Neutral ITC Ltd for the Target Rs. 400 by Motilal Oswal Financial Services Ltd

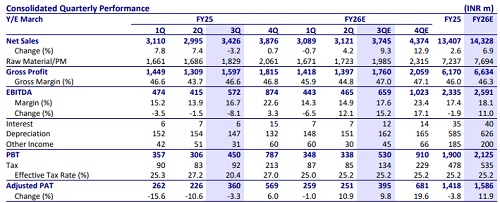

* The cigarette business is expected to show stable volumes and pricing, with the portfolio continuing to grow, aided by improvements in the product mix. We model 6% volume growth and 7% revenue growth in 3Q.

* FMCG business expected to post healthy growth. We model 9% revenue growth.

* The agriculture segment performed well during the quarter. We model 20% revenue growth.

* We model 6% YoY growth in cigarette EBIT, though margins may contract by 30bp due to rising leaf tobacco prices. In the FMCG business, we expect a 38% EBIT growth, with a 160bp margin expansion.

* In the paper segment, sequential improvement can be seen due to an increase in paper prices. We model 7% revenue and 5% EBIT growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412