Buy Larsen & Toubro Ltd for the Target Rs. 4,550 by Motilal Oswal Financial Services Ltd

Softer execution expected in 1HFY27

LT’s consolidated results for 4QFY26 and full-year FY26 were slightly weaker than our estimates on lower-than-expected execution in core EPC. Core EPC execution growth stood at 12% YoY during the year and was impacted by delays in domestic water projects as well as disruption due to the Middle East war. However, order inflows surprised positively at INR3.6t for FY26, up 25% YoY, indicating a healthy visibility for execution going forward. Margin performance was flat YoY, while NWC (at 4.1%) and RoE (at 16.6%) remained strong for FY26. Despite the disruption due to the West Asia crisis, prospect pipeline is strong at INR17.8t for FY27 vs. INR19t for FY26. LT has outlined investments across new-age areas in its strategic plan of Lakshya 2031 to be future ready, which we believe may be return dilutive in near term. We revise our estimates to factor in expected divestment of Hyderabad Metro and Nabha power by 1QFY27 and lower order inflows and execution for FY27, along with a stronger recovery in FY28 in the Middle East for reconstruction-led demand. With rolling forward to Jun’28, we arrive at a revised SoTP-based TP of INR4,550 (INR4,200 earlier), based on 25x two-year forward earnings for core business and a 25% holding company discount to subsidiaries.

Results hit by weak execution

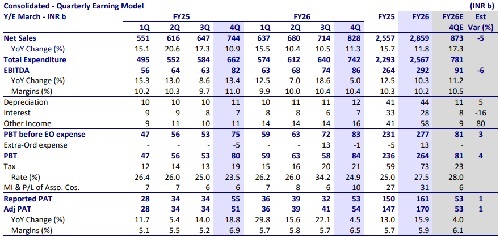

Consolidated revenue/EBITDA/PAT of INR828b/86b/54b grew 11%/5%/5% YoY in 4QFY26. While consolidated revenue/EBITDA missed our estimates by 5%/6%, EBITDA margin of 10.4% and PAT of INR54b were broadly in line with our estimates. For the core E&C business, order inflows came in 34% above our estimates at ~INR700b. While domestic order inflows increased 10% YoY, international ordering saw a 3% decline. This resulted in the core order book increasing 28% YoY to INR7.4t. Core E&C revenue came in at INR628b (up 11% YoY), 7% below our estimate mainly due to slightly weaker execution in water projects and revenue loss in Middle East projects in Mar’26. For FY26, consolidated revenue/EBITDA/PAT increased 12%/10%/16% YoY. OCF/FCF increased 83%/184% YoY. FY26 core E&C revenue/EBITDA rose 12%/12% YoY, while order inflow grew 25% YoY to INR3.6t.

Segmental margins impacted by cost overruns

For 4QFY26, core E&C EBITDA margin contracted 50bp YoY to 9.4% for the core business vs. our estimate of 9.6% mainly due to a change in revenue mix and higher logistics and insurance costs.

* Infrastructure segment margin improved 80bp YoY to 8.8%, mainly driven by execution cost savings.

* Energy segment margin stood at 6.6% vs. 8.1% last year. The margin variation is primarily attributed to cost inflation in few legacy jobs in the Hydrocarbon business.

* Hi-tech manufacturing margin stood at 17.9% vs. 19.5% in 4QFY25. The margin is reflective of the stage of execution and job mix in the portfolio.

* Others segment margin normalized after a sharp increase in the first nine months to 27.7% vs. 36.7% in the previous year.

Status of projects in Middle East

LT has indicated that the Middle East order book stands at around INR3t and currently work is progressing normally and payments are coming on time. The company has not seen cancellations of its projects, but deferment is seen in new project awards. Indirect impact of higher logistic and insurance costs is currently being felt on projects, and wherever possible, LT is in discussions with respective clients for a pass-through mechanism. The company lost nearly INR50b worth of revenue during the quarter due to the West Asia crisis and delays in water project completion on the domestic front.

Prospect pipeline remains strong

LT’s FY27 prospects pipeline stands at INR17.8t vs. INR19.0t last year (down 6% YoY). Of this, INR9.1t is from domestic and INR8.7t is from international markets. Under the new segment classification, infrastructure and utility prospects stand at INR9.4t (vs. INR8.1t last year), within which share of transportation is 23%, heavy-civil is 20%, power T&D is 18%, B&F is 17%, water is 16%, and metals and minerals is 6%. Prospect pipeline of Energy conventional is INR5.4t (vs. INR7.6t last year), which includes hydrocarbon prospects of INR4.7t (83% from domestic) and carbonlite solutions of INR0.7t (largely domestic). Further, the green energy segment’s prospect stands at INR2.5t (vs. INR3.0t last year), consisting of solar EPC prospect of INR1.8t (78% from international), and INR0.7t from offshore wind (completely international). The manufacturing and product pipeline is INR495b (vs. INR294b last year), including INR122b from heavy engineering and INR373b from PES systems. The previous year’s pipeline had gas-to-power prospects of INR0.6t, which is not being pursued in FY27.

Lakshya 2031 plan focuses on investments in new-age areas

LT has outlined plans for Lakshya 2026-31 with a capital allocation philosophy in 1) strengthening the core, which involves capability enhancement in manufacturing facilities and yards, process automation, project-led capex, and investments in commercial real estate; 2) building the future growth engines such as investments in data centers, green hydrogen & semiconductor design, and foray into electronic products manufacturing. The company targets a CAGR of 10-12% in order inflows and revenue growth of 12-15% over FY26-31 with RoE in the range of 16-17%.

Capex and investments across segments

The capital allocation plan for Lakshya 31 includes ~INR50b for industrial electronics, INR30b for semiconductors for acquisition of IP, creation of lab facilities, etc., INR150b for green hydrogen, and around INR100b for data centers across hyperscalers and non-hyper scalers. Around INR44b is allocated for the realty business, and around INR50b is planned for the upgrade of the existing hydrocarbon modular fabrication yard and shifting facility. Cumulatively, the company plans an investment of nearly INR430-450b over the next five years across these segments. For FY27 specifically, around INR25b will be for the core business, INR10b for electronics, and around INR20b for the data center.

Softer guidance for FY27 to bake in volatile environment

For FY27, LT has guided order inflow growth of 10-12%. Revenue growth would be in a similar range of 10-12%, with 1H to be softer due to the ongoing supply chain disruptions, and a pickup is expected in 2H as these constraints ease out. On the reclassification basis of the segments wherein realty business is excluded, core business margins for FY27 are expected to be in line with FY26 margins at 7.8%. NWC-to-sales is expected to normalize from current 4% levels to ~10% in FY27.

Financial outlook

We revise our estimates to factor in changes in subsidiary financials, expected divestment of Hyderabad Metro and Nabha power by 1QFY27, and lower execution in FY27. The company has highlighted that 1HFY27 will be softer in execution owing to the West Asia crisis and corresponding supply chain issues in the Middle East and India. We also bake in a subsequent faster recovery in FY28, led by reconstructionled demand in the Middle East region. We expect core E&C revenue/EBITDA/PAT to clock a CAGR of 19%/21%/26% over FY26-28.

Valuations and view

At the current price, for core E&C, LT is trading at 31x/23x P/E on FY27/28E earnings. Rolling forward to Jun’28, we arrive at a revised SoTP-based TP of INR4,550 (INR4,200 earlier), based on 25x two-year forward earnings for core business and a 25% holding company discount to subsidiaries.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412