Buy Mrs. Bector’s Food Specialities Ltd for the Target Rs.252 by Geojit Investments Ltd

A Branded Play at the Cusp of Earnings Recovery

Mrs. Bector's Food Specialities Ltd (MBFSL) is one of India’s leading manufacturers of biscuits and bakery products, established in 1978. The company operates through its two flagship brands—Cremica, which includes biscuits, cookies, crackers, cream biscuits, and digestives, and English Oven, which offers breads, buns, pizza bases, and cakes.

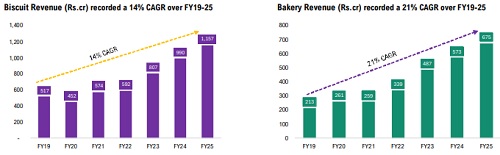

* MBFSL is projected to deliver a 13% revenue CAGR over FY26–28E, with revenue from operations expected to reach Rs.26bn, supported by scale-up in the bakery business (QSR and modern trade), rising export momentum, and gradual premiumization in the biscuits portfolio.

* EBITDA is expected to rise from Rs.251cr (13.4% margin) in FY25 to Rs.365cr (13.9% margin) in FY28E, supported by favourable input costs, though margin expansion is likely to remain gradual amid intense competition in biscuits. • PAT is projected to increase from Rs.143cr in FY25 to Rs.228cr in FY28E (a ~17% CAGR), supported by EBITDA expansion, moderate depreciation, and a strong balance sheet with negligible net debt, resulting in an FY28E EPS of Rs.7.4 (Rs.4.7 in FY25).

* Return ratios are expected to remain moderate in the near term as capex-led capacity additions expand the capital base. ROE is likely to decline from 15.7% in FY25 to 12.5% in FY26E, before improving to 14.5% by FY28E, while ROCE is expected to move from 14.1% to 11.7% and recover to 14.3% over the same period. The near-term dilution is structural, reflecting the ramp-up of newly added capacity.

Investment Rationale

* Dual-Brand Moat: Cremica + English Oven Covering the Full Value Chain

* India's fast-growing biscuit exporter to 70+ countries, expecting mid-to-high teen CAGR from FY26E.

* Preferred supplier for McDonald's, Domino's, KFC & Subway; institutional bakery revenue is growing at ~18% CAGR, with QSR chain expansion expected at ~19% CAGR through FY29.

* MBFSL is in the midst of its most aggressive expansion phase. This expansion facilitates the company's reach into South India and West India—markets where Cremica and English Oven have historically had limited presence. Distribution has been extended to 75,000+ retail outlets for English Oven (up from 55,000 in FY23).

• Strengthened Balance Sheet and Project Impact 1.0 Set the Stage for Margin ReRating.

Outlook & Valuations

At the current valuation levels, the near-term business risks, including raw material volatility and capex-led near-term profitability drag, appear largely factored in. However, with the topline expected to grow at a 13% CAGR in FY26E28E and EPS to grow at a 22% CAGR in the same period, we value the stock at 34X (5yr avg=40) and assign a target of Rs.252 on FY28E EPS.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034