Buy Phoenix Mills Ltd For Target Rs.2,030 Motilal Oswal Financial services Ltd

Growth visibility remains strong Retail segment drives a strong 4Q performance

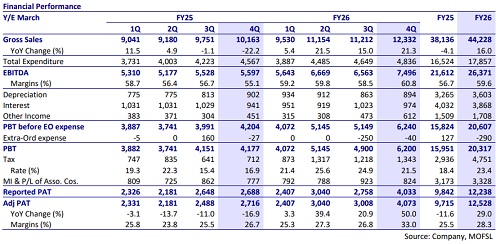

* In 4QFY26, Phoenix Mills (PHNX) reported 21% YoY growth in revenue to INR12.3b, while EBITDA grew 34% YoY to INR7.5b. Margin expanded +570bp/+230bp YoY/QoQ to 61%. Adj. PAT surged 50% YoY to INR4.1b, while the PAT margin stood at 33%.

* In FY26, revenue grew 16% YoY to INR44.2b. EBITDA grew 22% YoY to INR26.4b while margin expanded 295bp to 60%. Overall, Adj. PAT jumped 29% YoY to INR12.5b, with margins at 28%.

* Aided by improving occupancy at the retail and office portfolio, rental escalations, as well as better consumption growth, we expect a revenue CAGR of 14% to reach INR57.3b during FY26-28.

Improving occupancy and consumption growth drive the retail segment

* PHNX reported 14% YoY growth in retail rental income despite no new asset additions. This growth was mainly led by Mall of Asia/Citadel/Mall of Millennium/Palladium Mumbai, which reported 52%/27%/18%/15% YoY growth in 4QFY26. A mix of factors, like rental growth, strong consumption, and improving occupancy at these assets, contributed to its 4Q performance.

* In 4QFY26, consumption increased 31% YoY to INR43b, while in FY26 it grew 21% YoY to INR166b. In FY26, consumption growth was robust, led by the electronics segment, which grew 41% YoY. This was followed by the jewelry segment, showcasing 35% YoY consumption growth. Other segments like Entertainment and Fashion continued to perform well, growing at 22% and 16% YoY, respectively. The company plans to scale up the retail portfolio GLA to >18msf by FY30 (currently 11.5msf). We bake in a 10% CAGR in rental income to reach INR25.9b during FY26-28E.

Strong leasing in the office portfolio

* The company witnessed 13% YoY growth in income from commercial offices to INR580m during 4QFY26. EBITDA at INR380m grew 13% YoY while margins stood at 65%.

* The company completed gross leasing of ~2.2msf during FY26 for assets in Mumbai, Pune, Bengaluru, and Chennai. As of FY26, portfolio occupancy stood at 70%.

* Leased occupancy across new developments in Millennium Towers (Pune), Phoenix Asia Towers (Bengaluru), and One National Park (Chennai) stands at 78%, 33%, and 60%, respectively. The company targets scaling up the office portfolio GLA to 9msf by FY30 (currently 5msf). We expect income from the office segment to reach INR7.3b by FY28E.

Valuation and view

* In the retail portfolio, while new malls continue to ramp up well, PHNX is implementing measures to accelerate consumption at mature malls. These initiatives, along with a further increase in trading occupancy, will help PHNX sustain healthy traction in consumption. New asset additions in the coming years would further lead to better growth in rental income over the medium term.

* Further, the office portfolio has ramped up well, whereas the Hospitality segment continues to remain resilient.

* We have a BUY rating on the stock with a TP of INR2,030, valued on an SoTP basis.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041