarter came in at INR1.1b vs INR102m in 1QFY26 (our est. of INR190m) due to fair value gains on investments. This resulted in a PBT of INR2.1b (+63% YoY).

* The company reported one of the lowest client attrition rates in the industry, with only 0.09% of AUM lost in 1QFY27. It also recorded one of the lowest regret RM attrition rates in the industry, with no exits among RMs managing AUM of over INR400m. Additionally, the company has retained about 90% of AUM associated with the RM attrition witnessed in 3QFY26.

* AUM per RM increased to INR2.5b in Jun’26 from INR2.2b in Jun’25, driven by the continued association of RMs with the organization. Additionally, clients per RM improved to 33 from 32 in 1QFY26.

* The digital wealth business client count increased 23% YoY, reaching 7,320 in 1QFY27 vs 6,284 in 1QFY26.

Valuation and view

* ARWM is one of the few companies in the listed space that has consistently met its stated guidance. For FY27, management has guided for revenue/PAT of INR14.2b/INR4.6b vs. our estimates of INR14.1b/INR4.6b.

* We have broadly maintained our earnings estimates for FY27/28, considering the impact of ESOP expenses is offset by fair value gains on investments. We expect AUM/Revenue/PAT to expand at a CAGR of 24%/22%/18%, respectively, over FY26-28E. While the flow momentum is expected to remain stable, the stock is currently trading at a FY28E P/E of 64x, which appears stretched. Hence, we are downgrading our rating to SELL, with a one-year TP of INR1,700, based on 50x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412