Buy Persistent Systems Ltd for the Target Rs. 6,200 by Motilal Oswal Financial Services Ltd

Soft exit on core growth

USD2b revenue target intact; margins steady with reinvestment bias

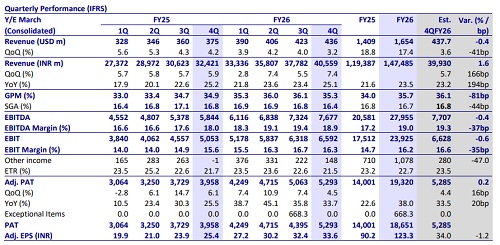

* Persistent Systems (PSYS) reported 4QFY26 revenue of USD436m (vs. est. USD438m), up 3.2% QoQ in USD terms and 3.4% in CC (est. +3.5%). Adj. EBIT margin stood at 16.3% (est. 16.6%).

* Adj. EBIT grew 16.3% QoQ/16.2% YoY to INR6.6b. Adj. PAT came in at INR5.3b (est. INR5.3b), up 4.5% QoQ/33.7% YoY.

* For FY26, revenue/adj. EBIT/adj. PAT grew 23.5%/36.6%/3.79% YoY in INR terms. We expect revenue/adj. EBIT/adj. PAT to grow 26.9%/38.9%/34.8% YoY in 1QFY27. Free cash flow stood at 94.7% of net profit for FY26. FY26 RoE came in at 27.3% (vs. 24.8%/25.6%/25.9% in FY25/FY24/FY23). TTM TCV was USD601m, down 10.8% QoQ and up 16.1% YoY (1.4x book-to-bill). We value PSYS at 34x FY28E EPS. Reiterate BUY with a TP of INR6,200.

Our view: Reinvestment to cap near-term margin upside

* Fifth straight quarter of deceleration in revenue growth excl. software licenses: 4Q revenue grew 3.4% QoQ in CC terms, a slight miss on consensus numbers. Revenue growth (excl. software licenses) continues to soften, with ~15% YoY growth in 4Q. While PSYS remains one of the fastestgrowing IT services companies in our coverage, this marks the fifth straight quarter of YoY deceleration in revenue growth excl. software licenses (Exhibit 2).

* The ask rate for next four-quarter CQGR for guided USD2b revenue is ~3.5% QoQ CC. This would imply ~15% YoY growth for PSYS in FY27, again better than the industry but lower than our earlier expectation of ~18%.

* Top 5 clients’ revenue declined ~1.2% QoQ, with YoY growth moderating to ~12% (vs. ~25% earlier). This moderation is largely driven by offshoring shifts and execution-related changes rather than demand weakness. Management indicated no structural issue in large accounts, with wallet share remaining intact.

* Margin recovery with reinvestment bias: 4Q EBIT margin at 16.3% (down 40bp QoQ) was supported by absence of 3Q one-offs (+220bp), operational efficiencies (+40bp), and favorable currency (+60bp), partly offset by higher consulting/advisory (-60bp) and software/travel costs (-70bp).

* However, management reiterated that growth reinvestment, particularly in AI platforms, consulting, and capability buildout, remains the priority. While the 16-17% margin band is achievable, near-term expansion could be capped by continued investments. We estimate EBIT margin of 16.7%/16.8% for FY27/FY28.

Valuation and revisions to our estimates

* We now build in ~16% USD revenue CAGR over FY26-28E for PSYS, reflecting moderation in core growth. Along with gradual margin expansion, this translates into ~20-22% EPS CAGR, still among the stronger growth profiles in mid-tier IT, though lower than earlier expectations.

* We cut our estimates by ~4-5%, factoring in a soft 4Q exit and continued reinvestments in AI platforms and consulting capabilities. We now build in a more gradual margin expansion to ~16.7-16.8% over FY27-28E. We value PSYS at 34x FY28E EPS and maintain BUY with a revised TP of INR6,200.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412