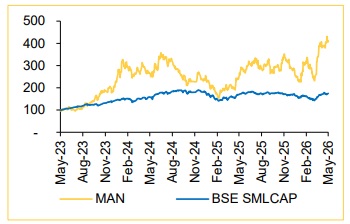

Buy Man Industries Ltd. for the Target Rs.690 by Choice Institutional Equities

Growth Catalysts will Lead to Profitability

FY26 was MAN’s most consequential year on record, delivering the highest-ever standalone EBITDA margin of 14% on revenues of INR 35,080 Mn whilst completing its landmark first international acquisition. The purchase of National Pipe Company in Saudi Arabia for INR 10 Bn at significantly cheaper valuation of 1.5x EV/EBITDA instantly transformed MAN’s scale, geography and addressable market. MAN has rapidly evolved from a domestic pipe manufacturer into a fully integrated, cross-border pipeline solutions platform. The management has guided FY27E consolidated revenues of INR 50–55 Bn, implying 40–50% growth, with sustained EBITDA margin of 13–15%.

Our positive stance is underpinned by the following key drivers:

1) Strong Earnings Trajectory: We build in Revenue/EBITDA/PAT CAGR of 31/41/66% over FY26–29E, supported by an order book of INR 30.0 Bn and a healthy bid pipeline of INR 160 Bn, providing multi-year visibility.

2) Balance Sheet Upside from Non-core Asset Monetisation: Monetisation of Navi Mumbai land parcel is likely to generate INR 8–9 Bn in cash inflow in the next 3–5 years, equivalent to ~20% of the current market cap, strengthening liquidity and funding growth capex.

3) Margin Expansion Catalysts: We forecast ~301 bps EBITDA margin improvement over FY26–29E, driven by a higher mix of value-added products, scale up benefits from increased capacity utilisation at existing and new plants and overall operating leverage gains.

Valuation: We reiterate our BUY rating on Man Industries Ltd. (MAN) with a revised target price of INR 690/share (INR 535/share earlier), driven by an improved business outlook, strong growth visibility, expected profitability expansion and capacity-led growth supported by a robust order book. We valued MAN using our EV/EBITDA multiple framework, assigning an EV/EBITDA multiple of 6x for FY28E. We consider these multiples conservative, given MAN’s strong ROCE trajectory, even under reasonable operating assumption.

Risks: Possible slowdown in conversion of bid pipeline into order book and probably slow ramp-up of upcoming capacities are risks to our BUY rating.

Q4FY26: Margin Expansion despite Soft Revenue Performance

* Consolidated Revenue for the quarter stood at INR 11,573 Mn down 5.0% YoY & up 39.4% QoQ (vs. CIE est of INR 14,000 Mn)

* Consolidated EBITDA grew by 4.5/8.0% YoY/QoQ to INR 1,397 Mn (vs. CIE est of INR 2,031 Mn), and margin improved by 110 bps YoY (down 351 bps QoQ) to 12.1%

* Consolidated RPAT down by 25.4/7.6% YoY/QoQ to INR 508 Mn (vs. CIE estimates of INR 1,106 Mn). RPAT margin stood at 4.4% down by 120/223 bps YoY/QoQ

* Order Book: Robust at INR 30.0 Bn (vs. ~40.0 Bn in Q3FY26)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131