Buy HDFC Asset Management Company Ltd For Target Rs.3,040 by Prabhudas Liladhar Capital Ltd

Higher SMID may bode well if broader market rallies

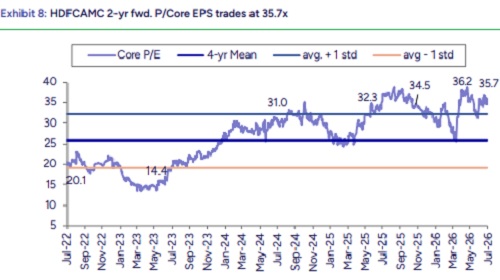

HDFCAMC saw a good quarter as revenue was a 4.7% beat due to better yield at 47bps which increased by 1.7bps QoQ (ICICIAMC +0.4bp QoQ). Opex was a miss largely due to higher other opex that included chunky CSR expense and technology cost. Positive yield movement QoQ suggests that major impact of TER change has been passed on to distributors. SIP flow fell slightly by 1.4% to INR 48.1bn (vs -4.5% for ICICIAMC). Led by strong equity performance in 3-yr bucket, market share in net flows remains 2nd highest; it was 14.6%/12.6% in FY26/Q1FY27. Near term triggers are (1) rally in broader markets that may drive better SMID returns and (2) SBIFM listing. We maintain multiple at 36x on Mar’28 core EPS but raise TP by 0.7% to INR 3,040. Retain ‘BUY’.

Good quarter; core income beat led by higher blended MF yield:

Equity QAAuM (incl. bal) came in as expected at INR 5.77trn (+1.4% QoQ). Revenue was higher at INR 10.9bn (PLe INR 10.5bn) led by higher yield at 47bps (PLe 44.9bps). Opex was more at INR 2.71bn (PLe INR 2.38bn). Staff cost was INR 1.4bn (PLe INR 1.3bn) and other opex was more at INR 1.28bn (PLe INR 1.06bn). Hence, core income was 2% ahead of PLe at INR 8.3bn (PLe INR 8.1bn) resulting in operating yield of 35.4bps (PLe 34.7bps). Other income was INR 2.6bn (PLe INR 2.0bn). Tax rate was a tad lower at 23.1% (PLe 24%) in Q1'27. Hence, core PAT was 3.2% above PLe at INR 6.4bn, core PAT yield was 27.2bps (PLe 26.4bps).

Healthy equity performance in 3-yr bucket supports net flows:

MF yield increased by 1.7bps QoQ suggesting that the entire impact of the TER change has been passed on to distributors. Share of equity/ETF segment increased by 38/8bps QoQ while that debt segment decreased by 118bps. Management aims to maintain an operating margin between 33-35bps. While equity performance in 1-yr bucket has slightly weakened, it remains one of the best in the 3-yr bucket. Market share in net equity flows is one of the highest at 14.6%/12.6% FY26/Q1FY27.

Higher CSR expenses drive opex increase:

Other opex rose by 24.5% QoQ largely driven by CSR expense (chunky in nature), and technology cost. Projected ESOP costs are INR790-800mn for FY27, INR 630mn for FY28, INR410mn for FY29 and INR110mn for FY30. Cost to AUM may trend down; we are factoring opex to AuM of 9bps in FY28E (10bps in FY26). HDFCAMC’s first SIF offering i.e. HSIF Equity Ex-Top 100 long-short is approved to be launched in near term.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

Tag News

Accumulate Union Bank of India Ltd For Target Rs.190 by Prabhudas Liladhar Capital Ltd