Buy Star Health Ltd for the Target Rs. 640 by Motilal Oswal Financial Services Ltd

Underwriting performance strengthens

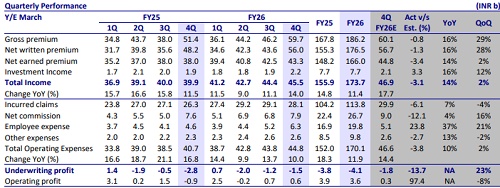

* Star Health (STARHEAL)’s net earned premium grew 14% YoY to INR43.3b (in line). For FY26, NEP grew 12% YoY to INR166b.

* The claims ratio at 64.8% (vs. our est. of 66.7%) improved 440bp YoY, the commission ratio at 14.2% (vs. our est. of 15.9%) declined 150bp YoY, and the expense ratio at 15.8% (vs. our est. of 13.6%) grew 160bp YoY. Robust underwriting performance led to a better-than-expected combined ratio of 94.8% (our estimate of 96.1%), which improved 440bp YoY.

* The underwriting loss of INR1.5b was lower than our estimate, while investment income was largely in line, leading to a 9% PAT beat at INR1.1b. For FY26, PAT declined 14% YoY to INR5.6b.

* The claims ratio is expected to maintain an improving trajectory, supported by price hikes and severity control through scaling up of prevention and wellness initiatives.

* We have largely maintained our IFRS estimates, considering a strong underwriting performance witnessed in 4QFY26. We expect IFRS PAT to post a 32% CAGR over FY26-28. We reiterate our BUY rating with a TP of INR640 (based on 24x FY28E IFRS PAT).

Fresh business growth supported by the new-to-insurance customers

* Gross written premium at INR59.7b grew 16% YoY, driven by a 19% YoY growth in retail health premium and offset by a 28% YoY decline in group health premium. For FY26, GWP grew 11% YoY to INR186.2b.

* The renewal premium ratio was 99% in FY26 (vs. 97% in FY25). Fresh business in the retail health segment grew 37% YoY to INR45.7b for FY26.

* The underwriting loss for 4QFY26 came in at INR1.5b (vs. our estimate of INR1.8b), compared to the underwriting loss of INR2.8b in 4QFY25. As per IFRS accounting, STARHEAL reported an underwriting profit of INR2.1b in FY26 compared to an underwriting loss of INR1.7b in FY25.

* The IFRS retail claims ratio improved to 64.8% in 4QFY26 (67.8% in 4QFY25), led by price hikes, fresh business growth, and reduced claim frequency. The group health claims ratio improved to 73.5% in 4QFY26 (from 87.3% in 4QFY25), driven by a calibrated approach in the segment towards profitable SME cohorts.

* The improvement in IFRS claims ratio from 68.2% in 4QFY25 to 64.6% in 4QFY26 was slightly offset by a rise in expense ratio from 30.1% in 4QFY25 to 31.1% in 4QFY26, resulting in a combined ratio of 95.7% in 4QFY26 (98.3% in 4QFY25). For FY26, the IFRS combined ratio improved to 98.4% (100.7% in FY25).

* The insurer experienced a loss of ~INR600m as per IFRS accounting in 4QFY26. For FY26, IFRS PAT was at INR9.1b (+16% YoY) with an RoE of 10%. Adjusting for a normalized yield of 8%, IFRS PAT would have grown 45% YoY to INR12.2b with an RoE of 13.1%.

* STARHEAL’s AUM grew to INR210b at the end of FY26 compared to INR183b at the end of FY25, with investment leverage at 2.1x. Investment yield declined to 5.8% (7.6% in FY25) due to negative equity market movements leading to MTM losses.

* The solvency ratio was largely stable at 2.1x.

* About 91% of the business came from proprietary channels, with STARHEAL having 830,000 agents and 924 branches. The target is to reach 1m+ agents in the next 2 years. Agency productivity grew 18% YoY to 410,000 in FY26, with 19% YoY growth in retail GWP and 8% YoY growth in fresh policies.

Key takeaways from the management commentary

* Due to higher contribution from long-term products and the 1/n accounting impact, NEP growth is expected to lag in the near term but should normalize in subsequent quarters.

* Investments in prevention and wellness initiatives (telemedicine, home healthcare, and condition management programs) have scaled significantly, with ~9x increase in usage in 4QFY26, supporting loss ratio improvement.

* Renewal book performance is improving, aided by pricing actions, with ~80% of the book expected to be repriced by 1QFY27.

Valuation and view

* Premium growth in 4QFY26 has been strong, especially in the retail health segment, backed by GST exemption. We remain optimistic about the overall prospects for Star Health, backed by 1) consistent growth in retail health, 2) improving agency and banca productivity, and 3) steady growth in specialized products and deepening presence. We believe that Star Health can deliver longterm growth with the investments made in profitable channels and products.

* The IFRS claims ratio is likely to improve and stabilize at ~68%, driven by the rising sum assured as well as price hikes. Continued operational efficiency will lead to an improved combined ratio in the long term.

* We broadly retain our IFRS estimates, considering a strong underwriting performance witnessed in 4QFY26. We expect IFRS PAT to post a 32% CAGR over FY26-28. We reiterate our BUY rating with a TP of INR640 (based on 24x FY28E IFRS PAT).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)