Buy IRB Infrastructure Ltd for the Target Rs 27 by Motilal Oswal Financial Services Ltd

Steady performance; healthy toll growth and O&M order book to drive earnings

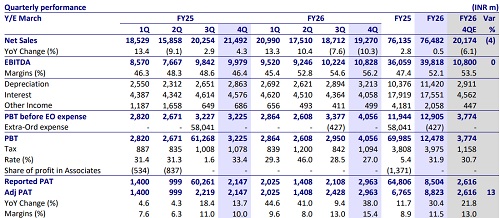

* IRB Infrastructure (IRB)’s revenue declined ~10% YoY to INR19.3b during 4QFY26 (in line). Its revenue included:

a) gains on InvITs & related assets as per the fair value measurement

b) dividend/interest income from InvITs & related assets.

* EBITDA margin came in at 56.2% (vs. our estimate of 53.5%) in 4QFY26 (+980bp YoY and +160bp QoQ). EBITDA grew ~9% YoY to INR10.8b (in line with our estimate).

* APAT grew 38% YoY to INR2.9b (13% above our estimate), supported by lower finance charges and lower tax outgo.

* Construction revenue stood at INR8.1b (-32% YoY); BOT revenue stood at INR7.1b (+11% YoY); and InvIT & Related Assets revenue stood at INR4b.

* In FY26, revenue was flat YoY, while EBITDA/APAT grew 10%/30% YoY.

* IRB declared an interim dividend of INR0.05 per equity share.

* The order book stood at ~INR449b (excl. GST) by the end of Mar’26.

* IRB delivered a steady performance, supported by rising toll collections. However, with EPC order inflows being subdued, the company is strategically focusing on bidding for Toll Operate Transfer (ToT) projects and building a sustainable O&M order book. Therefore, earnings growth is expected to be more driven by O&M and toll revenue than core EPC construction. In view of the changing order book composition and revenue growth toward toll and O&M contracts, we have cut our revenue/EBITDA by 10-15% for FY27 and FY28. We now expect a revenue CAGR of 19% over FY26-28. We reiterate our BUY rating with an SoTP-based revised TP of INR27

Resilient toll collections; healthy O&M orderbook and TOT opportunity pipeline

* In 4QFY26, IRB reported steady operating performance. Its EBITDA growth was supported by resilient toll collections and stable contributions from its BOT and InvIT portfolios.

* The order book stood at INR449b as of Mar’26, largely led by O&M (INR428b). The executable order book from O&M and EPC stands at ~INR33b for next year.

* NHAI plans to monetize about 1,806km of operational highways via the TOT model, having a revenue of INR27b at the end of FY26.

* BOT assets and InvIT investments continued to deliver healthy profitability, while construction margins were under pressure amid a weak order book.

Valuation and view

* IRB reported a steady performance, supported by rising toll collections. However, with EPC order inflows being subdued, the company is strategically focusing on bidding for the ToT projects and building a sustainable O&M order book. Therefore, earnings growth is expected to be more driven by O&M and toll revenue than core EPC construction.

* In view of the changing order book composition and revenue growth toward toll and O&M contracts, we cut our revenue/EBITDA by 10-15% for FY27 and FY28. We now expect a revenue CAGR of 19% over FY26-28. We reiterate our BUY rating with an SoTP-based revised TP of INR27.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412