2025-10-15 04:51:04 pm | Source: Motilal Oswal Financial Services Ltd

Buy Hyundai Motor Ltd for the Target Rs. 2,979 by Motilal Oswal Financial Services Ltd

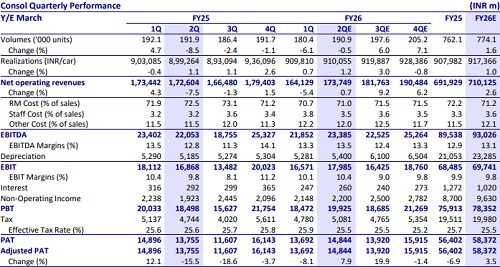

* Hyundai posted 0.5% YoY decline in volumes in 2Q. Exports were the key growth driver with mix improving to 27% from 22% YoY. Product mix was also favorable as Hyundai sold more SUVs than cars in 2Q.

* Amid weak demand, marketing spends to remain high QoQ. TN incentives expected to flow in from mid-2Q.

* We expect EBITDA margin to improve 70bp YoY to 13.5%, led by improved mix.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

?Cristiano Ronaldo puts on No. 21 shirt to honour Di...

Focus on Fit First (More Than Brands)

Automobiles Sector Update : No Sign of Weakness in D...

Building Materials Sector Update : Healthy Realizati...

Chiraharit touches roof on bagging Rs 4.49 crore ord...

Quant - Navigating Crests & Troughs - May`26 sectora...

SBC Exports moves up on extending contract with MPMMCC

Texmaco Rail & Engineering inches up on getting LoA ...

Monthly Ideas : Delhivery Ltd and TTK Prestige Ltd b...

Information Technology Sector Update : FY27 off to a...