Buy Minda Corporation Ltd for Target Rs. 650 by Choice Institutional Equities

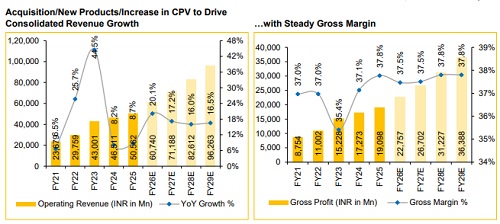

Rising Content Per Vehicle (CPV) Powers Transition to a System Supplier: Over FY21–FY25, MDA significantly expanded its CPV through strategic acquisitions and deeper product penetration. The shift, from conventional mechanical locksets (INR 400–1,000/unit) to smart keys and keyless entry systems (INR 1,500–4,000/unit), delivers a 2.5x–4.0x CPV uplift. Analogue-to-TFT cluster upgrades add a further 2.5x–5x value uplift, while EV wiring harnesses carry nearly 3.0x the content value of conventional ICE harnesses. Together, these initiatives have transformed MDA from a 2W-focussed component supplier into a diversified system solutions provider.

Profitable Growth Led by Acquisitions and Mix Gains: The strong financial outperformance in 9MFY26 has been driven by strategic acquisitions and favourable product-mix shifts. The acquisition of Flash Electronics (49% stake, at INR 13,720 Mn in January 2025), with Flash delivering INR 15,370 Mn revenue at 14.5% EBITDA margin in FY25 and a breakout 18.4% EBITDA margin in Q3FY26, materially enhances MDA’s EV powertrain credentials. Consolidated EBITDA margin improved ~220 bps over FY21–FY25 and we expect a further ~54 bps expansion over FY25– FY29E to ~12.0%, driven by operating leverage, premium product scaling, and rising JV contribution. Key subsidiaries and associates now operate at 14–20% margin, as compared with the group's ~11% historical margin, reflecting a structurally improving profitability mix.

Vision 2030–Capex-Funded Growth with Balance Sheet Discipline: MDA targets ~3.5x revenue growth to INR 175 Bn by FY30E from INR 50.6 Bn in FY25, alongside EBITDA margin expanding to >12.5% in FY30E, driven by premiumisation and JV-led scale-up. MDA has outlined a INR 20,000 Mn capex roadmap over the next 4–5 years, directed towards greenfield die-casting plants (Pune, Greater Noida), TFT instrument cluster facilities and JV ramp-ups (HCMF sunroof SOP Q1FY27E, Toyodenso switches SOP H1FY28E). Despite near-term capex intensity, the D/E ratio is expected to decline, from 0.6x in FY25 to 0.3x by FY30E. Capex, as a percentage of revenue, has moderated, from 6.9% in FY25 to ~4.5% by FY28E as new facilities are operationalised.

Valuation and View: MDA posted a consolidated revenue/EBITDA/PAT CAGR of ~21%/~28%/~48% over FY21–FY25, driven by premiumisation-led content upgrades and the Flash Electronics acquisition boosting content per vehicle (CPV) and EBITDA margin from 9.2% in FY21 to 11.4% in FY25.

We initiate a BUY rating with a DCF-based 12-month target price of INR 650 per share (implied P/E of 29x on FY28E EPS) and currently trades at a PEG ratio of 1.5x. We forecast a ~17%/~18%/~29% revenue/EBITDA/PAT CAGR over FY26– FY29E, driven by CPV gains across three structural levers: Premiumisation (smart keys, TFT clusters, EV harnesses), new product verticals (sunroof, switches, EV products) and export scale-up (7–8% → 10–15% of revenue).

Optionality: Upside from EV adoption, incremental recent JV wins (Turntide, Toyodenso and Flash), export scale-up, and future acquisitions could accelerate CPV expansion, margin improvement and earnings accretion

Risks: Key risks to our estimates include moderation in vehicle demand, volatility in raw material prices, and intensifying competition, which could impact growth and margins. However, limited exposure to the Middle East mitigates risks to export growth

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131