Buy SRF Ltd for the Target Rs.3,400 by Motilal Oswal Financial Services Ltd

Broad-based growth across all segments

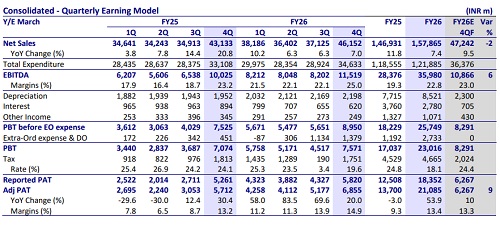

Operating performance beats our estimates

* SRF delivered a healthy performance in 4QFY26 as EBIT grew 14% YoY, led by a 5%/47%/63% YoY jump in the EBIT of Chemicals/Performance Films and Foil (PFF)/Technical Textiles Business (TTB). The company delivered a healthy performance despite a challenging global environment in the specialty chemicals segment, and successfully redirected its business away from the Middle East without any loss of volumes.

* Going forward, SRF’s overall business is expected to grow despite a volatile global environment, supported by diversification and a strong capex pipeline. Growth in FY27 is expected to be led by refrigerant gases, recovery in specialty chemicals, and improving fluoropolymer traction, while PFF and technical textiles show a gradual cyclical recovery.

* We broadly retain our FY27/FY28 EBITDA estimates. We reiterate our BUY rating with an SoTP-based TP of INR3,400.

Margin expansion across all the segments

* SRF reported overall revenue of INR46.2b (est. in line) in 4QFY26, up ~7% YoY. EBITDA margins expanded by 180bp YoY to 25% (est. of 23%). Gross margins stood at 50.5% in 4QFY26 vs. 48.2% in 4QFY25; employee costs

: 6.8% vs. 6.4%, power cost: 7.5% vs. 7.7%, and other expenses: 11.3% vs. 10.9%. EBITDA stood at INR11.5b (est. of INR10.9b), up 15% YoY. Adj. PAT grew 20% YoY to INR6.9b (est. of INR6.3b), adjusted for forex loss/labor code impact of INR1.3b/INR117m in 4QFY26.

* Chemical business revenue (53%/77% of total sales/EBIT in 4Q) grew 4% YoY to INR24.5b, EBIT grew 4.6% YoY to INR7.8b, and EBIT margin was 32.0% (vs. 31.8% in 4QFY25). The performance of the Fluorochemicals Business was robust due to higher domestic and export volumes, higher realizations in HFCs, and steady performance in Industrial Chemicals and Fluoropolymers. The Specialty Chemicals business improved QoQ despite pricing pressure and deferred orders, driven by cost efficiencies, new product launches, and progress in active ingredients development.

* PFF revenue (35%/15% of total sales/EBIT in 4QFY26) grew 13% YoY to INR16.0b, EBIT grew ~47% YoY to INR1.5b, and margin expanded 220bp YoY to 9.6%. The PFF Business delivered a healthy performance, driven by improved volumes and margins in BOPET and BOPP Films and a sustained focus on sustainable and value-added products

* Technical textiles revenue (10%/6% of total sales/EBIT in 4QFY26) was up 5% YoY at INR4.8b, EBIT grew 63% YoY to INR652m, and EBIT margin expanded 480p YoY to 13.5%. The TTB delivered an improved QoQ performance despite a challenging business environment.

* For FY26, Revenue/EBITDA/Adj. PAT grew 7%/27%/51% YoY to INR158b/INR36b/INR21b.

* Gross debt stood at INR50b vs INR46b as of Mar’25. CFO stood at INR2.6b vs INR2.5b as of Mar’25.

Highlights from the management commentary

* Guidance and outlook: The Chemical business is expected to deliver ~15-20% growth in FY27, led by refrigerant gas price and volumes and recovery in specialty chemicals. The company dos not expect the business to be impacted by the unavailability of raw materials. Further, the fluorochemical supply to the Middle Eastern market is expected to normalize.

* HFO project: SRF is setting up a project in Odisha, focusing on the fourthgeneration fluorochemicals comprising 20kMTPA of Hydrofluoroolefins (HFOs), 30kMTPA of Anhydrous Hydrogen Fluoride (AHF), and Value-added Hydrogen Fluoride (VHF). The project requires an estimated total capex of INR23b, financed through a mix of debt and internal accruals, with completion expected by Feb’28. The HFO product portfolio will comprise HFO1234yf, HFO1234z, and HFO1233zd.

* Capex: The BOD also approved a debottlenecking capex of INR880m, taking the HFC capacity to more than ~65kMTPA. SRF has deferred the proposed INR4.9b BOPP Film manufacturing facility at Indore and, instead, has planned to commission one new Polyamide line facility (India’s first of a kind) in Sep’27 (capex of INR1.8b). Further, management has guided for capex of INR25b for FY27.

Valuation and view

* We expect the chemicals business (fluorochemicals and specialty chemicals) to maintain the growth momentum going ahead, fueled by: 1) the ramp-up of recently commissioned plants, 2) the launch of new products, 3) a strong R&D and innovation pipeline, 4) stable demand for refrigerant gases in the international market and a recovery in the domestic market, and 5) expanding margins in PFF’s existing business, coupled with a ramp up in new capacities.

* We build in a CAGR of 15%/21%/24% of revenue/EBITDA/Adj. PAT over FY26- 28E. We reiterate our BUY rating and value the stock on an SoTP basis to arrive at our TP of INR3,400.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)