Buy J K Cement Ltd for the Target Rs 6,250 by Motilal Oswal Financial Services Ltd

Robust volume growth; capacity expansion on track Industry volume growth estimated at ~6-8% YoY in FY27

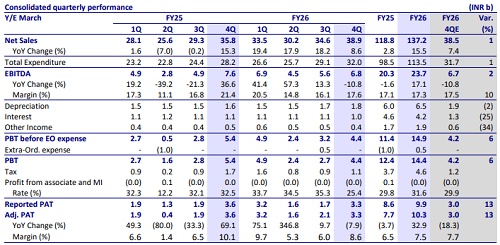

* JK Cement’s (JKCE) 4QFY26 operating performance was in line with our estimates. EBITDA declined ~11% YoY to INR6.8b. EBITDA/t declined ~19% YoY to INR1,008 (est. INR1,000) and OPM contracted 3.8pp YoY to ~18%. Adjusted PAT declined ~8% YoY to INR3.3b (+13% vs. estimate, driven by lower interest costs and lower effective tax rate vs. our estimates).

* Management indicated that grey cement industry demand is likely to grow ~6-8% in FY27, while the company targets double-digit volume growth. JKCE expects severe cost pressure in 1QFY27, with fuel costs rising by ~INR150/t, and potentially increasing toward ~INR200/t, if geopolitical disruptions persist. A price hike of INR10/bag has been taken in grey cement, and prices were also hiked in white cement and wall putty to partly offset the impact. JKCE continues its aggressive capex plans and guides for INR35-40b in FY27 and INR15-20b in FY28.

* We largely maintain our EBITDA estimates for FY27/FY28. We value JKCE at 17x FY28E EV/EBITDA to arrive at a TP of INR6,250. Reiterate BUY.

Highlights from the management commentary

* It expects at least 2.5mt incremental sales volumes in FY27 and indicated that annual incremental volume addition could eventually move closer to 3mtpa as future expansions get commissioned.

* It expects an additional INR50/t cost-saving opportunity in FY27, driven by higher green power share (waste heat recovery optimization and greater use of alternative fuels, particularly in North and South operations).

* Central India operations to deliver meaningful profitability improvement in terms of capacity utilization ramp-up, freight and operational benefits.

Valuation and view

* JKCE’s operating performance was in line with our estimates. The company reported robust volume growth, led by continuous capacity expansions. However, cost headwinds led to lower profitability on YoY basis. Elevated fuel/oil/packaging costs will weigh on margins in the near term. JKCE remains prudent in its capacity expansion and expects timely completion.

* We estimate JKCE’s consolidated revenue/EBITDA CAGR at 16% (each) and PAT CAGR of ~11% over FY26-28. We anticipate the company’s consolidated volumes to post ~15% CAGR over FY26-28. We estimate margin to decline in FY27 due to cost pressure, while margin would be at ~17% in FY28, similar to FY26. We estimate EBITDA/t at INR968/INR1,030 in FY27/FY28 vs. INR1,017 in FY26. We estimate its consolidated net debt to increase to INR79.8b in FY28 vs. INR55.7b in FY26. Net debt-to-EBITDA ratio is estimated at 2.5x in FY28 vs. 2.3x in FY26.

* The stock trades at 18x/15x FY27E/FY28E EV/EBITDA. We value JKCE at 17x FY28E EV/EBITDA to arrive at our revised TP of INR6,250. Reiterate BUY

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)