Buy Mankind Pharma Ltd for the Target Rs. 2,640 by Motilal Oswal Financial Services Ltd

Domestic formulation on revival mode; BSV scaling up

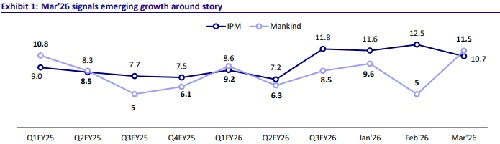

* Mankind’s domestic formulation (DF) business is witnessing a healthy revival, with Mar’26 growth at 11.5% YoY vs. IPM growth at 10.6% (1.1pp outperformance). The broad-based recovery in DF is driven by chronic therapies (cardiac up ~20%/anti-diabetic up ~12.6% YoY), indicating improving execution and field force stability after restructuring.

* Growth drivers are strengthening structurally, with the performance of new Rx launches surging 4.8x over the past three years (to INR5.2b in MAT Mar’26) and a concentrated contribution from top brands (~65%). Moreover, a rapidly scaling up in-licensed/partnered portfolio (~3x growth, led by respiratory) is building a dual-engine growth model for Mankind.

* BSV has moved past the integration phase, with a strong pickup in growth in 3QFY26 (20%+ YoY), driven by normalization in operations and improved execution. With cost synergies having largely been realized, the next phase will be led by revenue synergies, cross-selling opportunities and operating leverage.

* On overall basis, we expect a CAGR of 13%/11% in DF/export revenue over FY26-28, led by restructuring-led revival and strengthening revenue synergy in acquired products. Accordingly, we expect 16% EBITDA CAGR over FY26-28. This would be further supported by a declining interest outgo, driving 27% earnings CAGR over FY26-28. We value Mankind at 35x 12M forward earnings to arrive at a TP of INR2,640. Reiterate BUY.

DF: Broad-based recovery with chronic strength and pipeline-driven growth acceleration

* Mankind’s Mar’26 performance (~11.5% YoY vs. IPM’s ~10.6%) marks a clear revival, indicating ~1.1pp outperformance and signaling a strong exit momentum after a prolonged phase of underperformance, driven by restructuring and operational disruptions over the past 12-15 months.

* The recovery is broad-based but quality-led, anchored by chronic therapies cardiac/anti-diabetic (up ~20%/12.6% YoY) and supported by selective acute traction, while anti-infectives remain a key laggard (-0.4%).

* The rebound in Mar’26 is driven by core brands, with Glizid-M (+25% YoY), Telmikind (+21% YoY), and Dydroboon (+20% YoY) anchoring growth. Meanwhile, Cefakind/Gudcef continue to lag.

* In the past three years, the performance of new launches surged ~4.8x to INR5.2b, with top 20% brands contributing ~65%. Growth is non-linear/ therapy-driven – Gastro leads with ~8x; anti-diabetic compounds steadily by 3-4x; and AI/Pain therapies show strong ramp-up from a lower base.

BSV: Integration behind, growth acceleration driven by execution and synergies

* BSV’s performance in 1HFY26 was impacted by integration-related disruptions, with sequential improvement through the period indicating steady normalization in operations.

* Growth accelerated meaningfully from 3QFY26 (20%+ YoY), led by both domestic specialty and export segments, reflecting a recovery in execution.

* The prescription business has already surpassed full-year FY25 sales within 9MFY26, underscoring the strength of the rebound.

* Cost synergies and operational efficiencies are largely in place, supporting improved productivity and margin expansion.

* With integration largely behind and revenue synergies gaining traction, BSV is well positioned to deliver sustainable double-digit growth.

Valuation and view

* We expect Mankind to deliver ~13% revenue CAGR over FY26-28, led by a recovery in DF, steady traction in chronic therapies, and strong growth from new product launches and brand extensions across key segments.

* Growth will be further supported by the integration of the BSV acquisition, with revenue synergies beginning to materialize through portfolio cross-leverage, expanded reach in women’s health and fertility segments, and improved fieldforce productivity.

* EBITDA/PAT are expected to clock ~16%/~27% CAGR over FY26-28, driven by steady gross margin expansion owing to premiumization and scale benefits from acquired businesses.

* We value the company at ~35x 12M forward earnings, reflecting improving growth visibility, strong domestic franchise execution, and synergy realization from acquisitions. Maintain BUY with a TP of INR2,640.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412