Buy Hindustan Unilever Ltd for the Target Rs. 2,800 by Motilal Oswal Financial Services Ltd

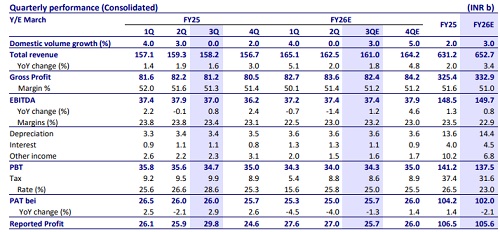

* The organic business is expected to deliver 4% revenue growth led by 3% volume growth. Reported revenue growth has been 2% due to the demerger of the ice cream business. ? The transitory impact of GST rate rationalization (which hit 40% of HUL's portfolio) weighed on the first half of 3Q.

* We model revenue growth of 3% in home care and personal care each, 8% in Beauty and Wellbeing, and 2% in F&B

* Reported EBITDA margin is expected to decline marginally by ~20bp to 23.2%. On an underlying, like-for-like basis, margins have contracted by ~60bp. However, at the reported level, margins benefit by ~50–60bp due to the demerger of the icecream business, which was a low-margin segment.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...