Consumer Sector Update : Consumer price and commodity tracker By Motilal Oswal Financial Services Ltd

In our consumer price tracker, we cover over 100 SKUs across 15 consumer product sub-categories, ranging food, BPC, and home care. Food categories and the BPC segment were among the key beneficiaries of GST 2.0, witnessing doubledigit price cuts. With commodities like palm oil, maize, wheat, cocoa beans, and copra witnessing a deflationary trend in recent months, pricing strategies have become an important tracker. Some companies have highlighted the possibility of price increases in the coming quarters as well.

* Following the GST 2.0 announcement, there was a temporary blip (Sep’25 to Oct’25) due to trade-related disruptions. However, the issue normalized in the subsequent month. Under our coverage universe, staple companies were the biggest beneficiaries of GST 2.0. Within staples, the foods category saw minimal channel disruption and double-digit effective price cuts across biscuits and noodles. This was driven by a combination of MRP reductions and grammage increases (especially in LUPs), which supported volume traction. Beverage pricing has largely remained steady despite cooling tea and coffee costs. Edible oil prices have been range-bound, with companies taking calibrated ml-age reductions to preserve affordability amid sunflower inflation. With macro indicators turning supportive, expectations of a stronger summer season (after two weak years), and a stable RM environment, we see improving earnings visibility across staples and discretionary consumption.

* Similar to the food categories, GST 2.0 also benefited BPC categories such as soaps, oral care, and shampoos. In BPC, we observed that most companies opted for direct MRP cuts rather than grammage adjustments. In soaps, leading players implemented INR5–6 price cuts on key 100g SKUs (e.g., HUL’s Lifebuoy and Dove; GCPL’s Cinthol; Reckitt’s Dettol), translating into 5–13% portfoliolevel reductions. A similar trend was evident in toothpaste, with double-digit MRP cuts across key SKUs of Colgate, Dabur, and HUL. Shampoos also saw comparable MRP-led price cuts. Within pure coconut hair oil (no GST 2.0 impact), pricing divergence persists: MRCO’s Parachute remained stable, while Dabur’s Anmol Gold witnessed a ~16% price hike over the last six months.

* In home care, laundry saw some price hikes over the last three months, with no GST benefits applicable to the category. We observed that most players incl. P&G, HUL and Jyothy implemented price hikes over the last three to six months.

* As of mid-4QFY26, prices of non-agricultural commodities, such as crude oil, TiO2, soda ash, and palm oil, continued to decline YoY. Agricultural commodities, which had witnessed elevated pricing over the last couple of quarters, are now seeing moderation on a YoY basis. Commodities such as mentha, copra, and cashew remained inflationary YoY, while prices of wheat, maize, and cocoa have cooled. Overall, agri commodity prices are a mixed bag at this stage. Meanwhile, the rising crude oil prices remain a key monitorable

Food categories benefit the most from GST 2.0

Biscuits and noodles see double-digit price cuts following GST 2.0

* Since the GST rate revision announcement (Sept’25), we have highlighted that the packaged food industry would be the key beneficiary. In line with this view, our packaged food tracker indicates double-digit price cuts compared to preGST 2.0 prices.

* The price cuts have been passed on through a combination of MRP reductions and grammage increases across select SKUs (primarily LUPs). In select brands such as BRIT’s 50-50 and Jim Jam, we saw grammage increasing ~10% from 92gms to 100gms. Meanwhile, in Good Day Cashew (90gms pack), the MRP was reduced from INR25 to INR20 following GST 2.0. Larger bundle packs witnessed higher MRP cuts.

* Within the noodles portfolio, most SKUs have witnessed grammage increases rather than MRP cuts (even larger packs). NEST’s 280gms Maggi pack has been increased to 300gms, while ITC’s Yippee increased its 240gms pack to 270gms.

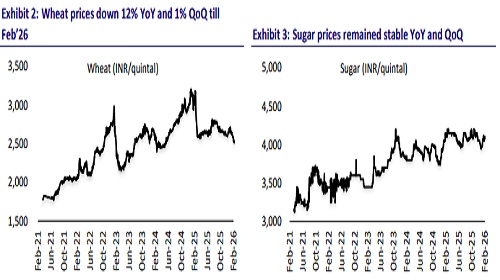

* On the RM front, wheat prices remained largely stable over the past few quarters (down 11% YoY). That said, with the wheat harvest season commencing in April, price trends thereafter will be a key monitorable. Sugar prices, on the other hand, have remained steady.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobile Sector Update : Timely revival in exports as domestic slows By Emkay Securities Ltd