Buy Sun Pharma Ltd for the Target Rs. 2,025 by Motilal Oswal Financial Services Ltd

Organon acquisition – Transformational fit, disciplined math

Portfolio expansion, 140+ country footprint and strong cash generation

* Sun Pharma’s (SUNP) proposed acquisition of New Jersey-based Organon will provide several advantages for SUNP in terms of portfolio expansion, healthcare professional (HCP) connect, and geographical reach.

* The USD12b all-cash acquisition will expand SUNP's innovative medicines portfolio by adding women healthcare segment, boost its biosimilar offerings, and significantly expand its commercial footprint across 140+ countries, including the US, EU, China, Canada, and Brazil.

* Notably, Organon’s stable EBITDA margins (30%+) and annual free cash flow of USD1b should boost SUNP's overall financials.

* Organon’s revenue has been stable over the past five years, which is adequately factored in its valuation of ~6.2x CY25 EV/EBITDA. Following SUNP’s acquisitions and subsequent scale-up track record, we believe there is a considerable scope to improve the company’s growth prospects going forward.

* Further, the combined EBITDA (~USD3.7b) would be more than sufficient to pay for the interest outgo related to Organon debt, as well as the debt taken by SUNP to fund the acquisition. The combined net debt-to-EBITDA ratio is comfortable at 2.3x. We will incorporate Organon’s financials after the deal closure (expected in 6-9 months).

* We value SUNP at 32x 12M forward earnings and arrive at a TP of INR2,025. Maintain BUY.

Transaction strengthens global positioning with attractive valuation and strategic fit

* SUNP has entered into a definitive agreement to acquire Organon in an allcash transaction at USD14/share, implying an enterprise value of ~USD11.75b.

* The transaction implies an equity value of ~USD4.0b and EV/EBITDA of ~6.2x (CY25 adj. EBITDA: USD1.9b), which appears reasonable given Organon’s stable cash flows and margin profile.

* SUNP will acquire 100% stake via a merger structure, funded through internal accruals and committed financing, with a pro forma net debt-toEBITDA ratio of ~2.3x after the deal completion.

Organon offers scaled global platform with strong cash flows and leadership in women’s health

* Organon is a global healthcare company with leadership in women’s health (ranked #2 in contraceptives and #3 in fertility), alongside a diversified portfolio of innovative medicines, established brands, and biosimilars.

* The company has a scaled and diversified portfolio of 70+ products, including 50+ established brands (with ~15 brands exceeding USD100m in sales), ~22 innovative/women’s health products (~33% revenue), and eight biosimilars (~11% revenue; ~USD700m sales; #7 globally).

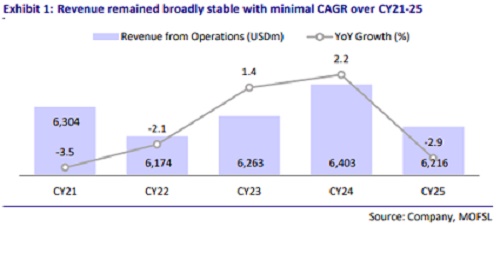

* Financially, Organon has delivered stable performance in CY25, with revenue of ~USD6.2b, EBITDA of ~USD1.9b (~30%+ margin), and annual free cash flow generation of >USD1b, supporting its leveraged balance sheet (USD8.6b debt, ~USD0.6b cash).

* The company has a strong global commercial footprint across 140+ countries and a diversified manufacturing base with six sites across developed and emerging markets, including capabilities in complex product manufacturing.

* Backed by ~100 years of legacy (via Merck & Co. spin-off), Organon benefits from strong brand equity, proven R&D capabilities (e.g., Nexplanon, NuvaRing), and a scalable global platform that complements SUNP’s portfolio and growth ambitions.

Highlights from the management commentary

* Organon has an established leading position in women’s health, with unmet needs across indications and scope for in-licensing to drive operating leverage.

* Synergies worth ~USD350m are expected over the next 3-4 years, primarily from cost efficiency in supply chain and workforce optimization.

* The combined entity will have commercial workforce of ~24k in 140+ countries, enabling a broader reach for its existing products and new launches.

* Organon adds scale in China (~USD800m in sales from eight key brands), providing a platform for product launches and access to the innovation landscape.

* Organon has ~10k employees, including ~4k field force. ? The company has capabilities in long-acting product development, which can be leveraged across multiple products.

* Organon has gross debt of USD8.5b and cash of USD0.9b, with the cost of debt at ~5.5%.

* It has maintained market share in core products with premium pricing in branded generics, with scope for line extensions.

* There is negligible overlap between SUNP and Organon portfolios; the acquisition is EPS accretive.

Valuation and view

* We expect SUNP to see a meaningful scale-up after the Organon acquisition, with pro forma revenue of ~USD12.4b and EBITDA of ~USD3.7b ((FY25 SUNP, CY25 Organon), supported by the addition of a stable, margin-resilient business with strong cash flow characteristics.

* The transaction enhances SUNP’s global positioning and portfolio diversification, with increased presence in women’s health, innovative medicines, and biosimilars. It strengthens SUNP’s scale across key international markets. We value SUNP at ~32x 12M forward earnings to arrive at a TP of INR2,025. Maintain BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041