Buy Sun Pharma Ltd for the Target Rs 2,120 by Motilal Oswal Financial Services Ltd

Opex drag dents margins; innovative medicines shine Specialty scale-up and branded generics leadership underpin growth

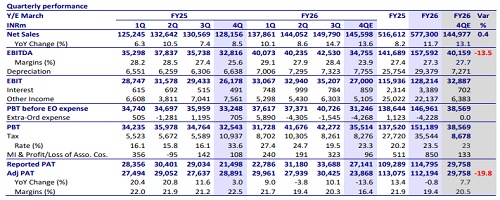

* Sun Pharma (SUNP) delivered in-line revenue in 4QFY26, whereas EBITDA/PAT came in lower than expected (14%/20% miss), dragged down by higher marketing spending and lower milestone income.

* SUNP has been beating industry growth in domestic formulation (DF) for two consecutive years, driven by product introductions and market share gains in existing products.

* Innovative medicines maintained robust growth momentum (20%/16.5% YoY in 4QFY26/FY26) and accounted for 22% of 4Q sales.

* US generics segment witnessed a decline in 4Q due to price erosion in the base portfolio. SUNP is working on greenfield manufacturing capacity to cater to various markets, including the US in the generics segment.

* We reduce our earnings estimates by 8%/10% for FY27/FY28, factoring in

a) increased opex for marketing/promotional spending on differentiated products

b) a gradual revival in US generics business. We value SUNP at 35x 12-month forward earnings to arrive at a TP of INR2,120.

* SUNP remains on track to expand its innovative medicines portfolio through

a) Product filing with USFDA,

b) Commercial partnerships

c) Increasing reach. Further, superior execution in branded generics positions SUNP well to outperform the industry. These benefits would be offset to some extent by ongoing price erosion in the US generics segment. Accordingly, we build in 12% earnings CAGR over FY26-28. Maintain BUY.

Segment mix benefit offset by higher opex YoY

* SUNP sales grew 13.6% YoY to INR145.6b (vs. our est. INR145b).

* Gross margin expanded 135bp YoY to 80.8% for the quarter.

* EBITDA margin contracted 175bp to 23.9% (vs our est. 27.7%).

* Accordingly, EBITDA grew 6% YoY to INR34.7b (vs our est. INR40.1).

* Adj. PAT was INR23.8b (our est. INR29.7b), down 13.6% YoY.

* For FY26, revenue/EBITDA grew 12%/11%, while PAT declined 1% YoY

Revenue growth driven by DF/ROW/EM segments offset by US sales

* DF sales grew 14.8% YoY to INR48.3b (33% of sales).

* ROW sales rose 16.1% YoY to INR20.1b (14% of sales).

* EM sales increased by 28.3% YoY to INR28b (19% of sales).

* US sales grew 4.5% YoY to INR42b (down 1.1% YoY to USD459m in cc terms; 29% of sales).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Buy Granules India Ltd for the Target 950 by Emkay Global Financial Services Ltd