Buy Godrej Properties Ltd for the Target Rs. 2,180 by Motilal Oswal Financial Services Ltd

Showcasing a diversified scale-up

Robust BD in FY26; launch pipeline remains healthy

Godrej Properties (GPL) added 18 new projects with an estimated saleable area of ~33msf, offering INR421b sales potential in FY26, which was >2x the guidance. These include INR386b in Group Housing and INR35b Plotted Developments. Apart from the larger cities, the company has added new projects in Nagpur (INR7.5b), Coimbatore (INR4.5b), Raipur (INR3.8b), and Vadodara (INR2.8b). These provide healthy pre-sales visibility for the medium term. It has planned for INR200b BD and INR480b launches in FY27, which would support pre-sales growth in the coming quarters.

Aiming for double-digit pre-sales growth in FY27

GPL clocked INR102b pre-sales in 4QFY26 (flattish YoY; ~12% above our expectations). Overall, in FY26, its pre-sales grew by 16% YoY to INR342b, which was 5% higher than the annual guidance; a broad range of 11 individual projects across 6 cities, each generating booking value of >INR10b, drove FY26 performance. Further, the annual pre-sales were well diversified regionally, with key contributions from MMR (INR103b), Bengaluru (INR88b), NCR (INR74b), Pune (INR37b), Hyderabad (INR24b) and Others (INR16b). The company has guided for INR390b pre-sales in FY27 (+14% YoY). We bake in a 10% CAGR in pre-sales to INR413b during FY26-28E.

Net debt increases in FY26 but remains at comfortable level Collections grew by 14% YoY to INR80b in 4Q, which was very strong. Overall, FY26 collections grew by 17% YoY to INR200b (achieved 95% of the annual guidance). Based on the pre-sales growth and progress in execution, we expect collections to expand at a 17% CAGR to INR274b during FY26-28E. Net OCF (before land & approval payments) stood at INR78.3b in FY26 (vs INR74.8b in FY25). GPL incurred INR91b towards land, approval, capital outflow, and advance to JV partners in FY26 (flattish YoY). Overall, net debt increased by INR31b to INR64b in FY26, while net D/E remains comfortable at 0.33x.

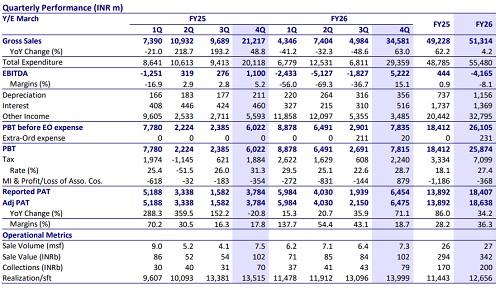

Financials

* In 4QFY26, revenue stood at INR34.6b, up 63% YoY. EBITDA was at INR5.2b, with EBITDA margin at 15.1%. PAT was at INR6.5b, up 71% YoY, with PAT margin at 19%.

* In FY26, revenue stood at INR51b, up 4% YoY. EBITDA loss was at INR4.2b vs profit of INR444m YoY. PAT was at INR18.7b, up 34% YoY, with PAT margin at 36%.

Valuation and view

* GPL has delivered healthy pre-sales growth despite a high base on the back of benefits of diversification across many regions. Further, collections growth has been slightly higher than pre-sales growth, which is encouraging. The strong BD during FY26, along with launches planned in the coming quarters, provides comfortable growth visibility over the medium term. While net debt increased in FY26 due to the sharp increase in project additions during the year, leverage remains at comfortable levels.

* Despite the high base, management has guided for 14% pre-sales growth, whereas it anticipates collections growth to be better than that.

* We have a BUY recommendation with an SoTP-based TP of INR2,180.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412