Buy TCS Ltd For Target Rs. 3,350 by Motilal Oswal Financial Services Ltd

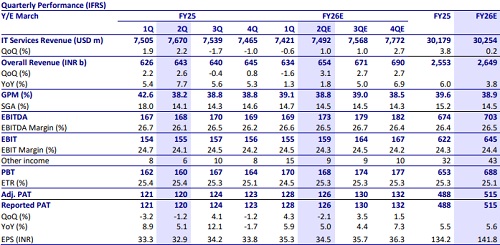

* TCS is expected to post revenue growth of 1.0% QoQ CC, with international business growing ~1% and India flat; we assume the BSNL ramp-up in 3Q.

* Outlook on near-term demand & tech budgets, BFSI vertical, and deal wins are key monitorables.

* We expect EBIT margin to decline ~20bp QoQ due to one-month impact of wage hikes, talent investments, lower utilization, and constrained leverage.

* We believe pyramid and productivity gains remain key levers, but pricing pressure, client behavior, and the GenAI transition signal a start of realignment as vendors adapt pricing and delivery models.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Buy Cholamandalam Inv. & Fin Ltd For Target Rs. 1,690 by Motilal Oswal Financial Services Ltd