Debt and Forex Market Update 29th August 2025 by CareEdge Ratings

Contents

Key Global Developments

* US Short-Term Yield Falls; Fed Likely to Cut Policy Rate in September

* Global Trade Resilience Matrix: Assessing Vulnerabilities & Buffers to Global Trade Shocks

India Debt & FX Market Trends

* CPI Inflation Moderates Further in July

* Cumulative Rainfall 4% Above the LPA

* Liquidity Conditions are Comfortable

* Centre May Face Rs 700-800 Billion Annual Impact from GST Reforms

* 10Y GSec Yield Surges; Yield Curve Steepens

* Policy Rate Cut Transmission Accelerates

* CD Issuances Dip; CP Issuances Surge

* Corporate Bond Issuances at 6-Month Low in July

* Goods Trade Deficit at 8-Month High; Services Surplus Steady

* Net FDI Eases; FPI Outflows Continue for Third Straight Month

* Rupee Near Record Lows

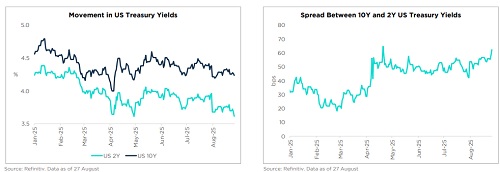

US Short-Term Yield Falls; Fed Likely to Cut Policy Rate in September

* US 2Y yield has declined by 31 bps over the past month, with Fed Chair Powell’s dovish tone at Jackson Hole adding to the move.

* The 10Y yield has eased by 15 bps but remains elevated amidst fiscal concerns and tariff-related inflation risks.

* The 10Y–2Y spread has widened to 62 bps from 46 bps a month ago.

* Markets are now pricing in two 25 bps Fed rate cuts in September and December 2025.

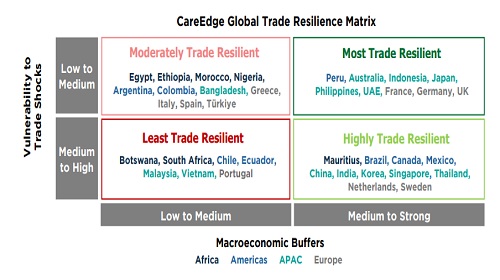

Global Trade Resilience Matrix: Assessing Vulnerabilities & Buffers to Global Trade Shocks

* CareEdge Global’s Trade Resilience Matrix evaluates 38 economies from our coverage universe on vulnerability to trade shocks and the strength of macroeconomic buffers. Countries are classified into four resilience profiles: Most Trade Resilient, Highly Trade Resilient, Moderately Trade Resilient and Least Trade Resilient.

* The US has imposed an additional 25% tariff on India, raising total tariffs to 50%. This could result in an annual drag on growth of around 0.8–1%. While India’s direct goods export exposure to the US is modest (~2% of GDP), elevated tariffs risk eroding competitiveness. Negotiations may take time, as India remains cautious on sensitive sectors like agriculture and dairy. There are also risks of sectoral tariffs on pharmaceuticals and select electronics, which are currently exempt. Nonetheless, we remain hopeful about a potential resolution in the coming months that could align India’s tariff more closely with peers, but the situation warrants close monitoring.

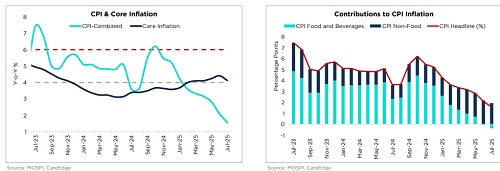

CPI Inflation Moderates Further in July

* The CPI inflation eased further to 1.6% in July, primarily driven by the deepening of deflation in the food category.

* The core inflation also eased to 4.1% down from 4.4% last month and remains at comfortable levels.

* We project average CPI inflation at 3.1% for FY26. However, we expect inflationary momentum to rise in H2 FY26 as the favourable base effect fades.

* Q4 FY26 inflation is projected to average well above 4%, and for FY27, we expect it to average above 4.5%. Accordingly, we do not anticipate further rate cuts unless economic growth weakens significantly

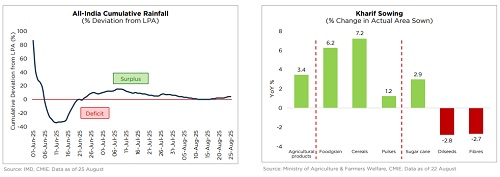

Cumulative Rainfall 4% Above the LPA

* The Southwest monsoon slowed in the first half of August but remained above the Long Period Average (LPA), standing at 4% above LPA as of 25 August 2025.

* Favourable prospects for agricultural output persist, with rainfall expected to pick up going forward.

* Total sown area recorded a 3.4% YoY increase as of 22 August 2025, despite subdued oilseeds and fibres sowing.

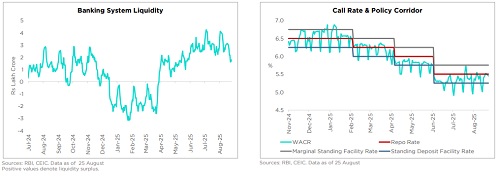

Liquidity Conditions Comfortable

* Banking system liquidity surplus averaged Rs 3 lakh crore in August (up to 25 August), though it narrowed recently due to GST outflows.

* On average, the WACR was 15 bps below the policy rate in August.

* The RBI has been conducting both VRRR and VRR auctions to manage liquidity conditions.

* Liquidity conditions are expected to stay comfortable, supported by month-end government spending, with the upcoming CRR cut in September providing further support.

Above views are of the author and not of the website kindly read disclaimer