Buy Radico Khaitan Ltd for the Target Rs. 4,000 by Motilal Oswal Financial Services Ltd

Growth excitement sustains; beat on margin

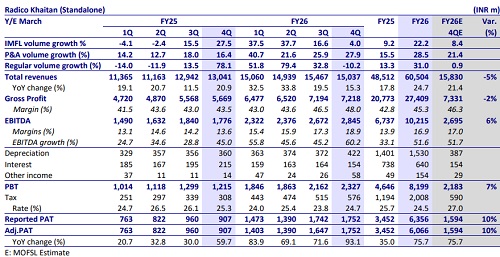

* Radico Khaitan (RDCK) continued to deliver robust P&A volume growth and strong operating performance in 4QFY26/FY26. Revenue growth was 15% YoY at INR15.0b, with P&A value growth at 29%. Meanwhile, regular portfolio declined 14%. P&A sustained industry-leading performance, and volumes jumped 28% YoY to 4.4m cases (est: 4.1m). On the other hand, regular portfolio volumes declined 10% YoY to ~5m cases due to a high base (AP route to market change in base) and impact of policy change in Karnataka and Maharashtra. Royalty cases declined 9% YoY to 0.4m cases. Non-IMFL revenue grew 21% on a low base.

* RDCK guided for 20% volume growth in P&A and 3–5% growth in the regular category for FY27. The company believes the proposed Karnataka excise policy will be favorable for the premium portfolio. In Maharashtra, the IMFL industry witnessed 20% volume decline. However, the premium and vodka segments have remained relatively resilient, thereby limiting the impact on the company portfolio. Further, the company is strengthening its presence in the MML segment through its JV, Radico NV Distilleries Maharashtra Limited (RNVDML), and is targeting 10–15% market share in the category over the medium term.

* Gross margin expanded by a sharp 450bp YoY to 48% (the highest in the last 20 quarters), backed by a benign raw material scenario (RM benefit +225bp YoY) and premiumization. EBITDA surged 60% YoY (est. 50%) and EBITDA margin expanded 530bp YoY to 18.9% (at an all-time high). Management maintained its EBITDA margin expansion guidance of 120–125bp for FY27 despite a 15% increase in glass cost over the last one month. Premiumization, operating efficiencies, and FTA will support margin. We model 17.6% and 18.5% EBITDA margins for FY27 and FY28.

* We continue to remain positive on RDCK, given its strong growth trajectory in the P&A segment and strategic expansion into premium and luxury portfolios. The luxury segment is seeing strong growth, generating INR4.7b revenue in FY26, and is expected to deliver 25% growth in FY27. With a continued focus on premiumization, operating leverage, and broad-based geographic expansion, RDCK has delivered industry-leading growth. We believe the rich valuations are well justified by its continued strong performance. We reiterate a BUY rating with a TP of INR4,000.

Beat on P&A volume; EBITDA up 60%

* Double-digit sales growth continues: Standalone net sales continued its robust growth momentum, up 15% YoY to INR15b (est. INR15.8b) in 4QFY26. P&A volume grew 28% YoY to 4.4m cases (est: 4.1m). Meanwhile, overall IMFL volumes grew 4% YoY (est. 8%). Regular portfolio volumes declined 10% YoY to ~5m cases, while Royalty cases dipped 9% YoY to 0.4m cases. Regular volume decline was due to a higher base of 4QFY25 after the change in the route-to-market in Andhra Pradesh, and the impact of the policy change in Maharashtra and Karnataka. Non-IMFL revenue grew 21% YoY on a lower base of bulk alcohol sales in 4QFY25.

* EBITDA up solid 60% YoY: Gross margin expanded 450bp YoY (+150bp QoQ) to 48% (highest in the last 20 quarters), backed by a relatively benign raw material scenario (RM benefit +225bps YoY), coupled with premiumization. Employee costs rose 15% and other expenses increased 13% YoY, while S&D rose 10%. Management alluded that in 4QFY26, A&SP was 6.7% of IMFL sales compared to 7.6% in 4QFY25. It expects to maintain A&SP spend at around 6% to 8% of IMFL revenues. EBITDA margin expanded 530bp YoY to 18.9% (highest ever), benefiting from robust GM expansion. EBITDA rose by robust 60% YoY (est: 50%).

* Strong growth in profitability: The interest cost declined by 28%. The net debt has reduced to INR2.4b (vs INR3.65b in 3QFY26), implying a reduction of INR3.3b since Mar’25. The company aspires to become net debt free by 1HFY27. PBT/APAT grew 92%/93% YoY in 4QFY26.

* In FY26, Revenue/EBITDA/APAT grew 25%/52%/76% YoY.

Highlights from the management commentary

* The company indicated that the gap between value growth and volume growth is expected to remain in the range of 300–400bp on an aggregate basis, supported by a favorable product mix and ongoing premiumization.

* Management highlighted that nearly 90% of power and fuel requirements across the Rampur and Sitapur facilities are met through biofuel-based systems, significantly reducing dependence on LPG. Both plants are largely self-sufficient in power generation through captive boilers and turbine infrastructure, thereby limiting operational risk from LPG disruptions.

* The company has reduced net debt by INR3.3b during FY26, driven by strong profitability and healthy cash flow generation, and is on track to become debtfree in FY27.

* The Board has made a formal dividend policy with a minimum payout ratio of 20% of PAT.

* FY27 capex guidance remains in the range of INR1.5–2.75b, largely focused on internal capacity optimization, operational efficiency improvement, and selective expansion initiatives.

Valuation and view

* We raise our EPS estimates by 3% for FY27 and FY28 on the back of continued strong volumes growth and beat on margins.

* Management remains committed to steadily reducing its debt, supported by healthy free cash flow generation. The company has reduced net debt by INR3.3b in FY26 and has net debt of INR2.4b as of Mar’26. It is on track to become debt free by FY27.

* RDCK remains focused on accelerating the premium and luxury growth, while driving greater efficiency across operations with disciplined capital allocation.

* Its P&A sales used to be ~15% of UNSP’s P&A sales in FY19; this share has now grown to ~30% (as of FY26), and we expect it to further improve going forward. The valuation gap with UNSP has narrowed significantly, reflecting market recognition of RDCK’s brand strength and execution.

* RDCK is currently trading at 58x/47x FY27E/FY28E P/E, with an RoE/RoIC of 20%/23% in FY27E. We believe a ~25% EPS CAGR over FY26-28E provides adequate support for sustaining rich valuations. We value the company at 55x P/E on Mar’28E EPS to derive a TP of INR4,000.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412