Buy TCS Ltd for the Target Rs 2,350 by Motilal Oswal Financial Services Ltd

Halting the slide Short-term commentary better than expected, long term still uncertain

* TCS reported 1QFY27 USD revenue of USD7.6b, up 0.4% QoQ in CC and above our estimate of flat QoQ CC growth. 1Q growth was led by Hi-tech/ BFSI/regional markets, up 1.7%/1.6%/4.0% QoQ cc, while consumer/ healthcare fell 4.0%/1.0% QoQ cc. EBIT margin was 24% (down 130bp QoQ), in line with our estimate of 23.9%. Adj PAT was up 1% QoQ/8.6% YoY at INR139b, above our est. of INR136b.

* In INR terms, 1QFY27 revenue/EBIT/adj. PAT grew 13.9%/11.6%/8.5% YoY. Cash flow from operations stood at 93% of net profit for 1QFY27. In 2QFY27, we expect revenue/EBIT/adj. PAT to grow 10%/8.4%/9.3% YoY. TCS reported a deal TCV of USD9.5b, down 20.8% QoQ and up 1.1% YoY. The book-to-bill ratio stood to 1.2x. We reiterate our BUY rating on TCS with a TP of INR2,350, implying a 15% potential upside.

Our view: 2Q to see improvement; AI deflation questions remain

* TCS expects demand to improve in 2Q, supported by a pent-up technology backlog and stronger client conversations. While we also expect 2Q to be better, we believe evidence around demand improvement is scant. The pent-up demand narrative has been around for some time, while geopolitics, tariff uncertainty and cautious discretionary spending continue to weigh on decision-making. We continue to expect FY27 demand to remain muted. Commentary, however, is better than we expected.

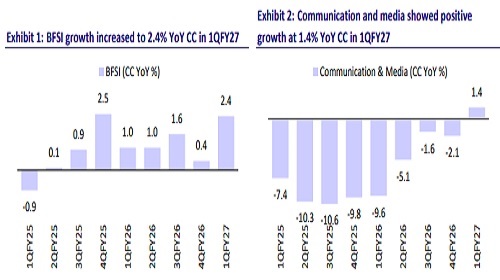

* BFSI continues to hold up well, while management expects Manufacturing and Life Sciences to recover in 2Q on the back of improving conversations and recent deal wins. Technology & Services vertical also remains healthy. However, Consumer continues to face pressure, particularly in airlines and discretionary retail in North America, with geopolitical uncertainty delaying spending recovery.

* 1Q EBIT margin declined 130bp QoQ to 24.0%, impacted by a 170bp wage hike, along with continued investments in AI partnerships, talent and sales, partly offset by ~40bp of currency benefits and operational efficiencies. While the wage hike impact will reverse, we expect investments in sales, AI capabilities and partnerships to remain elevated. Accordingly, we cut our FY27E EBIT margin estimate by 30bp.

* Management acknowledged 10-15% AI-led productivity pass-throughs as projects come up for renewal, although it argued that incremental client work has so far offset most of the revenue impact. We believe the full impact of AI deflation is still unfolding, and productivity gains are likely to continue getting passed on to clients over the coming quarters, keeping pressure on the existing book of business

* The market is pricing in anemic growth over the next 12-18 months: We continue to model ~2.5%/3.2% organic CC growth for FY27E/FY28E, assuming the current pace of AI-led deflation persists. On these assumptions, we see a limited downside to the stock, for now.

TCS 1QFY27 results: Beat on revenue (led by India business); margins in line with our estimates

* USD revenue came in at USD7.6b, up 0.4% QoQ in CC terms and above our estimates of flat QoQ CC.

* In terms of geographies, North America/Europe declined 0.4%/0.2% QoQ in cc, while India/Latin America/UK were up 7.6%/0.6%/0.3% QoQ cc.

* Annualized AI services revenue stood at USD2.6b in 1QFY27, up 13.6% QoQ. Core revenue (ex. AI) declined 1% QoQ in USD.

* 1Q growth was led by Hi-tech/BFSI/regional markets, up 1.7%/1.6%/4.0% QoQ cc, while Consumer/Healthcare declined 4.0%/1.0% QoQ cc.

* EBIT margin was 24% (down 130bp QoQ), in line with our estimate of 23.9%.

* TCS reported a deal TCV of USD9.5b in 1QFY27, down 20.8% QoQ but up 1.1% YoY.

* Adj. PAT was up 1.0% QoQ/8.6% YoY at INR139b (above our est. of INR136b).

* The net headcount rose by 9,279 employees to 5,93,798 (up 1.6% QoQ) in 1QFY27. Attrition (LTM) decreased by 10bp QoQ to 13.6%.

* FCF conversion to PAT stood at 93% in 1QFY27. The board declared an interim dividend of INR12/share in 1QFY27.

Valuation and view

* We expect USD revenue/EPS to compound at ~3%/~6% over FY26-28E. While management expects demand to improve in 2Q, we believe growth will continue to come from select pockets rather than a broad-based pickup. 1QFY27 commentary, however, is better than we expected. We have lowered our FY27 margin estimate by 30bp to reflect continued investments in AI capabilities, partnerships and sales. We keep our estimates unchanged and reiterate BUY with a TP of INR2,350, based on 15x FY28E EPS, implying ~15% upside

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd