Buy Max Healthcare Ltd for the Target Rs 1,200 by Motilal Oswal Financial Services Ltd

Margin resilience offsets revenue shortfall Brownfield ramp-up at Smart/Nanavati/Mohali and Gurgaon greenfield to drive FY27-28 recovery

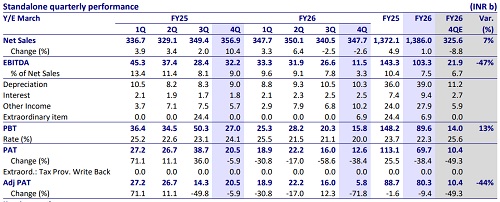

* Max Healthcare (MAXH) delivered lower-than-expected revenue (10% miss) in 4QFY26 due to a higher tax rate. However, EBITDA came in line with our estimate, implying improved profitability.

* The stoppage of sale of certain chemotherapy drugs impacted the overall performance of the company in 4Q, the second consecutive quarter of subdued YoY revenue growth.

* In-patient volume growth YoY was soft at 3.9%. ARPOB was stable YoY.

* Having said this, occupancy was strong at 75% and EBITDA per bed was robust at INR7.3m, stable YoY/QoQ.

* MAXH is working on improving occupancy of recent bed additions (20% being rolled out over past six months in brownfield capacity).

* We lower our earnings estimates by 3% each for FY27/FY28, factoring in a delay in operationalizing the Gurgaon project and b) the impact of discontinuation of chemotherapy drugs.

* We value MAXH on an SoTP basis (premised on 33x 12-month forward EV/EBITDA for the hospital business, 30x 12-month forward EV/EBITDA for Max@lab, and 11x EV/sales for Max@home) to arrive at a TP of INR1,200.

* Compared to robust earnings growth YoY over FY22-24, MAXH reported lower earnings growth YoY in FY25/FY26. Having said this, brownfield bed additions at Max Smart, Nanavati and Mohali would drive up earnings growth in the near term. Its greenfield project in Gurgaon would drive growth from FY28 onward. Further, it remains well-placed for bed capacity expansion in its focus markets. Maintain BUY.

Revenue growth drives operating leverage; high tax drags down earnings

* In 4QFY26, Max network revenue (including the trust business) grew 10.2% YoY to INR25.4b (our est. INR26.6b).

* EBITDA margin expanded 30bp YoY to 26.7% (our est. 25.2%).

* EBITDA grew 12% YoY to INR6.8b (our est. INR 6.7b).

* Adj. PAT declined 3.8% YoY INR3.8b (our est: INR4.2b), due to higher interest, depreciation and tax outgo on YoY basis.

* EBITDA per bed (annualized) stood at INR7.3m for the quarter.

* FY26 revenue/EBITDA/PAT grew 16%/14%/7% YoY to INR100b/INR26b/ INR16b.

Other conference call highlights

* In Mohali (426), structural work is ongoing; to start in FY28.

* Dwarka hospital would take 24 months to complete.

* Patparganj hospital to be commissioned by FY29.

* Awaiting plan approval for hospital project at Vaishali.

* MAXH would also be scaling up the capacity in Lucknow.

* Net debt was INR19b (vs. INR22b QoQ) at the end of 4QFY26.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412