Debt Market Watch 06th April 2026 by GEPL Capital

Government Security Market Update:

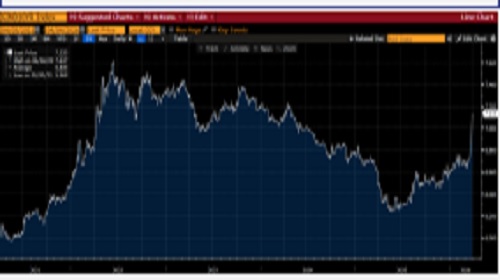

Indian government bond moved higher above 7.10% on the continued war escalation and higher crude oil prices. Brent crude oil jumped over 6% to $107 a barrel on Thursday. The yield rose 37 basis points in March and 45 bps in fiscal 2026 despite 100 basis points of rate cuts by the Reserve Bank of India. Bonds were caught in a sharp selloff across the country's markets that included surging swap rates, as investors weigh risks of the war in the Middle East widening further. That would pose significant challenges to economic growth and inflation for net energy importer India. The government released the borrowing calendar for the H1FY27 which was lower than the expectations and indicated that they will raise 8.20 trillion rupees amounting to 51% of its annual borrowing plan. Borrowing through so-called ultra-long bonds of 30 to 50 year duration will be lowered to 24.9% from 35% in April – September 2025 and 30% in October – March. As per the budget the government had pegged a record borrowing of 17.20 trillion rupees and multiple bond switch operations since then have lowered the borrowing to 16.09 trillion rupees. In the first auction of the FY27, the government raised Rs.29,000 crore by issuing two securities 6.68% GS 2040 & 7.09% GS 2074 at a yield of 7.5303 & 7.8812%respectively. The yield on the 6.48% Government bond due Oct 2035 rose to 7.1329% from 6.9419% last week

Global Debt Market Update:

Earlier this week, the U.S. Treasury rallied, pushing down yields, on comments from Fed Chair Jerome Powell that traders interpreted as dovish, and on hopes that the conflict in Iran could turn out to be less inflationary for the U.S. economy than previously feared. On Friday, however, yields retraced some of that move, climbing after a much-betterthan-expected March jobs report. The benchmark 10-year yield finishes at 4.344%, down from 4.439% last Friday. The 2 -year yield this week declined to 3.85% from 3.915% a week ago. Treasury yields rise and the dollar strengthens following a much stronger-than-expected March jobs report. Payrolls grew by 178,000 versus the 59,000 economists polled by WSJ expected. The unemployment rate edged down to 4.3% from 4.4%. Health care added 76,000 jobs last month. Employment in ambulatory health care services rose by 54,000, reflecting an increase of 35,000 in offices of physicians as workers returned from a strike. Retail sales in February were also better than expected, with the Commerce Department reporting that the headline sales number increased 0.6% in the period compared to the 0.5% gain that economists polled by Dow Jones had estimated. Australia's three-year yield was up about 50 bps for the month, the most in 17 months, despite easing more than 9 bps on Monday to 4.715%. Japan's two-year government bond yield was up 12.5 bps for March, after dipping 2 bps to 1.36%.

Bond Market Ahead:

Government bond yields are likely to remain elevated, weighed down by rising prices of crude oil and persistent supply pressures and the 10-year benchmark likely to head towards 7.20 to 7.25% range amid global uncertainties, which are likely to keep the rupee under pressure. Additionally a heavy supply of state development loans (SDLs) is seen exerting further upward pressure on yields owing to oil price shocks and geopolitical uncertainties. Yields are therefore, likely to remain under pressure in the first half. Sustained elevation in oil price could add to the strain. The market will turn it focus on the RBI MPC meet on April 8 and the Reserve Bank of India faces a limited but critical set of policy options in its April monetary policy as the Iran-linked West Asia conflict sharpens risks to inflation, growth and external stability. The most likely option before the Monetary Policy Committee (MPC) is to maintain status quo on the policy repo rate and stance. A pause would allow policymakers to assess the evolving impact of sharply higher crude oil and gas prices, supply chain disruptions and global financial volatility. With domestic growth still holding up and inflation yet to fully reflect the energy shock, a wait-and-watch approach preserves flexibility. The RBI may focus on liquidity management and can deploy open market operations and variable rate repo auctions to ease periodic tightening in banking system liquidity and stabilize money market rates. This allows the central bank to support financial conditions without altering the policy rates.

Bond Strategy:

* Buy 6.48% GS 2035 around 7.15 to 7.14% with a target of 7.07% and a stop loss of 7.22%.

* Buy 6.68% GS 2040 around 7.52 to 7.53% with a target of 7.45% and a stop loss of 7.58%.

SEBI Registration number is INH000000081.

Please refer disclaimer at https://geplcapital.com/term-disclaimer

Tag News

The Nifty has its crucial resistance 24500(Pivot Level) and 24600(Key Resistance) - GEPL Cap...