Buy Prestige Estates Projects Ltd for the Target Rs 1,680 by Motilal Oswal Financial Services Ltd

Scaling up well Strong pre-sales led by launches and diversification; healthy BD

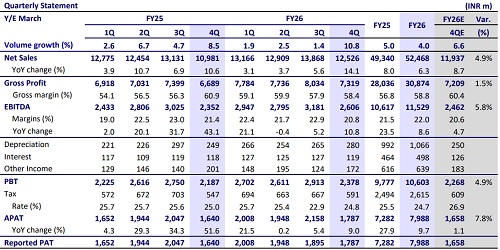

* Prestige Estates Projects’ (PEPL) 4QFY26 pre-sales rose 11% YoY to ~INR77b, driven by Bengaluru, which contributed 56% to pre-sales, followed by Mumbai (21%), NCR (14%), and other markets (9%). Evergreen @ Prestige Raintree Park (INR17b), Prestige Marigold P-2 (INR9b), and Prestige Nautilus (INR7b) were key performance drivers in 4Q.

* FY26 pre-sales grew by a robust 76% YoY to ~INR300b, with 63% contribution from newly launched projects (total ~INR274b GDV launched in FY26). Bengaluru led the performance with 34% contribution, followed by NCR (33%), Mumbai (20%), and other markets (13%). Key projects: TPC Indirapuram (INR96b pre-sales), Prestige Nautilus (INR30b), and Prestige Southern Star P-1 (INR21b).

* PEPL’s BD was strong with ~INR514b GDV added during FY26, providing healthy growth visibility. The company has guided for 15-20% pre-sales growth in FY27. It has a launch pipeline of INR578b, with additional projects expected to be added in the coming quarters. We expect a 14% CAGR in presales to ~INR388b over FY26-28.

Healthy collections limit debt increase despite aggressive BD

4QFY26 collections rose 66% YoY to ~INR52b, which led to FY26 collections growing strongly by 53% YoY to ~INR185b. OCF increased 56% YoY to ~INR70b, reflecting a healthy cash flow conversion. However, given the aggressive BD in FY26, net debt increased by ~INR21b QoQ to ~INR109b, while net debt-to-equity stood at 0.65x. On the back of healthy pre-sales growth and progress in execution, we expect ~16% CAGR in collections to ~INR251b over FY26-28, which would enable future expansions vis-à-vis keeping leverage under check.

Valuation and view

* PEPL has showcased strong scale-up in the residential segment on the back of regional diversification as well as continued launches. Recent business development deals have replenished the inventory pipeline, thus improving growth visibility over the medium term.

* Ramp-up in the annuity portfolio is progressing well, and upcoming assets are likely to significantly increase the annuity income over the medium term.

* We value the residential business at its NAV, while the land bank value is calculated on 1.7x FSI. Further, we value operational annuity assets at a 7.5% cap rate, and ongoing and upcoming assets at 8% cap rate.

* We have a BUY rating with a TP of INR1,680, indicating a 21% upside potential

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412