Buy V-Guard Industries Ltd For Target Rs. 430 By Yes Securities Ltd

Inhouse manufacturing coupled with premiumization to drive margin expansion; Upgrade to BUY

Result Synopsis

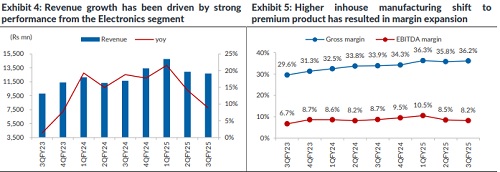

VGRD reported revenue growth of 9% marginally missing estimates. The growth was driven by strong performance of electronics segment (+27.9%) followed by Consumer durables (+8.1%). Electricals revenue grew 1.2%, lower growth in electricals was largely on account of channel destocking of wires. Sunflame has grown by 4% yoy. muted revenue growth was attributed to lower demand for kitchen appliances and significant decline in CSD orders. Gross margins for the quarter expanded by 228bps yoy on back of, benefit of pricing actions and increased inhouse manufacturing. Company believes large part of gross margin improvement on back of moving production inhouse is largely done with, further gross margins will expand when plant utilization sees improvement in couple of years. VGRD has started to make inroads in the nonsouth market resulting in non-south revenue growing faster than the South. On the Sunflame front restructuring is under way and company expects initiatives taken will take 3-4 quarters post which company will sunflame can see sustainable growth. We expect strong growth (ex of Sunflame) to continue in ensuing quarters as well, however margin is expected to remain in the similar range. Considering recent correction in the stock price we upgrade the stock to BUY with the revised PT of Rs430 valuing the stock at 42x FY27 EPS.

We believe VGRD’s brand strength, investments in own manufacturing and increased distribution in non-South markets are now paying rich dividends with non-south market with improved growth is also witnessing margin improvement. Moreover, material margins have been improving trend. We are factoring FY24-27E Revenue/EBITDA/PAT CAGR of 13%/17%/20% and our EPS for FY26 and FY27 gets trimmed largely considering higher employee expenses. We, however upgrade our rating to BUY given correction in the stock price and ex of sunflame business is on sound footing.

Result Highlights

* Quarter summary – V-guard has registered revenue growth 8.9% YoY driven by strong growth in Electronics, Electricals has seen muted growth of 1.2% on back of channel de-stocking of wires owing to volatility in copper prices. Consumer durables registered growth of 8%.

* Margin – Gross margin at 36.2% has seen expansion of 228bps, while EBITDA margin came in at 8.2% has contracted by 51bps. Higher employee expenses and increased A&P spends has resulted in EBITDA margin contraction.

* South vs Non-south – South markets witnessed a YoY growth of 3.7% whereas non-South markets grew by 15.8% in Q3FY25. Non-south market contribution stands at 48.4%.

* Debt – The company now has net cash of Rs 277.2mn vs net debt of Rs1451.2mn as on Q3FY24. The company has further repaid long term debt taken for sunflame acquisition and expect to repay entire debt by end of the fiscal.

Please refer disclaimer at https://yesinvest.in/privacy_policy_disclaimers

SEBI Registration number is INZ000185632