Buy Kotak Mahindra Bank Ltd for the Target Rs. 470 by Motilal Oswal Financial Services Ltd

Steady quarter; asset quality improves

RoA outlook remains healthy

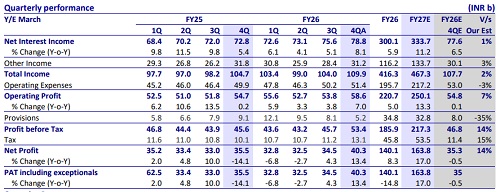

* Kotak Mahindra Bank (KMB) posted a healthy standalone 4QFY26 PAT of INR40.3b (14% beat; up 13.4% YoY/16.8% QoQ), aided by a notable decrease in provisions, NIM expansion and lower opex (reversal in retiral benefits). Consol PAT stood at INR54.2b (up 6% YoY/6% QoQ).

* NII grew 8.1% YoY/4.1% QoQ to INR78.8b (in line). NIMs improved sharply by 13bp QoQ to 4.67% (our est of 4.48%). Adjusted for day count impact, NIMs remained largely flat QoQ at 4.54%.

* Advances growth was steady at 16.2% YoY/3.2% QoQ to INR4.96t, aided by broad-based growth in HL, BB, SME and corporate advances. While credit card stood flat QoQ. Deposits grew by 14.7% YoY/5.5% QoQ, while CA book grew 18% QoQ. CASA ratio improved by 200bp QoQ to 43.3%.

* Slippages declined sharply to INR10.2b (down 32% YoY/37% QoQ). Credit cost fell to 0.39% (lower vs guidance). GNPA ratio declined by 10bp QoQ to 1.2%, while NNPA ratio declined by 6bp QoQ to 0.25%. The bank sees no inherent risk from the West Asia conflict.

* We marginally upgrade our earnings estimates by ~2% for FY27/28E and expect RoA/RoE of 1.96%/12.1% by FY27. Reiterate BUY with a TP of INR470 (2.1x Sep’27E ABV + SOTP of INR165).

NIMs improve 13bp QoQ (Adj NIMs flat QoQ)

* Standalone PAT stood at INR40.3b (up 13.4% YoY/16.8% QoQ), aided by a sharp decline in provisions, NIM expansion and lower opex (reversal in retiral benefit). Consol PAT stood at INR54.2b (up 10% YoY/10% QoQ).

* NII grew 8.1% YoY/4.1% QoQ to INR78.8b (in line). NIMs improved 13bp QoQ (adj NIMs stood flat QoQ at 4.54%), aided by lower day count in the quarter.

* Other income grew by 9.8% QoQ (down 2% YoY), led by healthy fee income and minimal treasury income. Opex rose 2.9% YoY/2.3% QoQ to INR51.4b (3% lower than estimate). PPoP rose 7% YoY/8.8% QoQ to INR58.6b (7% beat).

* Loan growth (already known) was steady at 16.2% YoY/3.2% QoQ to INR4.96t, aided by growth in HL (4.4% QoQ), SME (5.3% QoQ), MFI (8.4% QoQ), BB (5.5% QoQ), as well as PL, BL and consumer (3% QoQ).

* Deposits grew by 14.7% YoY/5.5% QoQ. CASA deposits grew 10.5% QoQ. As a result, CASA ratio improved to 43.3% (up 2% QoQ). TD witnessed slow growth at 14.1% YoY/2% QoQ.

* Fresh slippages declined to INR10.2b (down 32% YoY/37% QoQ) amid easing stress across segments. GNPA ratio fell 10bp QoQ to 1.2%, while NNPA ratio declined by 6bp QoQ to 0.25%. PCR improved to 79%. SMA-2 loans declined to INR1.9b/4bp of loans. CAR/CET-1 ratios stood at 22.4%/21.3%.

* Performance of subsidiaries: Kotak Prime’s net earnings fell 19% YoY/4% QoQ, while Kotak Life’s PAT declined 45% QoQ to INR0.9b. For Kotak Securities, reported PAT decreased 7% QoQ to INR4b. Kotak AMC’s PAT declined 42% QoQ to INR1.8b.

Highlights from the management commentary

* The secured portfolio continues to show negligible stress, with no reliance on large corporate recoveries.

* NIMs are expected to decline gradually over the next year, largely due to rising TD rates, especially toward 2H.

* For FY27E, the credit cost trajectory will depend on improving efficiency in retail, MFI, PL, and credit cards, with continued focus on collections. ECL transition impact is estimated to be less than 2% of net worth.

* The bank reduced reliance on high-cost deposits, including ~30% reduction in floating-rate SA balances, while focusing on stable granular funding.

Valuation and view: Reiterate BUY with a revised TP of INR470

KMB reported a strong quarter, marked by controlled slippages and credit costs, along with an uptick in NIMs. However, the bank guides for largely flat or slightly lower NIMs in FY27E vs. FY26, as it focuses on elongating deposit tenor (currently ~9-12 months), with higher peak rates offered on longer maturities. The unsecured portfolio is showing signs of stabilization, and the bank expects credit costs to remain well contained going ahead. While overall advances growth remained steady, corporate lending was relatively subdued as the bank chose not to roll over short-term wholesale exposures amid unattractive pricing. Encouragingly, disbursements in the unsecured segment have picked up, primarily led by existing customers. Management reiterated its guidance of delivering loan growth at ~1.5- 2.0x nominal GDP, supported by steady traction in retail and unsecured segments. On the regulatory front, the bank highlighted that the transition to ECL would have a limited impact of less than 2% on net worth, with no material effect expected on ongoing credit costs, reinforcing visibility on asset quality. We marginally upgrade our earnings estimates by ~2% for FY27/28E and expect RoA/RoE of 1.96%/12.1% by FY27. Reiterate BUY with a TP of INR470 (2.1x Sep’27E ABV + SOTP of INR165).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412