Buy State Bank of India Ltd for the Target Rs.1,300 by Motilal Oswal Financial Services Ltd

A perfect blend of growth, profitability, and scale

To sustain market share gains and RoAs > ~1%

* State Bank of India (SBIN)’s FY26 annual report highlightsthat the bank has steadily strengthened its balance sheet and consistently delivered healthy RoE while maintaining its leadership position.

* SBIN’s loan book grew ~17% YoY, led by retail segment growth, with an uptick in corporate and Xpress credit books. SBIN has delivered an earnings CAGR of 26% over the past four years and crossed a milestone of INR800b of profits in FY26.

* Even as the deposit growth at ~11% YoY continued to lag credit growth, the bank remains comfortable with respect to its LCR and domestic C/D ratio at 124% and 73.1%, respectively, while maintaining stellar granularity in deposits.

* On the digital front, YONO continued to gain traction with ~100m registered users and 66% of savings accounts opened through YONO in FY25. The revamp of the YONO Business application in FY26 significantly strengthened the digital outreach of the bank, with the platform now supporting around 4.4m corporates with 5.9m users apart from retail customers. YONO continues to be a key enabler for sustained operating leverage for the bank.

* SBIN has maintained strong asset quality, with PCR at 74.4% (92.0% including TWO) in FY26. Controlled slippages(0.55%), a low SMA pool (7bp) with prudent underwriting, and continued recoveries shall keep credit costs under control. The top 20 NPA concentration hasreduced drastically to 11.8% as of Mar-26 from 29.1% on Mar-25,reflecting improved corporate health and granularity in underwriting.

* We estimate an 8% earnings CAGR over FY26-28, with an RoA/RoE of ~1.0%/15.5% in FY28. We reiterate SBIN as our top BUY idea among PSU banks with a TP of INR1,300 (premised on 1.4x FY28E ABV+ INR352 for subsidiaries).

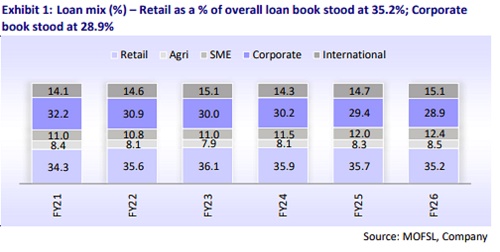

Building a granular asset book with a retail mix at ~35% of the loan book

SBIN delivered a 17% YoY loan growth in FY26, backed by prudent underwriting while focusing on the granular, high-quality portfolio. Retail loans grew steadily at 15.2% YoY, now making up 35.2% of the loan book, led by home loans and personal gold loans. Xpress credit growth is showing signs of recovery with the bank revamping the disbursement process. Corporate loan growth picked up significantly to ~15% YoY, driven by growth in renewables, data center capacities, metal, and infrastructure sectors. The SME segment posted robust growth of ~21% YoY alongside a notable reduction in GNPA from 9.2% in 1QFY22 to 3.0% in FY26. With a strong credit pipeline and a controlled domestic CD ratio of 73.1%, SBIN expects 13-15% credit growth in FY27. We estimate SBIN to report ~13.6% CAGR in its loan book over FY26-28.

Deposit market share at ~23%; C/D ratio remains comfortable

SBIN’s deposits grew 11% YoY in FY26, sustaining the 24% market share, with CASA deposits growing at 8.5% YoY (a challenge for the bank and the industry). With a favorable domestic CD ratio of 73.1%, well below that of peers, SBIN is wellpositioned for sustainable credit growth supported by robust underwriting and a potential corporate capex recovery. SBIN has a best-in-class granular deposit franchise with a higher proportion of retail deposits compared to its peers, also reflected in a low concentration of top 20 deposits at 4.5%. Costs of funds going forward are expected to only inch up marginally in the medium term, with sustained improvement in garnering the retail deposits. We, thus, build in ~11% CAGR in deposits over FY26-28 with a CASA CAGR of ~15%.

