Buy Sagility Ltd For Target Rs.54 by Elara Capital

Long runway for growth

Sagility (SAGILITY IN) is a pure-play healthcare focused technology provider that predominantly supports US payers (90% revenue mix). The company has 80+ clients in total, with an average tenure of 18 years for its top-five largest clients. SAGILITY is set to benefit from: i) sustained cost pressure for payers, thus creating further outsourcing opportunities, ii) end-to-end capabilities across payer value chain, and iii) further account mining scope in top-10 clients. Expect SAGILITY to post 13.9%/ 20.0% revenue /earnings CAGRs (INR-denominated) in FY26E-28E. We initiate with a BUY and a TP of INR 54, implying an upside of 26%, valuing SAGILITY at 19x FY28E EPS. Key risks are slower-than-expected outsourcing in US healthcare, muted growth in top accounts and lower-than-expected earnings.

Revenue from top-five accounts can potentially double from here: SAGILITY generated 60%/71%/85% of its revenue from top 3/5/10 clients, as on TTM Dec ’25. With a view to gauging the potential scale-up in these accounts in the long-term, per our analysis, revenue from top three accounts was USD 465mn as on TTM Dec ’25 with potential to be scaled up further by 40% (biggest opportunity for client 2/3). At the same time, revenue from top five accounts was USD 550mn as on TTM Dec ’25 and these five accounts can be scaled further by 80-90%, with maximum opportunities in client 3/4/5.

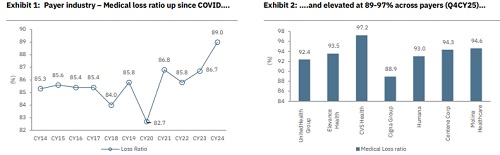

Higher MLR, rising administrative cost creating more outsourcing opportunities: Medical Loss ratio (claims paid/ premium earned) is rising across payers (e.g. United Healthcare, Humana, CVS Aetna, Elevance Health, Cigna HC, Centene Corp etc). At the same time, they have witnessed a continuous rise in admin cost, and costs have spiked at 2.5-18% CAGR in the past decade. We expect both these factors , creating further outsourcing opportunities. SAGILITY has guided 22.5% revenue growth in FY26, with guidance of low-to-mid teen medium term growth, which does not seem challenging, in our view.

Earnings growth to support multiple expansion: We build in 12.4%/13.9% USD/INR revenue CAGRs through FY26E-28E, majorly to be driven by FTE addition with minor improvement in revenue per employee. We do not see any major change in revenue mix in the medium term.Adjusted EBITDA margin may see some dip in FY26E due to integration of Broadpath business (low margin), but margin may settle at 25% by FY28E. Expect earnings to see jump in FY28E driven by absence of finance costs (planned full debt repayment in FY27E) . We are building in 20% earnings CAGR through FY26E-28E.

Initiate with Buy and a TP of INR 54: The stock is trading at 15.2x FY28E EPS, which is at a discount to some peers, possibly on account of client concentration risks and scalability of top accounts, which we believe is unwarranted. There is enough scope to scale up top accounts, which with new client additions and full debt repayment in FY27, may aid 20.0% earnings CAGR through FY26E-28E. We believe that with strong earnings growth, the stock should trade at a better multiple. We initiate with a BUY and a TP INR 54, based on 19x FY28E EPS. A downtrend in MLR (medical loss ratio) and administration costs for payer will likely reduce the need for outsourcing, which is a key risk, in our view.

Please refer disclaimer at Report

SEBI Registration number is INH000000933