Buy Hindalco Ltd for the Target Rs 1,280 by Motilal Oswal Financial Services Ltd

Beat on earnings; outlook robust Consolidated performance

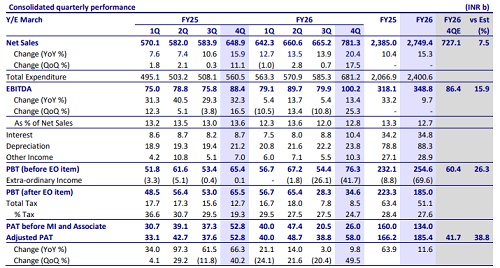

* Hindalco’s (HNDL) consol. revenue stood at INR781b, reporting a growth of +20% YoY and +18% QoQ (+8% above our estimate), led by a favorable pricing and better product mix.

* Consolidated EBITDA stood at INR100b (against our estimate of INR86b), rising 13% YoY and 25% QoQ, driven by the strong performance of the Indian business and better-than-expected Novelis EBITDA.

* Adj. PAT came at INR58b, against our estimate of INR42b (+10% YoY and 50% QoQ), led by improved profitability.

* The company recorded an exceptional item related to the repairs, clean-up, and restoration of the Oswego plant affected by a fire incident. The costs associated with the events (net of insurance proceeds) amounted to INR46b (USD500m) during the quarter.

* In FY26, the company reported a revenue of INR2,749b (+15% YoY), whereas EBITDA stood at INR349b (+10% YoY) and APAT at INR185b (+12% YoY).

* Consolidated net debt increased to INR648b as of Mar’26 from INR353b as of Mar’25, largely due to a rise in capex spend and the Oswego fire impact. This translated into net debt/EBITDA of 1.83x as of Mar’26 vs 1x during Mar’25.

Aluminum business

* Upstream revenue stood at INR114b in 4QFY26 (+11% YoY), and EBITDA stood at INR54b (+13% YoY; USD1,756/t), backed by cost optimization and favorable macros.

* Downstream revenue stood at INR49b (+35% YoY), whereas EBITDA stood at INR2.6b (+16% YoY), led by a better product mix and higher shipments. EBITDA/t stood at USD226 (-6% YoY) in 4QFY26 due to lower operating leverage at Aditya FRP as volumes are ramping up.

* Upstream Aluminum sales stood at 339kt (+2% YoY), while Downstream Aluminum sales stood 124KT (+18% YoY) in 4QFY26, backed by strong domestic demand.

* In FY26, upstream volume grew 2% YoY to 1,350kt, and downstream volume stood at 446kt, rising 11% YoY, backed by strong domestic demand.

* Upstream revenue stood at INR414b (+8% YoY) and EBITDA at INR189b (+16% YoY), translating into EBITDA/t of USD1,583/t in FY26.

* Downstream revenue came in at INR159b (+24% YoY), and EBITDA stood at INR9.8b (+55% YoY), leading to an EBITDA/t of USD248/t (+34% YoY) in FY26.

Valuation and view

* HNDL posted strong earnings in 4QFY26. Earnings growth was primarily driven by favorable pricing, better domestic product mix, and higher by-product pricing. Novelis posted better-than-expected earnings, adjusted for the Oswego fire incident.

* Going forward, the strong earnings outlook for the Indian business remains intact, and Novelis’ volume/EBITDA is expected to recover from 2Q/3QFY7 onwards, with the Oswego facility coming on stream in Jun’26.

* In addition, with the commissioning of downstream capacity, Indian business margins are expected to expand, offsetting the near-term cost inflation. Meanwhile, Novelis is expected to witness strong incremental volumes from the Bay Minette project, which is expected to get commissioned by 3Q/4QFY27E.

* We increase revenue by +9/10%, EBITDA by +10/11%, and PAT by +14/12%, for FY27/28, factoring in the strong domestic business outlook based on elevated commodity prices, cost savings, and recovery in Novelis’ earnings. At CMP, the stock trades at 7.5x EV/EBITDA and 1.7x P/B on FY28E. We reiterate our BUY rating on HNDL with an SoTP-based TP of INR1280.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412