NIM to remain broadly stable; NII to clock a 15% CAGR over FY26-28

SBIN, in line with the industry, experienced pressure on NIMs in FY26 owing to the impact of the 125bp rate cut and the increasing proportion of EBLR mix. Consequently, NIMs contracted to 2.91% (3.03% in domestic business) in FY26 from 3.08% (3.21% in domestic business). The EBLR mix also increased from 42% in FY25 to 49% in FY26, increasing the pace of transmission. Going forward, expecting a relatively stable rate environment for FY26 and an uptick in Xpress credit book, we expect SBIN’s NIM to sustain at 2.8% over FY27. SBIN’s CD ratio remains under control, positioning the bank to deliver healthy loan growth, thus supporting NII. We estimate a ~15% CAGR in NII over FY26-28, after a muted NII growth of 4% in FY26.

Lower dependence on non-core income; PSLC costs moderate

* SBIN has historically had lower dependence on non-core other income items like treasury and recovery from technically written-off accounts. Recovery from TWOs contributes on average ~13bp to overall RoA and forms only 14% of the total other income, unlike its PSB peers, which have higher dependence on the same. Given the 10-year G-Sec has surged to 7.1% in the past few months, PSU banks are expected to report modest treasury performance, though, unlike other PSBs, SBIN has relatively lower dependence on treasury income.

* SBIN continues its trend of paying lower PSLC commission on a YoY basis, with the bank paying INR1,500b of PSLC commission in FY26 as against INR2,098b in FY25, hence lowering its opex intensity. Bancassurance income dipped 4% YoY in FY26, with bancassurance as a % of fees dropping to 12.2% in FY26 as against 14.7% in FY25, unlike trends for the previous few years, where bancassurance income mix witnessed a rising trend.

Building strong digital capability; YONO emerging as a key growth driver

SBIN has established leadership across debit card spends, POS terminals, ATMs, and mobile banking transactions (both in volume and value terms). YONO application continued to set new records, with ~100.2m registered users and 66% of savings accounts opened through YONO in FY26. The revamp of the YONO Business application in FY26 significantly strengthened the digital outreach of the bank. As of Mar-26, the platform had been supporting around 4.4m corporates with 5.9m users, apart from retail customers.

Digitalization to help contain costs and improve productivity levels

SBIN is focused on enhancing operating efficiency through digital innovation and cost management. We estimate the opex run rate to post an 11% CAGR over FY26- 28, growing in line with balance sheet growth, factoring in a moderate increase in branches and employees, and being partly offset by lower pension/gratuity provisions due to high interest rates. We estimate the C/I ratio to reduce from 51.1% in FY25 to around 49.8% by FY27, aided by increased digital adoption (notably via YONO) and productivity improvements.

Credit costs remain under control; NPA concentration reduced to ~12%

SBIN has maintained strong asset quality supported by robust underwriting and healthy recoveries from its TWO pool, with GNPA and NNPA ratios improving 33bp and 9p during FY26 to 1.49% and 0.39%, respectively. The bank maintains a healthy PCR of 74.4% (92.0% including TWO). SBIN reported benign slippages at INR238b (~0.5% of loans) in FY26, with continued traction in recoveries and upgrades. The top 20 NPA concentrations have reduced drastically to 11.8% as of Mar-26 from 29.1% as of Mar-25. With prudent underwriting and continued recoveries, we expect asset quality trends to remain stable, thus projecting the GNPA/NNPA ratio at 1.4%/0.4% by FY28, while credit costs remain in control at avg. 43bp over FY27-28E.

Valuation and view:

Reiterate BUY with a TP of INR1,300 SBIN has delivered a robust set of performances in recent years, propelled by steady business and revenue growth as well as controlled provisions. Even though NIMs have contracted in recent quarters owing to repo rate transmission, MCLR cuts, and migration of select corporate loans from MCLR-linked to T-bills, the bank has levers in place (CD ratio, MCLR repricing, asset mix improvement, etc.) to mitigate the impact arising from moderation in lending yields. SBIN’s asset quality remains healthy, with consistent improvements in headline asset quality ratios and a healthy recovery and upgrades run rate. We estimate credit costs to remain in check at 40- 45bp, enabling an 8% earnings CAGR over FY26-28. We, thus, estimate SBIN to deliver RoA/RoE of ~1.0%/15.5% in FY27-28. SBIN remains our preferred BUY in the sector with a TP of INR1,300 (based on 1.4x FY28E ABV + INR352 for subsidiaries).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412