Buy Lloyds Metals and Energy Ltd for Target Rs.1,730 by Choice Institutional Equities

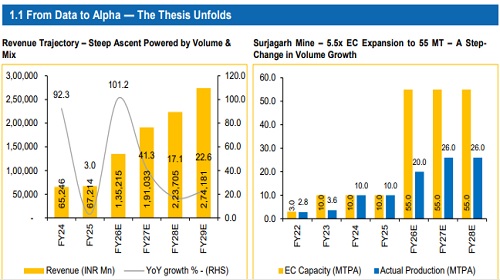

A Revenue Rocket Fuelled by Iron Ore Dominance and a Steel Value Chain in Full Build-out — From ~INR 67.2 Bn in FY25 to ~INR 223.7 Bn in FY28E: LLOYDSME is transitioning from a merchant miner to an integrated steel player, with revenue expected to grow from ~INR 67.2 Bn (FY25) to ~INR 223.7 Bn (FY28E) on a standalone basis driven by ramp-up in Surjagarh mining capacity to 55 MT and a 2.6x increase in production. At the same time, LLOYDSME is scaling up its value-added portfolio — pellet capacity expanding from 4 to 12 MT and a 1.2 MT wire rod plant coming online in FY27E. This integration across Iron Ore → Pellets → DRI → Wire Rod enables better margin capture and reduces dependence on raw material price cycles.

Margin on a Tear — Structural EBITDA Expansion to ~34.8% by FY28E: LLOYDSME is driving structural cost efficiency through integration (captive sourcing, logistics, captive power, value-addition), supported by a zeropremium ore base (MMDR 2015), slurry pipelines (85 km operational; 195 km by FY27E) and captive power (from 34 MW to 504 MW in phased manner). The mix shift the EBITDA (iron ore ~INR 2,000/t → pellets ~INR 4,000– 4,250/t → wire rods ~INR 11,000–13,500/t) delivers strong value uplift (2x/6x), expanding EBITDA margin (29.1% FY25 → ~34.8% FY28E).

Not a Cyclical Bet — Thriveni is LLOYDSME Annuity Engine: Thriveni adds a structural third lever to LLOYDSME’s margin framework, bringing asset-backed, contract-driven revenue visibility in a cyclical mining landscape. With an INR 100+ Bn asset base by FY28E (1,650+ equipment; >250 Mn BCM capacity; ~75 MT iron ore; ~1.7x volume ramp to 123.9 MT), the model is utilisation-led, where revenue scales with throughput, not commodity prices. As asset turns improve (~0.7x to ~1.0x), revenue productivity rises ~40– 45% without incremental capex, supporting ~INR 97.3 Bn revenue (FY26– 28E) with strong visibility via long-tenure MDO contracts. While labourintensive, costs are largely throughput-linked and partly pass-through, enabling stable-to-improving margins through operating leverage.

Copper Cathode JV — Hidden Optionality, Not in the Numbers: We assign no value to the Copper Cathode JV in our SOTP, given early-stage execution risks. However, with Congo-linked resource exposure and active promoter-led on-ground oversight, the project provides long-term optionality, with potential to be value-accretive upon successful commissioning and scale-up

Valuation: Our SOTP-based valuation assigns a 12x EV/EBITDA multiple to the core standalone business, reflecting peer-leading margin. We further value the Thriveni MDO subsidiary at 6x, recognising its distinct cash-flow profile and strategic optionality. We expect a steady improvement in earnings quality and cash-flow visibility. We initiate with a BUY rating and a 12-month target price of INR 1,730, offering a compelling 32.4% upside.

Key Risks: Possible Project Execution Delay, Probable Raw Material Volatility, Elevated Contingent Liability, Pledged Shares and Regulatory & Mining Risks.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131