Buy JK Lakshmi Cement Ltd for the Target Rs 720 by Motilal Oswal Financial Services Ltd

Healthy volume growth; margin pressure in near term Cost headwinds and soft pricing keep near-term outlook cautious

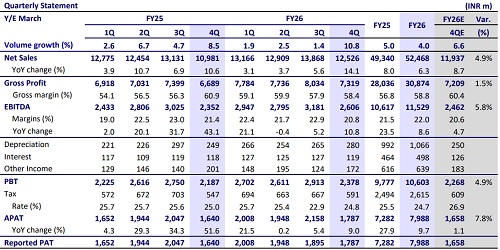

* JK Lakshmi Cement’s (JKLC) 4QFY26 EBITDA declined ~19% YoY to INR2.9b (+10% vs. estimates, led by lower-than-estimated opex/t). EBITDA/t fell 25% YoY to INR734 (est. INR683). OPM contracted 3.5pp YoY to ~15% (+1.4pp vs. estimates). Adj. PAT declined ~29% YoY to INR1.2b (+9% beat).

* Management highlighted that industry demand growth will be moderate at ~6% in FY27, impacted by macro headwinds. Margin pressure is intensifying due to sharp cost inflation, leading to a cost increase of ~INR400/t, while price hikes (INR50-75/t, so far) are insufficient to fully offset this impact. It expects further hikes going forward, while sustainability depends on demand. Capex is estimated to accelerate in next two years (INR15-17b in FY27 and INR20b in FY28) as it is adding 4.6mtpa clinker-backed grinding capacity.

* We maintain our estimates for FY27-FY28E. The stock is trading at 9x/8x FY27/FY28E EV/EBITDA. We value the stock at 9x FY28E EV/EBITDA to arrive at a TP of INR720. Reiterate BUY.

Sales volume rises ~8% YoY; realization/t declines ~7% YoY

* Consolidated revenue/EBITDA/adj. PAT stood at INR19.0b/INR2.9b/INR1.2b (flat/-19%/-29% YoY and in line/+10%/+9% vs. our estimate). Sales volume increased ~8% YoY to 3.9mt (+3% vs. our estimate). Realization/t declined 7% YoY (up ~1% QoQ) to INR4,881/t (~3% below our estimate).

* Opex/t declined ~4% YoY, led by ~9%/8%/6% decline in employee/freight/ other expenses per ton. Variable cost/t inched up ~1% YoY. OPM contracted 3.5pp YoY to ~15%, and EBITDA/t declined ~25% YoY to INR734 in 4QFY26. Depreciation/finance costs rose 9%/20% YoY. Other income grew 2.4x YoY.

* In FY26, revenue/EBITDA/adj. PAT stood at INR67.6b/INR10.1b/INR4.3b (+9/+17%/+37% YoY). OPM expanded 1pp YoY to ~15%. Realization/t fell 1% YoY to INR5,067, while EBITDA/t grew 6% YoY to INR757, led by cost savings. OCF stood at INR10.8b vs. INR7.8b in FY25. Capex stood at INR7.1b vs. INR6.6b in FY25. FCF stood at INR3.7b vs. INR1.2b in FY25.

Valuation and view

* JKLC 4Q performance was above our estimates, led by better cost efficiency. Though the company is among the top low-cost producers in the industry, aided by lower variable costs, its profitability remained lower than peers’ due to lower realization. The near-term outlook is challenging due to steep cost pressure and subdued price hikes. Further, aggressive capex is estimated to increase its net debt to INR27.9b in FY28 vs. INR12.6b in FY26 (net debt-to-EBITDA ratio at 2.3x in FY28 vs. 1.2x in FY26).

* We estimate a CAGR of ~9%/11%/6% in revenue/EBITDA/PAT over FY26-28 and project EBITDA/t of INR754/INR797 in FY27E/FY28E vs. INR757 in FY26. We estimate volume CAGR of ~8% over FY26-28. Due to aggressive capex plans, we estimate net cash outflow of INR3.5b/INR5.3b in FY27/FY28. The stock is trading at 9x/8x FY27E/FY28E EV/EBITDA. We value the stock at 9x FY28E EV/EBITDA to arrive at A TP of INR720. Maintain BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412