Buy Larsen and Toubro Finance Ltd for the Target Rs. 350 by Motilal Oswal Financial Services Ltd

Healthy quarter fueled by strong growth and declining credit costs

ECL model refresh leads to lower PCR on S3; Lakshya 2031 targets announced

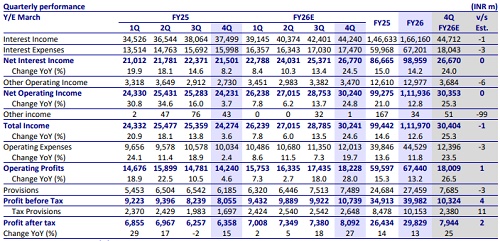

* L&T Finance (LTF)’s reported 4QFY26 PAT grew 27% YoY to INR8.1b (in line), and FY26 PAT grew 13% YoY to INR29.8b. NII in 4QFY26 grew ~25% YoY to INR26.8b (in line).

* Opex grew ~20% YoY to ~INR12b (in line). The cost-to-income ratio rose ~30bp QoQ to ~39.7% (PQ: ~39.4%). PPoP in 4QFY26 grew ~28% YoY to ~INR18.2b (in line), and FY26 PPOP grew 13% YoY to INR67.4b. Credit costs stood at INR7.5b (in line). Reported credit costs dipped to 2.64% (PQ: 2.83%), a reduction of ~20bp QoQ. Slippage continued to decline with slippages of INR4b in 4QFY26 (PQ: INR6b).

* In line with its annual ECL model refresh, LTF recalibrated PD and LGD assumptions and updated forward-looking risk parameters. This resulted in an ~INR3b release of provisions (INR2.9b from S3 and INR110m from S2), which was redeployed into Stage 1, enhancing coverage on S1 to ~80bp (PQ: ~60bp). The S3 PCR declined to 68% (PQ: 73%) but is adequate as per the company management and the ECL model. The overall adjustment was P&L neutral, and the balance sheet was further strengthened.

* Management expects FY27 to mark the start of consistent, high-quality growth, driven by strong demand across rural, urban, and gold loan segments, with a continued focus on quality-led expansion. Despite external shocks such as the West Asia crisis and potential El Niño impact, LTF remains confident of sustaining healthy, risk-calibrated growth and profitability.

* The company outlined its Lakshya 2031 goals, targeting 20%+ AUM growth, credit costs below 2%, RoA of 3.0-3.2%, and RoE of 16-18%, with a strong emphasis on tech-led execution, granular expansion, and strengthening both core and emerging businesses.

* We estimate a CAGR of ~21% in the loan book and ~28% in PAT over FY26- FY28E, with consolidated RoA/RoE of 2.6%/~15% in FY28E. We expect LTF to deliver a structural improvement in profitability and RoA from FY27 onward. Reiterate BUY with a TP of INR350 (based on 2.5x Mar’28E BVPS).

NIM improves ~20bp QoQ; CoB (reported) declines ~8bp QoQ

* Reported NIM improved ~20bp QoQ to 8.8%. However, NIM + fees rose ~6bp QoQ to ~10.5%. Spreads (calc.) declined ~10bp QoQ to ~8.4%. Yields (calc.) declined ~30bp QoQ to ~15%, while CoF (calc.) declined ~20bp QoQ to 6.6%. Reported CoB declined ~8bp QoQ to 7.17% in 4QFY26.

* Management shared that disbursement yields continue to remain higher than portfolio yields, primarily driven by a favorable product mix, and it expects NIM + fees income to remain stable in the ~10.0-10.5% range. We expect LTF to deliver a stable NIM (calc.) of ~9.4% each in FY27/FY28E.

Asset quality improves significantly; retail GS3 declines to ~2.5%

* Consol. GS3 declined ~30bp QoQ to ~2.9% while NS3 rose ~5bp QoQ to ~0.96%. PCR declined ~460bp QoQ to ~67.3%. Retail GS3 declined ~30bp QoQ to 2.53%.

* Management indicated that asset quality remains stable across segments, with no visible stress in rural, SME, or 2W portfolios, while maintaining a cautious stance in urban SME and personal loans amid ongoing West Asia uncertainties. We expect credit costs for LTF to decline gradually from ~2.6% in FY26 to ~2.3% in FY28E.

Retail loans grow 26% YoY; strong momentum across all product segments

* Disbursements grew 62% YoY to INR241b in 4QFY26. Growth in secured disbursements was led by 2W Finance, which stood at INR29.3b and grew 58% YoY. Gold Finance disbursements stood at INR27.8b in 4Q. Personal loan disbursements stood at INR37.9b with increased focus on big tech partnerships. Rural business finance disbursements rose 41% YoY and 7% QoQ to INR72.1b.

* The total loan book grew ~24.5% YoY and ~6% QoQ to ~INR1.22t. Wholesale loans declined to ~INR22b (PY: INR25.8b). Retail assets contributed ~98% to the loan mix. Retail loans grew ~26% YoY, led by healthy growth in MFI, 2W, SME, LAP, and personal loans. Personal loans exhibited robust growth of ~14% QoQ and 70% YoY. Rural Business Loans (MFI) grew ~6% QoQ, LAP grew ~9% QoQ, and SME grew at 7% QoQ.

MFI collection efficiency improves during the quarter

* MFI collection efficiency (0-90dpd) was ~99.2% in Mar’26 (98.7% in Dec’25).

* Only ~1.6% (PQ: ~2.4%) of LTF customers have loans from 4 or more lenders (including LTF). There were improvements across PAR1-30, PAR31-60, and PAR61-90 cohorts.

Highlights from management commentary

* Management shared that improvement in credit costs will be driven by sharper customer selection through the Cyclops underwriting engine, initially deployed in higher-risk segments such as 2W, tractors, and SME, with early trends encouraging and reflecting a strong shift toward prime customers alongside healthy origination growth.

* The company is undertaking aggressive distribution expansion, with plans to add 400-500 gold loan branches (including ~100 Sampoorna branches), along with 150-200 each of micro-loan and micro-LAP branches, significantly expanding its physical distribution footprint.

Valuation and view

* LTF’s 4QFY26 earnings were in line, with strong disbursement leading to healthy retail loan growth. Asset quality improved significantly during the quarter, resulting in sequentially lower credit costs. It also benefited from lower borrowing costs, aided by better treasury management and policy rate cuts, which contributed to a healthy expansion in NIM. The company also announced its Lakshya 2031 goals, which suggest potential for significant improvements in credit costs and return metrics over the coming years.

* LTF currently trades at 2.3x FY27E P/B. We estimate a CAGR of ~21% in the loan book and ~28% in PAT over FY26-28E, with consolidated RoA/RoE of 2.6%/15% in FY28E. We expect LTF to deliver a structural improvement in profitability and RoA from FY27 onward. Reiterate BUY with a TP of INR350 (based on 2.5x Mar’28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412