Buy Sansera Engineering Ltd For the Target Rs. 1,430 By the Axis Securites

Recommendation Rationale

Robust Order Book: Sansera has a strong order book, with annual peak revenues of Rs 2,201 Cr, 55% of which come from the Non-Auto, Auto Tech Agnostic, and EV segments. Its non-automotive business is experiencing strong growth, with a total order book of Rs 600 Cr spread across semiconductors, EMS, aerospace, and defence. The company expects to execute 50% of its non-automotive order book by FY26, driven by increased activity in semiconductor and defence projects.

Strong Financials to Support Growth: In Q3FY25, Sansera raised Rs 1,200 Cr through a QIP to support its strong order book and expansion plans. Of this, Rs 700 Cr was used to retire debt, reducing gross debt to Rs 350 Cr as of December 2024. The company allocated Rs 200 Cr for capex, Rs 100 Cr for land acquisition, and Rs 100 Cr for advanced manufacturing equipment. The remaining Rs 300 Cr includes Rs 25 Cr for QIP-related expenses and the allocation of Rs 275 Cr will be finalised in the coming weeks, focusing on growth capex and other developmental costs.

EBITDA Margins: We expect the company to deliver margins of 17-18% in FY25/26/27E, with projected EBITDA/PAT growth of approximately 15%/22% CAGR over FY24-27E. This growth is expected to be driven by a shift in the sales mix towards non-Auto ICE components, higher capacity utilisation, expansion in the export business, volume growth, and a recovery in Swedish operations.

Sector Outlook: Positive

Company Outlook & Guidance: The company is driving manufacturing growth and strengthening its position as a key exporter, creating more opportunities within the autocomponent sector. It has visible growth in xEV, Tech Agnostic, and Non-Auto products, supported by a strong order book and an increasing contribution to overall sales.

Current Valuation: 25x PE FY27EPS (unchanged).

Current TP: Rs 1,430/share (earlier Rs 1,780/share)

Recommendation: We maintain our BUY rating on the stock.

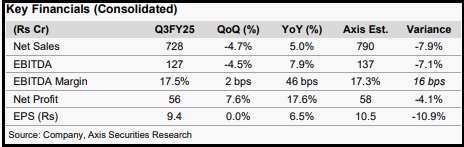

Financial Performance Sansera's Revenue/EBITDA/PAT missed both our and consensus estimates. Consolidated revenue (7.9% miss) grew 5% YoY. EBITDA (7.1% miss) up 7.9% YoY, primarily due to lower raw material and other expenses. EBITDA margin stood at 17.5%, up 50 bps YoY, largely in line with expectations. PAT (4.1% miss), grew 17.6% YoY, driven by higher other income and lower interest expenses.

Outlook Given factors such as a) a higher sales mix in Non-Auto ICE components, b) increased international business (exports), c) a focused approach on improving margin trends, d) the company’s strong ability to generate operating cash flows and e) capacity expansion plans, we expect Revenue, EBITDA, and PAT to grow at CAGRs of 13%, 15%, and 22%, respectively, over FY24-27E.

Valuation & Recommendation Due to a slower-than-expected recovery in the EU and North America; and a slowdown in the Auto segment, we have revised our earnings estimates downward. However, given Sansera’s 40 years of expertise, diversified business model, strong engineering capabilities, we maintain our BUY rating. We assign a 12-month forward PE multiple of 25x on FY27 EPS (unchanged) to arrive at a TP of Rs 1,430, implying an upside of 23% from the CMP.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633