Buy Indian Bank Ltd for the Target Rs 1,025 by Motilal Oswal Financial Services Ltd

Steady quarter; further strengthens provisioning buffer Margins improve QoQ

* Indian Bank (INBK) reported 1QFY27 PAT of INR32.7b, up 10% YoY (in line), as strong traction in other income was offset by higher-than-expected provisions (additional provision of INR10b on account of ECL provisioning).

* NII grew 17% YoY/5% QoQ (in line) to INR74.3b (our est. of INR73.7b). NIM improved by 6bp QoQ to 3.29%.

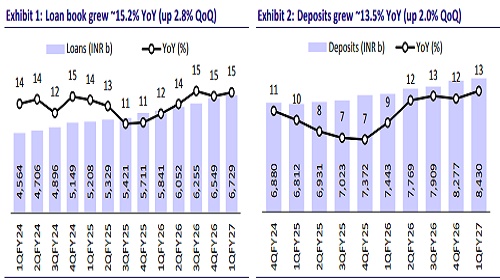

* Advances grew 15.2% YoY/2.8% QoQ, while deposits rose 13.5% YoY/2.0% QoQ. Consequently, the C/D ratio rose by 55bp to 79.7%. Domestic CASA was largely flat at 39.7%.

* Slippages declined to INR13b from INR14b in 4QFY26. The bank made additional floating provisions of INR10b for the ECL transition impact, with further residual provisions of INR20-25b expected to be made. GNPA ratio improved by 12bp QoQ to 1.86%. PCR stood at 92.2%.

* We fine-tune our earnings estimates and anticipate the bank to deliver FY28E RoA/RoE of 1.3%/18.2%. Reiterate BUY with the unchanged TP of INR1,025 (premised on 1.4x Mar’28E ABV).

Business growth steady; NIMs improve 6bp QoQ

* 1Q PAT of INR32.7b was up 10.1% YoY/5.5% QoQ (inline), as strong traction in other income was offset by higher-than-expected provisions (additional provision of INR10b on account of ECL provisioning)

* NII grew 17% YoY/5% QoQ to INR74.3b (in line). NIM improved 6bp QoQ to 3.29%. The bank expects NIMs to remain at 3.15-3.25%, with cost of funds expected to remain elevated.

* Other income rose by 8% YoY/5% QoQ to INR26b (8% beat), with strong recoveries from written-off accounts of INR7.6b. Total revenue, thus, rose 14% YoY/5% QoQ to INR1007b (3% beat). Treasury income improved to INR2.3b from INR60m in 4QFY26 as bond yields declined.

* Opex grew 12% YoY/4% QoQ to INR45.1b (2% higher than est.). C/I ratio remained flat at ~45%. PPoP grew 17% YoY/ 5% QoQ (3% beat) to INR55.6b.

* Advances grew by a healthy 15.2% YoY/2.8% QoQ to ~INR6.7t, led by retail MSME and Agri loans. Retail loans grew 18.7% YoY/3.8% QoQ. Within retail, gold loans grew 14.9% QoQ and housing grew 2.3% QoQ. Agri advances increased 3.5% QoQ, MSME rose 1.9% QoQ, and corporate grew 0.7% QoQ.

* Deposits grew 13.5% YoY/2.0% QoQ. Consequently, C/D ratio rose 55bp QoQ to 79.7%. CASA ratio was flat at 36.1%, with domestic CASA at 39.7%.

* Slippages declined to INR13b vs. INR14b in 4QFY26 and INR13.7b in 1QFY26. GNPA/NNPA ratios were up 12bp/flat QoQ at 1.86%/0.15%. PCR stood at 92.7%. Credit cost declined to 23bp in 1QFY27 from 47bp in 4QFY26, while the bank conservatively guides it to be 1%.

* SMA-2 book increased primarily due to one DCCO account; management expects normalization once the credit line is operational.

Valuation and view

INBK reported an in-line quarter, supported by strong traction in other income. NIM guidance remains unchanged at 3.15-3.25%, with management expecting to sustain margins at the upper end of the range. Management expects to keep a balance between loan and deposit growth, which would be closely monitored. The bank made additional floating provisions of INR10b for the ECL transition impact, with further residual provisions of INR20-25b expected to be made. On asset quality, slippages and credit costs came in lower, with asset quality improving across asset classes. The bank maintains a best-in-class PCR, providing comfort in incremental credit costs. Further, the transition to ECL is expected to have a manageable impact alongside minimal increase in steady-state credit costs. We fine-tune our earnings estimates and expect the bank to deliver FY27E RoA/RoE of 1.3%/18.2%. Reiterate BUY with an unchanged TP of INR1,025 (premised on 1.4x Mar’28E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412