Buy Laurus Labs Ltd for the Target Rs. 1370 by Motilal Oswal Financial Services Ltd

Sustained capacity investments drive earnings upgrades

* Laurus Lab delivered in-line revenue in 4QFY26. Improved operating leverage led to a 7% beat on EBITDA. A lower-than-expected tax rate led to 19% beat on PAT for the quarter.

* FY26 is the second consecutive year of strong YoY growth in CDMO revenue. (49%/38% in FY25/FY26). While Laurus continues to benefit from development project/commercialized molecules, it continues to invest in API and fermentation capacity to sustain the growth momentum.

* Affordable medicine business was stable YoY in 4Q but grew 18% YoY, led by strong off-take in Non-ARV FDF and higher traction in ARV segment.

* Higher revenue growth and better profitability led to ROE improvement to 18% from 7% YoY.

* We raise our earnings estimates by 8%/6% for FY27/FY28, factoring in a) higher traction in CDMO contracts, b) steady growth momentum in Non-ARV and ARV segments, and c) continued operating leverage. We value Laurus at 62x 12M forward earnings to arrive at a TP of INR1,370.

* We remain positive on Laurus on the back of a) continued investment across manufacturing capacities for CDMO as well as contracts in generics space; b) enhancing technology offerings to widen business prospects in CDMO segment; and c) controlled financial leverage. Reiterate BUY.

Segmental mix benefit partly offset by higher opex YoY

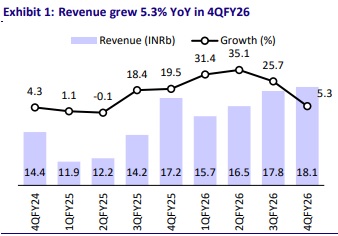

* 4Q revenue grew 5.3% YoY to INR18.1b (our est. INR18.3b), primarily driven by strong growth in generics (API business) and CDMO segments.

* Gross margin (GM) expanded 680bp YoY to 61% due to better divisional mix.

* EBITDA margin expanded by ~450bp YoY to 29% (our est: 26.8%), majorly driven by better gross margin, partially offset by higher employee expenses (up 200bp YoY).

* EBITDA grew 24.8% YoY to INR5.2b (our est. INR4.9b).

* Adj PAT grew 54% YoY to INR2.9b (our est: INR2.4b) for the quarter.

* FY26 revenue/EBITDA/PAT grew 23%/70%/188% YoY to INR68b/INR18b/ INR9b.

API/CDMO segments drive overall revenue growth

* CDMO business (29% of sales, small molecules) was up 14% YoY at INR5.2b.

* API sales (43% of sales) rose 12.5% YoY to INR7.7b.

* Bio division sales (4% of sales) grew 124% YoY to INR650m.

* FDF sales declined 17% YoY to INR4.5b (25% of sales).

Highlights from the management commentary

* Laurus guided for capex of ~INR30b over the next two years, with more than 90% allocated toward growth-oriented projects focused on expanding mid- and large-scale manufacturing capabilities.

* Key projects include greenfield Unit 7 facility with over 2,000 cubic meters of reactor capacity, expected to be ready for commercial validation by Mar’27, along with a second commercial-scale manufacturing block targeted for validation in 2QFY27.

* Additional investments include expansion of animal health capacity at Unit 10, greenfield fermentation facility expected to be operational by end-2026, formulation facility via JV with Phase 1 with completion targeted by mid-2027.

* Management remains confident of sustaining growth momentum of CDMO in FY27, supported by strong pipeline visibility and scaling of recently commissioned facilities. Laurus delivered three APIs in on-patent category. Given the long patent life, the sustainability of the business remains quite robust.

* Affordable medicine segment has a sufficient order book in place to have some growth in FY27 as well.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

Tag News

Buy Granules India Ltd for the Target 950 by Emkay Global Financial Services Ltd